Q4 2021: Year In Review

The Jiggy Capital Newsletter #8

Newsletter Review

Thank you all for being apart of this newsletter these past two quarters. It’s been a blast putting this substack together, shooting from the hip sharing different kinds of data and overall thoughts while going through my investing journey. 860+ of you signed up for my emails since starting the Jiggy Capital Newsletter six months ago and I’m appreciative of each one of you.

I started this newsletter for no other real reason than I was sick of abiding to the laws of 280 character tweets while portraying data, and also I enjoy playing around with numbers and researching different companies. I never expected it to be this fun and become such a positive feedback loop for me and my development as an investor — but also as a writer!

Unfortunately I haven’t kept my side of the bargain with my intended bi-weekly schedule for this past Q4 with this being only my third Q4 newsletter (goal is six per quarter) and first since October 24th. This was due to just life happening being busy with work and traveling, getting some health news, and then finally getting ready to move out of Missouri.

Now that I’ve made my final move for work in my rotational development program back to Chicago, I foresee having more of a free flowing schedule to continue making these newsletters into 2022 and beyond on the normal bi-weekly cadence. I’m also brainstorming and testing out new topics to highlight and am pretty excited for the newsletter moving forward into 2022!

Here are my spreadsheet links that I’ve gotten some really nice feedback on this year (especially the financial watchlist):

2021 Year In Review

2021 felt like the pivotal year I really learned about myself as an investor and how I wanted to interact with the markets. Starting my investing journey in January 2020 messing around on WSB for the most part, it felt like you could get by with any market strategy and you would end up doing pretty good in 2020. I traded in and out of positions and for the most part and just didn’t take it all that serious (no outside background or exposure to stock market before then).

In general I like to think of myself as someone who is not shy about my passion for anything that strikes my broad interest, not being afraid to say I’m a complete dumbass stepping into a new topic, willing to admit I’m wrong while staying open minded and be a complete sponge. This is how I got through engineering school and life so far, so I like to think it has some decent example of execution.

This is part of the reason why Fintwit has been such a match made in heaven for me (or time destroyer depending on who you ask lol). I would never get this exposure anywhere else to the thinking of some much smarter folks than myself and it really sets something off in my brain to understand their perspective and soak everything in.

I came into this year being a more short term oriented trader interested in SPACs - which is what actually started this wildfire effect of myself diving deeper into the markets. I created my fintwit account early December 2020 to follow certain SPAC traders on a separate feed than my personal one and that I think was one of the bigger butterfly effects I’ve had in my life (which is hilarious).

As I slowly had more exposure and knowledge from different pockets of fintwit (expanding outside SPACs), I got completely sucked in and started thinking much differently on how I viewed the market and how I wanted to interact with it. I then quickly got much more long term focused and fundamental based as 2021 progressed, dipping my toes into different sectors but overall being a generalist not knowing what I value in a company or what I truly look for past a strong brand that I know.

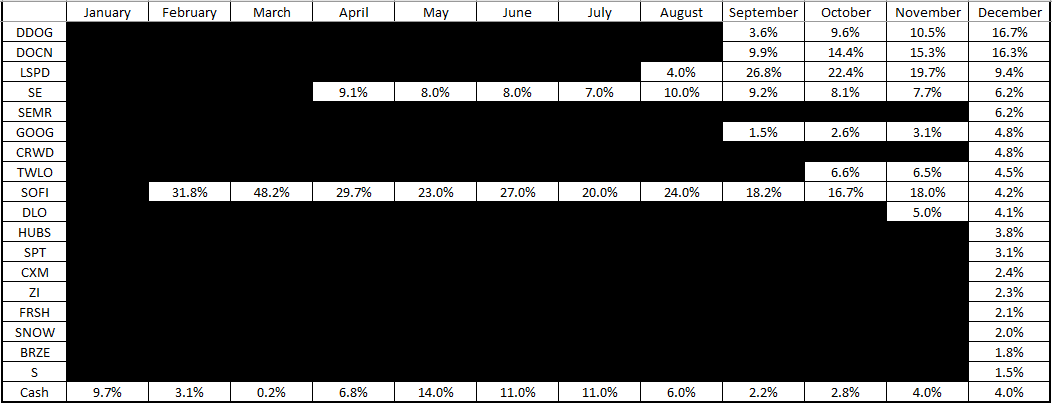

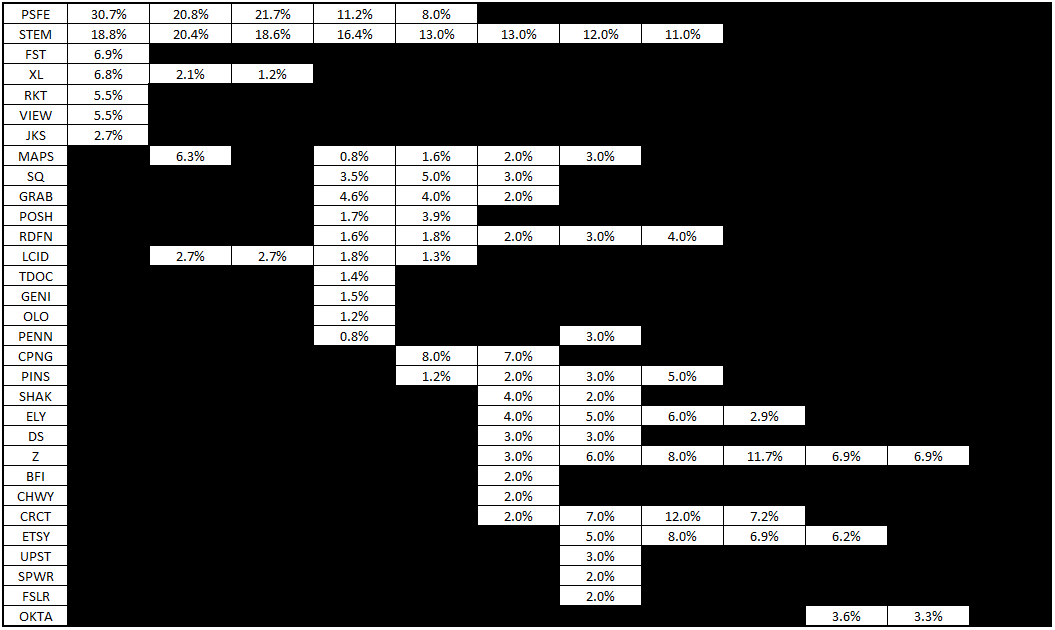

Even from just my end of Q3 newsletter write up, my process has changed a great amount since for what I value in a company in what sectors, as you’ll see in the chart below showing my holdings as the year progressed! I’m really starting to see the benefits of honing in on a craft and finding sets of key parameters that I think tell a bigger story and trend than just the numbers itself.

Now I totally get it, am I going to claim I’m long term oriented when I’ve just entered 8 new positions this month and my overall average held length is just under 3 months?? (sad typing that out)

I will counter that by saying it’s quite obvious when you look at my holding trends that I’ve settled into becoming a (somewhat deranged) SaaS investor of all kinds. This wasn’t always the case and I will remind you I never looked at literally any SaaS company further than a chart until like July because I had simply written them off as a bubble for so long.

The fun part about how I’ve used my fintwit account also as a journal, I have a thread progressing through my whole 2021 of buys and sells going over each iteration I went through!

This SaaS fix really got started in July/August when I invested in Lightspeed then Digital Ocean. Their strong growth and metrics really got me interested to dive deeper in software companies and I ended up putting out my Operating Expense Analysis newsletter of well known growth stocks which really sparked something further.

I became enamored with the Income Statement trends of companies like Datadog, Twilio, Alphabet etc and quickly invested in all three around that late August/early September timeframe after putting out the OpEx newsletter. Following those companies and others through Q3 earnings, learning more about the broader SaaS space, listening to founder podcasts among other forms of information, it really just hit me that these “overvalued” bubble stocks I had written off are potentially some of the best companies we have seen.

The common traits of things like low touch sales motion of software companies with little barrier to scale, paired with strong unit economics, strong macro trends in TAM, high focus on innovation and R&D investment and incredible GTM strategies (inbound vs outbound) are just such strong dynamics not found in other sectors that I don’t think I can ever go back to other areas of the market.

For better or worse!

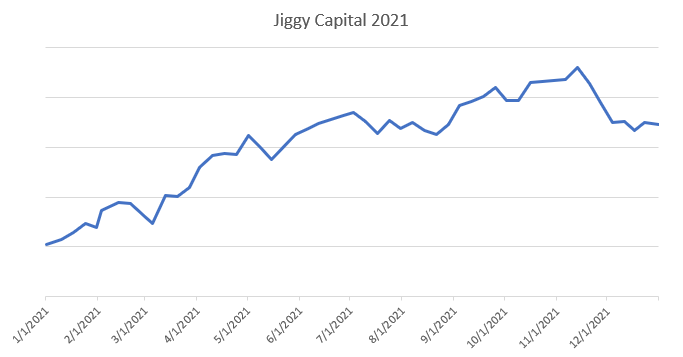

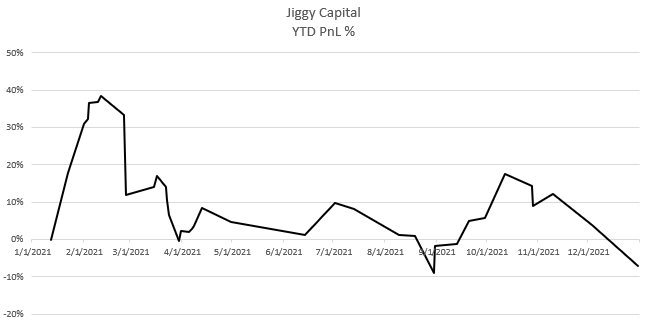

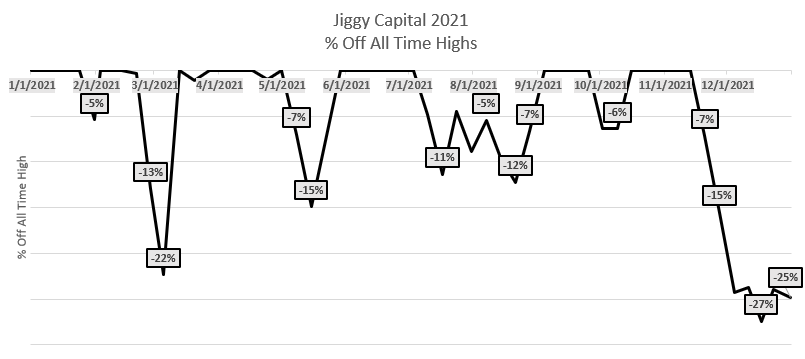

2021 Performance

Portfolio Chart:

% Performance:

% Off All Time High Chart:

2021 Performance Commentary:

What a crazy year PnL wise. My final tally performance was hard to calculate across all my different accounts (Roth IRA, Taxable, HSA) and due to the fact that my portfolio increased 5x just from deposits. Luckily Commonstock (highly recommend) has a great feature which adjusts for deposits and gives a time weighted return which came out to be -6.55%. I ended up doing the calculation myself as well and got -7.53% so I think that’s a safe ballpark to call -7.05%. This would come out to -35.34% of Alpha.

{kind=link}

The only good news I can lean on performance wise is my 401k had an awesome year (again) and it’s my largest sum of money in the market, and I’m coming off a 55.23% year in 2020 + overall up 44.29% since opening my TD Ameritrade account last July from Robinhood.

I think my significant underperformance this year is pretty easily attributable to figuring what kind of investor I was going to be and running into a few unfortunate buzzsaws creating needed lessons. I went through many strategy iterations this year - with my most profitable one being a SPAC trader early in the year going up 40% quickly, but I knew I wasn’t going to do that long term and it took some time to adjust to a more traditional playbook building out a long term portfolio. Then you pair that dynamic with a couple top holdings seeing significant pullbacks that were hard to make up for, and I wasn’t all that surprised by the final tally.

After that hot start to the year, I then quickly had my first ever 20%+ drawdown from the February-March growth stocks carnage making it all the way down to 0% YTD in April. What I only realized now doing this write up is this most recent drawdown from my early November high has actually been more drastic for me than the February-March one! It doesn’t help when your largest position at 28% gets cut in half after a short report and not well received earnings report.

That ended up being the theme for my year in 2021 outside of finding my focus as an investor. Big drawdowns in single stocks, most of the time ones in my top half, that made it significantly hard to overcome. Like I mentioned, the Lightspeed drawdown has very much been felt, but looking even further I booked losses of 20%+ in Zillow, Pinterest and Cricut, while still being down 20%+ on dLocal.

Moving forward, I expect my order of holdings to drastically change over 2022 as my portfolio should at least 3x from just deposits again. Past the rebalancing, I don’t foresee any potential exits to positions on the horizons which is the way I want it to be. I could see myself getting up to 25 positions for 2022 in a couple scenarios, but I know I won’t be going in and out nearly as much as I did in 2021 (as seen below).

Holdings Progression:

Meme of the year:

Q4 2021 What I Learned

Position Sizing is the difference between consistent alpha through portfolio turbulence and underperformance that’s challenging to make up for. The good news is I’m young to this investing world and bound to be make these mistakes along the way, and I would much rather learn these lessons that this stage in my career. Single company risk is something I didn’t respect as much until I got handed a harsh lesson repeatedly this year.

Diversifying vs Diworsifying… this is one of the biggest implementations I’ve done over the last month as I decided I wanted to go from 10 positions up to around 20 over time. I want to still be concentrated in the sectors I’m most bullish on, but having a small basket of each idea is something that I believe will highly mitigate that single company risk factor susceptible to black swan events that made this year challenging to see consistent growth.

It can really turn on any company for whatever reason/narrative and I don’t think I’ve been accurate in having so much faith in my pure stock picking abilities having such a concentrated portfolio. It also helps that I’m amazed by so many companies and believe in the path forward they have!

Don’t Underestimate “Niche” when judging a disrupting, innovating company. The amount of times I was amazed by the strong fundamental trends of some random company I had just learned of is amazing. The typical software winning playbook is a well received app to then develop into a platform selling to different tiers of customers. It never failed to amaze me just how big some markets are to produce all these multi-billion dollar software companies.

2021 What I Learned

Figure Out Your Golf Swing of the investing world, and don’t be shy to try different swings. There’s so many ways to make money interacting with equities and I don’t think there’s true merit to look down upon any one different way (outside of pure grift of course). I’ve gone from a SPAC trader, to growth stock swing trader, to growth stock investor, to tech investor, to now a software investor all in the course of this year. I’m not trying to box myself in and still own a few companies outside that realm, but that is where I’ll be primarily spending my efforts.

{kind=link}

Isn’t This All So Fun? I can’t believe how much fun the investing world is honestly. The amount you learn about yourself, the amazing people you meet with similar passions and goals, being exposed to wicked smart people on Fintwit, and then of course the joy of being right…and then building wealth all the while. Going into 2021 I was very hooked on the stock market itch after investing for most of 2020 and I still never would’ve imagined it’d snowball the way it did this year.

Q4 21 Commentary

As I have made clear in my year in review section, I’ve more or less decided to be a software focused investor and have leaned completely into that this quarter. I entered 10 new positions this quarter (8 in December) and exited 2 positions. I’ll delve into this more in the next section but I had a deeper awakening of the importance with position sizing which was the main reason for such an increase.

My failed positions this year in other sectors (for various reasons that don’t effect software companies) made it harder and harder to justify owning other companies with each blow that occurred. I like to think I’ve learned something from each one of the sharp unnatural pullbacks from whatever catalyst, as I would like to think each of them all are still quality companies (Zillow, Pinterest, SoFi, Lightspeed, Cricut).

Even with that, I don’t look at software investing as easy whatsoever. Every company has those benefits in the space so you need to be disciplined in looking at what matters financially, underlying fundamentals and KPIs, strength of management, product development potential, go-to-market playbook effectiveness. All that then just to judge “is that high multiple it currently has is worth it, and is there still good upside with multiple compression moving forward.”

Notice how I’m not even mentioning anything about understanding the actual product (since I think that’s the hardest part). That comes with time over many earnings calls and reading many G2 reviews, and is the area I don’t think I have anything close to an edge. I also am a believer that financials and KPIs can tell very strong stories to help that learning curve along.

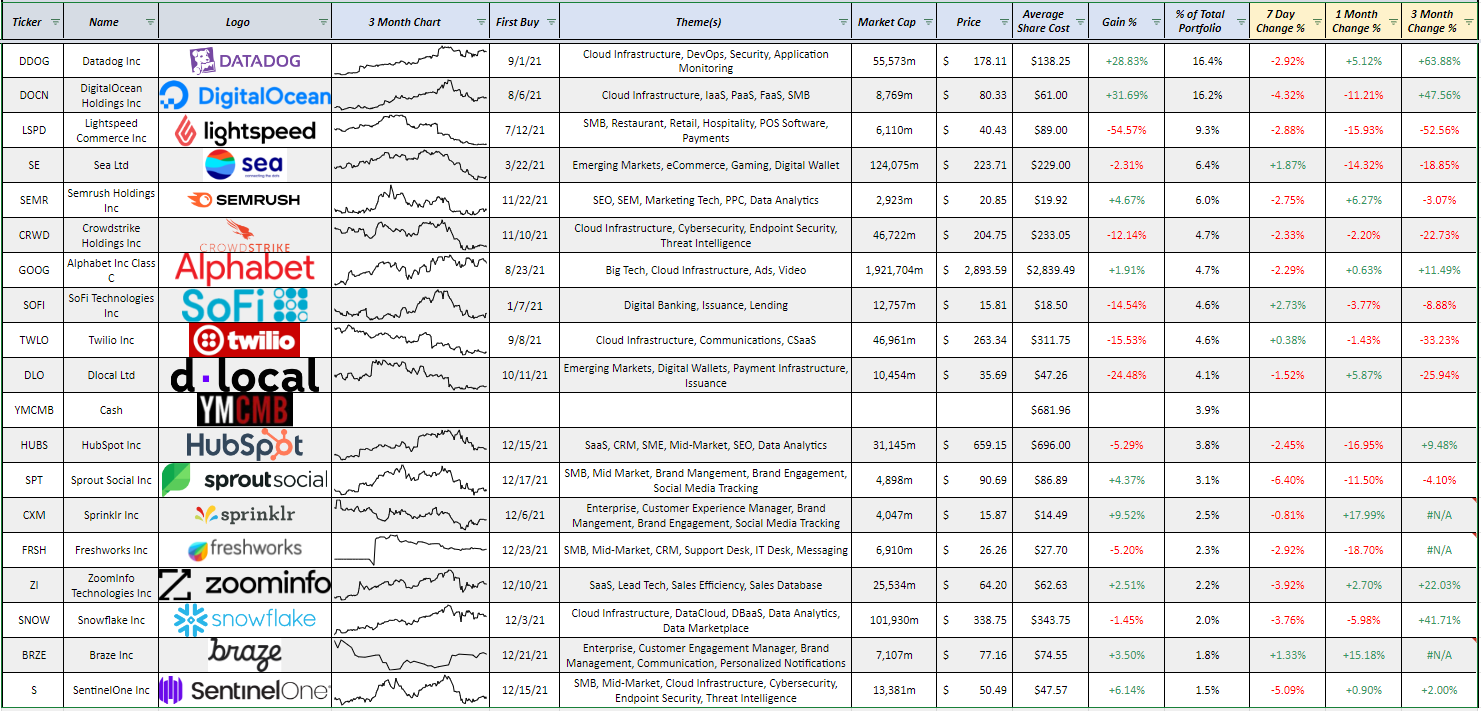

My Portfolio

This section turned into a really challenging one to not have this newsletter turn into a book, so I’ve only just briefly gone over each position from a top level view (the side effects going from 10 positions to 18)…

I plan on doing another separate newsletter where I go over how each company in my portfolio is progressing and the key metrics I look at just before my quarter review newsletter.

Datadog (DDOG)

Percentage Holding: 16.3%

Last Quarter Holding Percentage: 8.5%

First Buy: 9/1/2021

Last Buy: 11/23/2021

P/L %: 29%

Why I Invested/Q4 Update: Datadog had a 2021 for the ages. They’ve only reported 3 quarters from the year, but they’ve knocked it out of the park everywhere you would want them to. They continue to have one of the smoothest GTM movements in enterprise software and their product cadence took it up a notch. I couldn’t be more pleased with their Q3 report and it’s incredible we’ve seen Datadog re-accelerate top line growth at such a larger base from 56% to 75%.

This is the product of a true land and expand, product-led SaaS model where Datadog just continues to develop new complimentary products and continue to see higher customer adoption of new products, where now 77% of all customer have 2+ products, and 31% have 4+ products.

For the best write up on Datadog’s Q3, Peter from Software Stack Investing is an amazing resource.

My Plan Moving Forward: With Datadog’s continued extremely high level of execution, I’ve continued to add to my position in small increments since their Q3 report. I plan on building out other positions until the Q4 earnings season rolls around but is one that will stay a staple of my portfolio. Hard to find many things to be worried about with this company outside of valuation.

Digital Ocean (DOCN)

Percentage Holding: 16.4%

Last Quarter Holding Percentage: 12.6%

First Buy: 8/6/2021

Last Buy: 9/22/2021

P/L %: 32%

Why I Invested/Q4 Update: Q3 was an absolute rollercoaster for DigitalOcean stock and the company. Finishing the year up 88% since their IPO, while still being down 40% from their ATH is quite the interesting dynamic - and I haven’t done too much at all through that turbulence as an investor.

DigitalOcean continues to show that their products are resonating with their customers and are gaining further traction, as their unit economics have only improved. Taking NDRR from 104% to 116% Y/Y with SMB’s is not a small feat and shows they have a serious value proposition for these smaller developers to use their more simple services instead of the hyperscalers.

The one issue I have with them in their Q3 report is that we actually saw a net negative in customer adds from last quarter. Management has said this was due to getting a couple bad apples off their services, but you would hope the organic growth in customer adds would still be greater than that effect.

My Plan Moving Forward: With this being such a large position (mostly due to outperformance), I’ve felt pretty comfortable with this position size before their Q3 earnings report and I feel the same way after as well. I’m still very happy with this position and how DigitalOcean is executing but I’m prioritizing other areas to add in the first quarter of 2022.

Lightspeed (LSPD)

Percentage Holding: 9.6%

Last Quarter Holding Percentage: 26.4%

First Buy: 7/12/2021

Last Buy: 9/29/2021

P/L %: -55%

Why I Invested/Q4 Update: Whew….. what a ride this year LOL. Lightspeed was almost 32% of my portfolio at one point where I was up about 40% on my position, then it all came crashing down after a (objectively weak) short report and then a Q3 earnings report that didn’t meet the street’s baked in outperformance expectations.

This one has been incredibly volatile after being one of the strongest stocks I owned. To help mitigate my changes having something like this happen again, I have now implemented a rule on no position can have a cost basis above 15%, and ideally below 10%.

Now about the actual company, I thought Q3 earnings were good!! Everything I track looked good except overall customer adds. They continued to meaningfully expand ARPU and payments adoption trends are extremely strong.

My Plan Moving Forward: I’m still quite bullish on Lightspeed and think it could see a great bounce back in 2022 in all honesty, but prepared for all scenarios. I think investors are just uncertain with the Lightspeed story and I think a couple strong quarters of forward momentum will greatly help.

I trimmed my position in the 70s and 60s when it lost key levels but didn’t take off nearly as much as I should’ve looking back. I don’t intend adding to this position for quite some time as it’s still a very large % of my holdings and like other areas for future adds.

The only thing I’ll pat myself on the back on is I never caught the falling knife during this destruction to make things worse. I thank my learnings from earlier this year, although the effects were still very apparent unfortunately.

Sea Limited (SE)

Percentage Holding: 6.4%

Last Quarter Holding Percentage: 8.4%

First Buy: 3/24/2021

Last Buy: 7/28/2021

P/L %: -2%

Why I Invested/Q4 Update: Sea Limited is the second biggest reason why I’ve been open to expanding my total holdings. This was one of the strongest stocks on the market for much of the last 2-3 years, but has been deflated almost 40% from it’s November ATH and has seen sentiment completely shift.

Picking apart their Q3 earnings, you can see some softness in the gaming business which has served as their growing internal cash cow to finance their Shopee global domination conquest. This was the first time they’ve had flat sequential Garena user numbers since going public which is not a very fun fact. I’m looking for Q4 numbers to show this was just a mortal quarter for Forrest Li and co.

My Plan Moving Forward: I still don’t plant to add to this position as there’s the ever looming large execution risk that Sea Limited has with Shopee and Sea Money. I feel comfortable to still hold my position and let things play out.

Semrush (SEMR)

Percentage Holding: 6.1%

Last Quarter Holding Percentage: NEW

First Buy: 11/22/2021

Last Buy: 12/17/2021

P/L %: 5%

Why I Invested/Q4 Update: Semrush caught me off guard when I was first looking into them after seeing their name a couple times on Fintwit. Their fundamentals and trends really popped out to me when you consider this isn’t a company trading at a premium valuation.

69 Rule of 40 Score ( 53% Y/Y Growth, 16% FCF Margins)

NRR trends of 117% → 121% → 124%

Consistent near 10% sequential revenue growth over last 5 quarters

Semrush really got me on a marketing tech tools binge as I realized this space had so many exciting, innovative companies that are building platforms out from their initial product/act. Semrush has some incredible product development and a very popular freemium model where the top of the funnel is always full.

I feel quite confident company would trade at a much higher valuation if the founding team weren’t Russian, and over enough time horizon I think the company execution will win out over any such doubts or worries.

My Plan Moving Forward: I’ve sized this into a nice position and I’m going to the let the company execute and follow along from here closely.

Crowdstrike (CRWD)

Percentage Holding: 4.7%

Last Quarter Holding Percentage: NEW

First Buy: 11/10/2021

Last Buy: 12/1/2021

P/L %: -12%

Why I Invested/Q4 Update: Ever since I started investing, Crowdstrike seemed like a really interesting company when I first read about them on Wallstreetbets. The need for new generation cybersecurity continues to be a growing need and Crowdstrike is a testament to that. An incredible company with 30%+ FCF margins still growing 63% Y/Y, Crowdstrike is another textbook land and expand software winner. 68% of customers now have 4+ modules (up from 57% Y/Y), 32% have 6+ modules!

With strong management lead by Founder/CEO George Kurtz, this has always been a company I’ve admired with such balanced and strong fundamentals. This stock has seen increased pressure in this most recent pullback and I actually started a small position just before that all happened. It’s all relative with these kinds of software companies but I’d argue the stock is very reasonably valued here at 78x 2022 FCF.

{kind=link}

My Plan Moving Forward: I have quickly built out a solid position in Crowdstrike with their 30% pullback from ATHs. I was quite impressed with their Q3 earnings and have added to my position since that report. I plan on doing so again as but it probably won’t be the first get new money into 2022.

Alphabet (GOOG)

Percentage Holding: 4.7%

Last Quarter Holding Percentage: 1.9%

First Buy: 8/23/2021

Last Buy: 12/3/2021

P/L %: 2%

Why I Invested/Q4 Update: This company is something special, and investors rewarded them with a breakout 2021 up 67% while being flat since August. They followed up an incredible Q2 2021 earnings report with another killer Y/Y topline growth at 41% and 52% gross profit per share growth. For a company their size to be putting up numbers like that is just incredible. It’s no secret these mega cap companies making up the largest portions of our indices are absolutely amazing companies that don’t come around too often.

My Plan Moving Forward: When I decided Alphabet was too impressive for me not to own, I decided I would buy my position over time in monthly buys. This has gone to plan and has worked out well since GOOG shares have largely been flat since I started building a position. I have no intentions of stopping those monthly buys for 2022 and beyond!

SoFi (SOFI)

Percentage Holding: 4.5%

Last Quarter Holding Percentage: 14.9%

First Buy: 1/7/2021

Last Buy: 7/20/2021

P/L %: -15%

Why I Invested/Q4 Update: In my last quarter end update, I was pretty honest about my thoughts on SoFi and felt like I wouldn’t have it as such a large position with the criteria I walk through now. After Q3 earnings that were actually very solid, I still just didn’t great about having such an oversized SoFi position anymore with their core business (that is providing most of the growth) very much being the lending business the company was originally built on.

My Plan Moving Forward: I used these last couple months to significantly reduce my position in SoFi and put those funds towards areas I felt more confident about moving forward. At this point I’m quite happy with the sizing now and don’t plan on reducing it further. All of fintech had quite a tough Q4!

Twilio (TWLO)

Percentage Holding: 4.5%

Last Quarter Holding Percentage: NEW

First Buy: 9/8/2021

Last Buy: 10/28/2021

P/L %: -16%

Why I Invested/Q4 Update: My Twilio fascination is very similar to that of Crowdstrike. A company I was familiar with when I started investing unlike most other software co’s that I’ve become such a fan of. Twilio has a very interesting core business that’s quite unlike other SaaS with the Communication Platform-as-a-Service (CPaaS) offerings. Because of this, Twilio gross margins have only decreased as they’ve now ramped up their International efforts which is even more fragmented and expensive to provide their CPaaS solutions piping through the network providers.

Twilio has a couple really exciting new developments coming down the pipeline in Twilio Flex, their next gen contact center software, and Twilio Engage, where you can build personalized marketing campaigns on every channel (Twilio Segment M&A infusion). These two have significantly different GTM strategies as they’re much more high ACV, enterprise focused, whereas core Twilio is bottom up, developer focused, usage based structure.

Because of theses staunch differences, the market is handing Twilio quite a “show me” valuation currently. I would be a more stronger bull if they had better underlying fundamentals, and especially when you consider how large they are. They have a FCF margin range of -10% to 0.5% over the past few years, but that’s now on a base of 2.6B TTM revenue and almost a 50B valuation. I would ideally like to see stronger margins there but at ~20x 2022 gross profit with 60% growth this year and 30%+ expected the next two years, I can be patient to see how Flex and Engage play out in a smaller position.

My Plan Moving Forward: I actually trimmed this position in my most recent buy or sell, and I think that puts my cost basis % in the sweet spot for how I feel about their outlook. I could equally see playing out Twilio providing amazing returns over the next couple years with strong execution in their new platforms, or they could really struggle putting it all together and continue to see their multiple compress.

dLocal (DLO)

Percentage Holding: 4.0%

Last Quarter Holding Percentage: NEW

First Buy: 10/11/2021

Last Buy: 12/7/2021

P/L %: -24%

Why I Invested/Q4 Update: When I first looked at dLocal’s fundamentals and margins, I was shocked at how balanced it was in hypergrowth, net expansion, and highly profitable bottom lines. I wrote a one pager on them when I quickly started to appreciate what they are building that best describes why I’m bullish. Having 30%+ net margins while still growing triple digits and complimenting that with 170%+ NRR is not something you see very often.

I don’t think dLocal is nearly as expensive as it looks at 41x 2023 EBITDA growing 55%+ the next two years, and it’s a company I get very excited about. They obviously provide value to large enterprises looking to do business in emerging markets. This is a very long sales cycle business with high switching costs and lots of onboarding from what I understand.

My Plan Moving Forward: In their Q3 report they did not provide guidance and had their IPO lockup happen thereafter which resulted in a 25% drawdown. I don’t quite enjoy the not providing guidance in their second ever earnings report as a public company part which is why I haven’t added more aggressively on this pullback.

Hubspot (HUBS)

Percentage Holding: 3.8%

Last Quarter Holding Percentage: NEW

First Buy: 12/15/2021

Last Buy: 12/15/2021

P/L %: -5%

Why I Invested/Q4 Update: Hubspot is a company where once I started to appreciate software companies and understand some of the common winning playbooks, they really shined in any analysis I did. Hubspot revenue growth re-acceleration as they went from an app (marketing automation hub) to a full platform is a truly a thing a beauty: 25% → 32% → 35% → 41% → 53% → 49%. They’ve stayed above a 60 rule of 40 score with solid FCF margins ranging from 8% to 22%.

I love the playbook they’re running and the kinds of products they offer being a more nimble, modern CRM to all types of customers with their different product tiers (Enterprise, Pro, Starter, Free).

My Plan Moving Forward: I got a starter position in HUBS and plan on continuing to add to it into Q1 2022. I think they had the most tame reaction to a short report I’ve ever seen, which made sense since it was only on a valuation basis. I agree it’s not a cheap valuation but they’ve shown great past execution and still have a long runway ahead in my view with their other products outside of Marketing Hub.

Sprout Social (SPT)

Percentage Holding: 3.2%

Last Quarter Holding Percentage: NEW

First Buy: 12/17/2021

Last Buy: 12/22/2021

P/L %: 4%

Why I Invested/Q4 Update: These next two companies go hand-in-hand, and I’m still quite new to both in my investing research journey. With Sprout Social, they are the SMB, mid-market side of the coin to what Sprinklr is. There is so much to like with Sprout when you start to dig a little deeper. They’ve had improving sales efficiency at scale showing strong GTM motion, impressive growth upstream with >10k & >50k ARR customers, trending FCF margins at 9% from 5%, and accelerating Y/Y revenue growth at 27% → 33% → 34% → 42% → 46%.

Combine this with all 4 co-founders still being involved in a big way and this becomes quite a compelling long, and is actually a company I’m quite excited about. They’re another company running the product to platform motion within brand and social media management.

My Plan Moving Forward: I very much plan on continuing my venture learning more about Sprout Social and will likely be adding to this position in the near term. Unfortunately, this has received some well deserved attention is holds a pretty lofty valuation which is something I monitor.

Sprinklr (CXM)

Percentage Holding: 2.4%

Last Quarter Holding Percentage: NEW

First Buy: 12/14/2021

Last Buy: 12/20/2021

P/L %: 10%

Why I Invested/Q4 Update: Now for the large enterprise solution to brand and social media management. Sprinklr is another company showing acceleration in important fundamentals like NRR, revenue (14% → 19% → 27% → 32%) and large customer growth. What’s different about Sprinklr is that it’s over $100,000 per seat to use the platform, meaning they are an large enterprise game through and through.

They’ve developed new features to still drive top of funnel like Modern Research Lite, which was launched in September. This free, limited social media listening tool is a great way to drive new customers in a different way than their traditional enterprise long sales cycle method.

My Plan Moving Forward: This is a very reasonably valued company for what I think they can do. Trading at under 9x 2022 Gross Profit, I feel quite comfortable taking a small speculative position while I further do research on them. I quite like the founder/CEO and think this is a strong, mission driven company for a different kind of customer.

I don’t think I’ll be adding to this position as aggressively as some of my other new ones and want to let it work for some time (at least until next earnings) as I have doubts about some pure GARP companies like this.

Freshworks (FRSH)

Percentage Holding: 2.3%

Last Quarter Holding Percentage: NEW

First Buy: 12/23/2021

Last Buy: 12/27/2021

P/L %: -5%

Why I Invested/Q4 Update: Another recent addition to my portfolio, Freshworks is a recent IPO that really resonated with myself after doing work on Hubspot. Freshworks is basically gunning to run a similar playbook and become a modern, more nimble product suite for SMB and mid-markets to use.

The way they are doing it is slightly different than Hubspot with Freshdesk (Customer Experience hub) vs Marketing Hub as the core winner and going up or down stream from there into IT Service Management and Sales & Marketing products, but it still feels quite similar and Freshworks has strong fundamentals behind it.

My Plan Moving Forward: I can honestly say this company excites me just as much as any position in my portfolio. I think there’s such an obvious winning path for this company in the areas they play in, but it all comes down to execution in an extremely hard and competitive arena.

This is another holding where I could equally see it 10x or go nowhere over the coming years but is one that I want to see out. I’m taking this position quite slow as it’s still such a new IPO and we still have lockup pressure ahead, but absolutely intend on building it out over time.

ZoomInfo (ZI)

Percentage Holding: 2.2%

Last Quarter Holding Percentage: NEW

First Buy: 12/10/2021

Last Buy: 12/15/2021

P/L %: 3%

Why I Invested/Q4 Update: ZoomInfo was a company I really respected for their strong bottom line margins being a bootstrapped company, but thought it was relatively gimmicky with what they did and borderline unethical. After reluctantly listening to a couple podcasts on them, I felt I needed to at least further look into ZoomInfo and I was quite happy I did.

What surprised me is this is a very acquisitive company where they’ve done a couple large (and wildly successful) deals over their company life. Their newest M&A deal of Chorus.ai is another extremely exciting one and I think ZoomInfo is really doing something with crafting the next age of B2B sales technology.

My Plan Moving Forward: I think the overhead inherit risk that ZoomInfo has with their data extraction practices are enough for me to never let this become a larger than 5% position, but is still one that I think that can become a fruitful investment over time with their Founder/CEO leading the way.

Snowflake (SNOW)

Percentage Holding: 1.9%

Last Quarter Holding Percentage: NEW

First Buy: 12/3/2021

Last Buy: 12/3/2021

P/L %: -1%

Why I Invested/Q4 Update: As I become quite entrenched with high performing software companies, I started going back and forth on when does Snowflake become worth it as an investment, or do I just close my eyes and hop on the train. This companies fundamentals are incredible when you think about the scale the company is growing triple digits at.

My Q3 update thread on Snowflake probably does the best job encapsulating why I decided to begin a small position, and I think their runway is all to large in data for a young investor like myself to not be apart of (with discipline).

Also another highly recommended read on Snowflake is another special from Peter at Software Stack Investing

My Plan Moving Forward: When I started my small position, I told myself I wouldn’t add to it until it dropped under $300 (which it almost did before blowout Q3 earnings). I still feel like that’s my best plan but I’m becoming more tempted to add to this position as I thought their last quarter was that good.

Braze (BRZE)

Percentage Holding: 1.8%

Last Quarter Holding Percentage: NEW

First Buy: 12/21/2021

Last Buy: 12/29/2021

P/L %: 4%

Why I Invested/Q4 Update: Braze is new Q4 IPO like Freshworks is, and really caught my attention with their first earnings report as a public company. When I first learned about this company when it first listed I thought to it as a pure play on Twilio Engage. After digging further from there this is more of a complimentary piece to Twilio Segment and they actually work together on the data streaming and are technology partners.

This dynamic is a reason why Braze won’t ever having incredible gross margins as it’s working through multiple different players to provide its services, but has actaully seen gross margins expand from 65% to 70% this past quarter, while accelerating gross profit growth 59% → 62% → 79%. They mostly are involved with large enterprise customers for their services (Braze was built on mobile customized push notifications) and have increasingly strong sales efficiency as scale. Their GM Adj CAC Payback period has gone from 24.5 months to 13.5 months while overall CAC has dropped over 60%.

My Plan Moving Forward: This is a company I’m quite excited about as they move to offer more full brand engagement services outside the core push notifications for mobile, and I think is a great compliment to owning Twilio in my portfolio.

I’m not sure this ever becomes an outsized position but I plan on continuing adding to it over time as it’s still a very new IPO and we need to get through key events like IPO lockup.

SentinelOne (S)

Percentage Holding: 1.5%

Last Quarter Holding Percentage: NEW

First Buy: 12/6/2021

Last Buy: 12/16/2021

P/L %: 6%

Why I Invested/Q4 Update: SentinelOne was once an extremely high flying, nose bleed valuation IPO that has since had a couple earnings reports under its belt and a multiple compress significantly. The core cybersecurity tech for SentinelOne seems to be the strong point with much easier billing setup for SMB and mid market customers than a solution like Crowdstrike.

They as well have accelerating key fundamentals that get me excited to own this name into the future, although they do experience some small base effects like dLocal (newer companies really ramping up). That said, there’s no taking away from a company being able to scale with gross profit growing 32% sequentially and 44% the quarter before that. Seeing their gross margins expand from 54% to 64% in under a year was pretty eye opening to see the benefits of scale for SentinelOne.

My Plan Moving Forward: This company is still quite expensive no matter if it’s growing at an incredibly pace, so I’m quite cautious with how I approach building this position out (hence why it’s my smallest position). This is another complimentary pair I have in my portfolio with Crowdstrike and feel like these two will cover my bases to a strong macro trend with next gen cybersecurity.

SentinelOne execution from their first two public reports have been everything I could ask for and have little doubts I’ll be increasing my position over time in them.

Top Picks for 2022

This is more for fun and something I think I’ll enjoy looking back on. Please don’t take investing advice from me, I’m just some guy. My top picks reflects how I view my positions I take now by pairing two complimentary stocks together. I’ll be averaging the performance of both and comparing it to the S&P 500.

I think I’ve reflected on each of these companies enough in the above sections for you to understand why I’m quite bullish on these company’s outlook for 2022. I’ve also ordered them in confidence of outperformance for added fun:

Datadog (DDOG) & Snowflake (SNOW)

Alphabet (GOOG)

Twilio (TWLO) & Braze (BRZE)

Sprout Social (SPT) & Sprinklr (CXM)

Hubspot (HUBS) & Freshworks (FRSH)

Bonus prediction: S&P finishes up 10-15% for 2022 and most of software outperforms it.

Newsletter Schedule for Q1 2022

January 16th - Sector Analysis

January 30th - LinkedIn Company Insights

February 13th - General Analysis

February 27th - TBD Deep Dive/Company Overview

March 13th - Portfolio Companies KPI Update

March 27th - My Portfolio & What I Learned

Thank you all for making 2021 such a special year, and cheers to another great year ahead in 2022.

- Sean

Sean, have you looked into $ZS within the cybersecurity sector? Another stellar company with:

- Leader within the fastest-growing segments of enterprise security. (ZTA, SASE, ZIA)

- Clearly differentiated, cloud-native moat

- 71% billings growth and 62% YoY on $1B ARR on 30% FCF