Q3 2022: Portfolio Update

The Jiggy Capital Newsletter #18

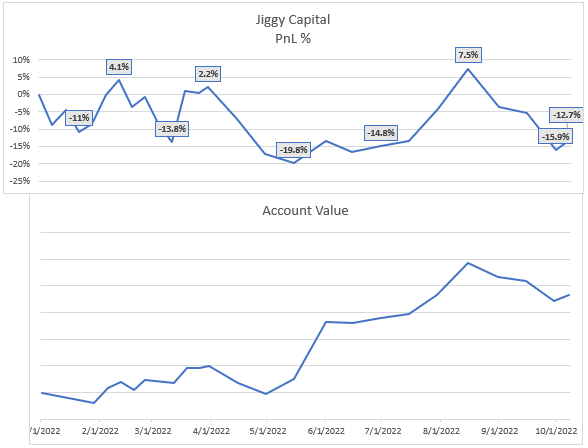

Performance

Let’s just get into the good stuff first and then I can ramble on about it for the rest of the post below, sound good?

At -15.9% YTD at Q3 end and -12.7% YTD as of October 7th market close, I’ve been able to outperform my benchmark in QQQ 0.00%↑ — -33.6% YTD — while owning many companies that have actually done much worse YTD than QQQ.

The main reason for this is due to where I’m at in my young investing and professional career at 25, where I’ve prioritized a high savings and reinvestment rate from my day job. Also worth mentioning I had a 401(k) rollover from an employment change almost perfectly at the bottom in May on May 17th which was extremely lucky timing.

There’s another small angle to that relative outperformance due to how I’ve been able to make meaningful buys near local market lows due to literally buying when I want to cry and delete my portfolio haha — and then taking wins trading around a core position.

General Commentary

In my end of 2021 portfolio recap post, one of my goals for 2022 was to think of my previous self as a complete idiot in at least two iterations. I can confidently say I’ve accomplished that sitting here in October lol.

One of my favorite parts about being as transparent as I am on my twitter account is how I’m easily able to remind myself how many god awful companies I’ve deluded myself into owning over my almost three year investing career. I mean, I still owned Lightspeed (probably my biggest loser ever and only individual write up) in size at the beginning of this year which really makes me laugh.

From an extremely hot two years of market gains into this certified bear market — 2022 has been yet another speed run lesson of full market cycles, bear market dynamics, owning actual quality companies, and to have a much shorter leash of investable ideas.

I feel like the most valuable effect this year has brought my investing thought process and expectations is just how humble I think about target returns and what I strive for. Easy evidence of this in practice for me is owning multiple ETFs and two of them being equal weight S&P500 and Nasdaq-100 index (the proverbial white flag haha)!

One of the things I've focused on the most is to keep a positive mindset throughout this all while being so young and able to buy the proverbial dip. This market drawdown has given me the opportunity to buy into more traditional “compounder bro” stocks that have traded at 60x+ NTM P/E over the past two years that are back under 40x P/E — and in some cases much lower. Examples of this are MSCI 0.00%↑ MA 0.00%↑ CMG 0.00%↑ ASML 0.00%↑ CRM 0.00%↑ SNPS 0.00%↑.

These are companies that I'm all quite excited to own and are a much different kind of investment that I was interested in for all of 2021, and has been a welcomed change of heart for me! Buying these more mature companies from above that are still compounding EPS close to 20% annually or more, then mixing in buying the more typical hypergrowth companies on occasion with fire-sale market volatility has been my formula 2022 — but worth noting I say this still being negative on the year lol!

My plan for the rest of the year is to continue my bi-weekly deposits with at least 75% of that going to the three ETFs I own. I’ll continue to deploy moderate leverage into my taxable account which has much less risk-on investments.

Currently I’m 115% long in my taxable account where I use that leverage but only 106% overall when accounting my HSA, Roth and Traditional IRA. The most I’ve gone on margin for leverage is 125% net long in my taxable account which translated to ~111% overall long, and I own only “risk-off” stocks and ETFs in that taxable account on margin.

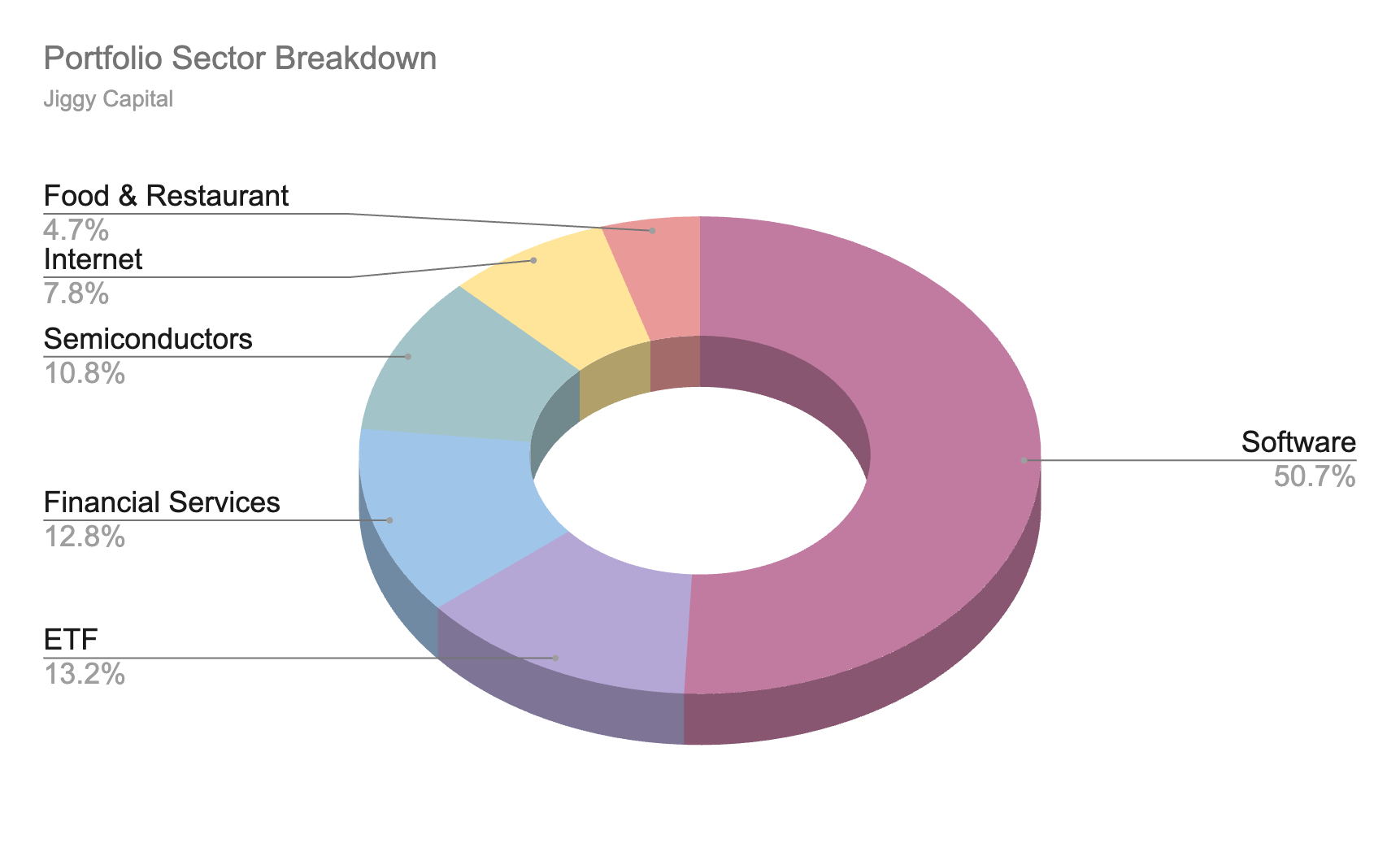

My Portfolio

I’ll be keeping my commentary on individual position brief in this Q3 portfolio update, and I plan on really diving into how I think about each position in detail in my year end 2022 portfolio review post!

My sector weightings have been pretty steady at large since my 401(k) rollover in May with the newest edition being the ETFs. Anywhere from 50%-60% of my portfolio in Software is my target range, and this is actually the lowest it’s been in a while since building out those recent ETF positions.

Last thing worth mentioning is the natural predecessor of a 401(k) rollover, I had an employment change going from selling shredded cheese bangs and coffee bags at a flexible packaging company to now selling software at a public company. I have what would be a ~13% position in my ESPP from that company, so like most my employer is my pseudo largest individual position.

ETFs:

Like I alluded to in the general commentary section, I entered three ETFs this quarter and plan on keeping these as a stable for decades to come. I personally think an equal weight approach to the market indexes will outperform, just given my personal views of some of the top weighted companies.

I also feel this gives me a much more well rounded portfolio having equal weight into many companies I wouldn’t normally buy (RSP is much more healthcare and industrials heavy than SPY for example). Building a solid base of ETFs puts me at ease going into Q3 earnings season where I’m sure there will be many wild individual moves as guidances update.

S&P 500 Equal Weight ETF RSP 0.00%↑

Fundamentals Snapshot:

Nasdaq-100 Equal Weight ETF QQQE 0.00%↑

Fundamentals Snapshot:

iShares Expanded Software ETF IGV 0.00%↑

Fundamentals Snapshot:

Equities:

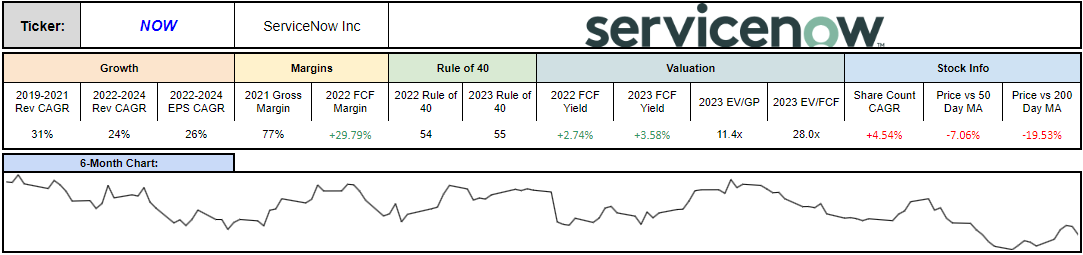

ServiceNow NOW 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: ServiceNow has been going back and forth as my largest position with Datadog for most of this year, and is a company I’ve built quite a strong level of conviction in.

On a relative basis I feel quite good about the value proposition ServiceNow brings to large-enterprises driving their digital transformation, and really being a deflationary platform doing more-with-less and automation. ServiceNow also continues to increase the breadth of their Now Platform with increasing investment into more adjacencies such as observability.

Overall, I would say that Bill McDermott is one of the people I feel safest putting my money with among SaaS CEOs in this environment. This is a company trading at 28x 2023 FCF and 48x Fwd P/E, both of which are basically the lowest ever for ServiceNow as a public company (the low is ~45x Fwd P/E in late September).

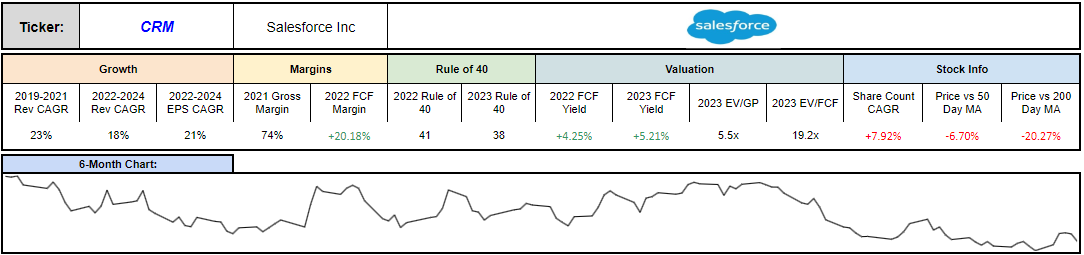

Salesforce CRM 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: Salesforce is making the painful transition of a compounding growth story rewarded for top line metrics — to a more mature state company of returning FCF to shareholders and becoming more thoughtful about general expenses. In other words becoming adults.

I’ve consciously turned this into a meaningful bet for my portfolio, and think this will be a company we look back on at how cheap it ended up being. The market really just doesn’t believe Salesforce is serious about making the necessary changes it needs to, while still making those lofty FY26 targets.

It’s funny how much of a fan I am of everything Saleforce is doing with Slack, and think their announcement of Genie is a really powerful data tool for the overall Salesforce platform and value proposition.

Salesforce is probably the primetime example of a company that will benefit from the trend of SaaS vendor consolidation at the enterprise level moving away from point solutions, and think that is an under-appreciated tailwind.

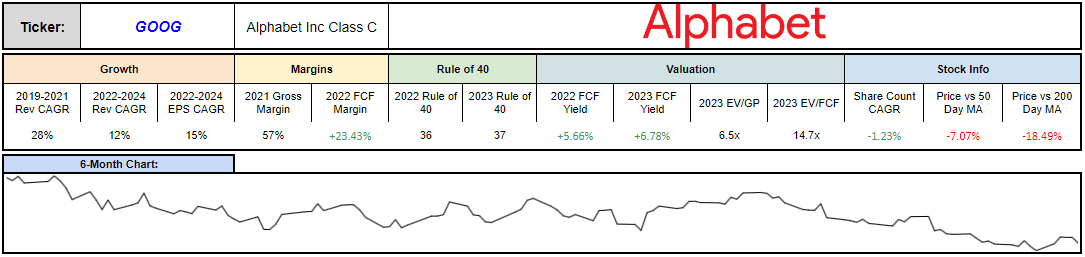

Alphabet GOOG 0.00%↑ GOOGL 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: Alphabet is a company I’ve proverbially ate shit on since entering in August of 2021 (my longest standing position LOL). I really try and not lose too much sleep over this position at <15x 2023 FCF, and feels like it’s completely macro driven how this stock will perform moving forward.

I’m still very much at peace with my mega cap choice of Alphabet when I decided I wanted to indefinitely own one in July of last year, and this is really my only internet long after briefly going long Meta for about a month in August, and Amazon for a brief bit in June.

Datadog DDOG 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: Datadog has been one of the few mainstays in my portfolio over the last year, and is a company I’ve only increased my conviction as I get more earnings reports under my belt. I’m a firm believer that Datadog is the true gold standard of SaaS financial metrics, and are actually GAAP profitable on a TTM basis while growing 70%.

Datadog executive team have always shown to be adults in the room with thoughtful spending, and is a company I feel quite comfortable with owning in size at these valuations. At their core they’re selling into Mid-Market and Enterprise companies with a strong self-serve motion for startups, and think the driving forces behind their business will prove to be durable even through uncertainty over this market cycle.

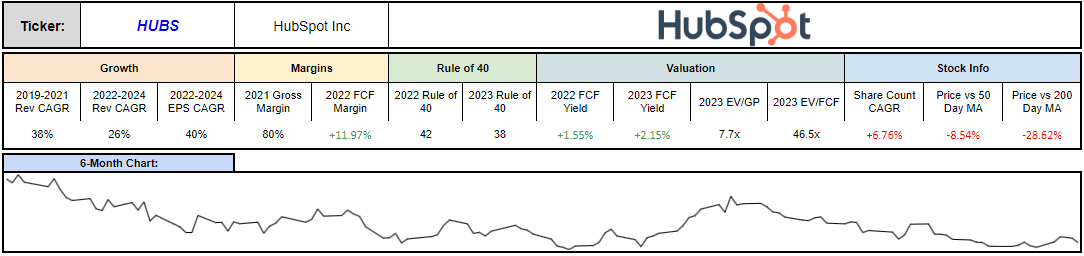

HubSpot HUBS 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: HubSpot has sat in the top echelon of my portfolio for most of this year, which has proven to be a painful experience haha! Even through that my conviction in HubSpot has increased, as I really think they will be a big benefactor of that SaaS vendor consolidation push I already mentioned with Salesforce.

HubSpot is another innovation-first company where they’ve built out quite the application software platform for all types of use cases. It’s (now) not a hot take to actually call them the Salesforce for SMBs with the full platform breadth they have, and they’ve increasingly have shown success going upmarket.

It’s unfortunate they didn’t guide to incremental non-gaap operating margin gains at their 2022 Analyst Day, which has really stayed the same since 2019. If they can drive any sort of upside there in 2023, I think this stock presents quite a nice opportunity for the value proposition they provide businesses in this macro environment.

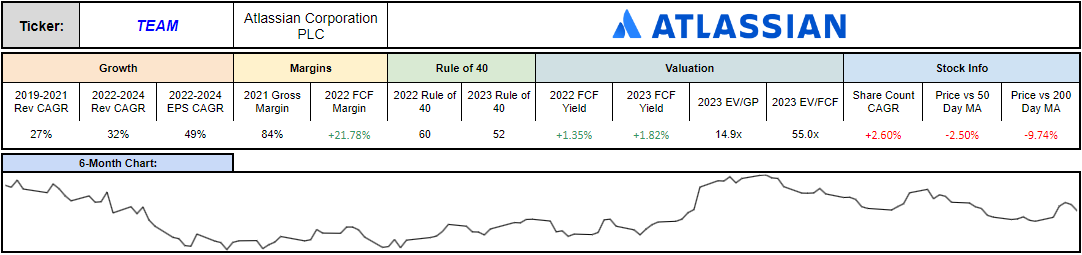

Atlassian TEAM 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: Atlassian is a company that I really struggle with how I think about position sizing. I’m such a big fan of everything Atlassian does and their similar R&D prioritization to Datadog, and think they still have tons of runway with JSM and their whole suite of products in general (new ones like Atlas seem interesting). BUT — this is a $58B market cap company that won’t have anything close to GAAP profits for what sounds like at least a couple years as they continue to prioritize investing in the business.

I hate to say it since again it’s such a great company, but investing in Atlassian in size just feels like a confidence game that you think TEAM will still fetch a top 5 SaaS multiple indefinitely in the future. It’s funny because as you can see from my buy/sell history on the stock this year it’s absolutely been one of my winners with how much I bought in May and then sold in July and August.

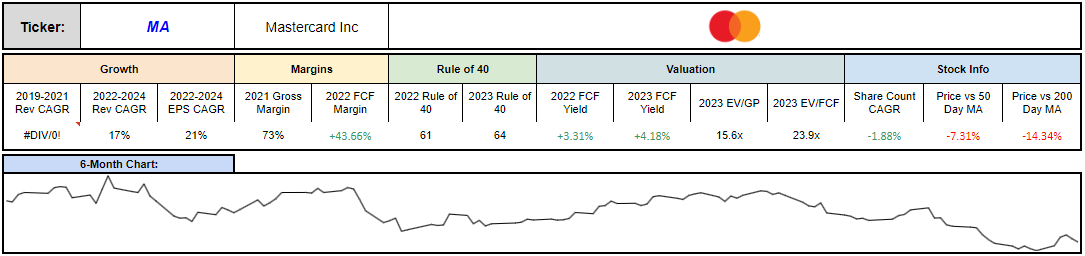

MasterCard MA 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: I’ve gone back and forth quite a bit on the payment rail titans this year where I started out owning Visa, then owned both Visa and Mastercard, to owning just Mastercard, and recently reducing that position out of the top echelon of my portfolio.

The reason for the last nugget is I do think there is a chance we see a recession affecting consumer spend — and I mean c’mon so does the market with how they’re trading both Visa and Mastercard. Regardless, Mastercard is a company that I plan on holding indefinitely for decades to come where I don’t see their moat ever becoming seriously challenged in a way they won’t ultimately benefit from (or shareholders).

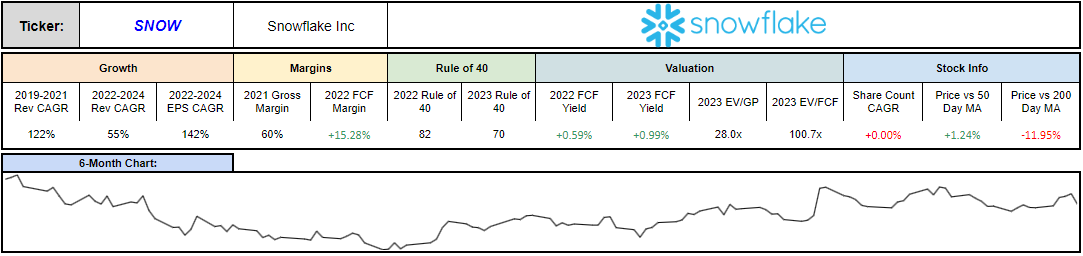

Snowflake SNOW 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: If I’m out here calling Atlassian a confidence game, Snowflake is the definition of a confidence game lol. As you can see, this has been another one of my best winners YTD with how I’ve traded the stock around my core position.

I tend to agree with the market participants that have decided to give as much bid support it’s gotten, and is one of the few software companies hedge funds have really accumulated this year as it sold off. Snowflake has showed they are viewed as a mission critical platform to all the kinds of companies they serve, and have continued to show incredible success with their enterprise and >1mm ARR customers.

At 100x 2023 FCF and $56B market cap, I am realistic with what returns I can reasonably expect here, and have reduced my cost basis % as the year as progressed. I genuinely think this is a company that can out-innovate market expectations for many years to come, but that’s somewhat of a confidence game in itself haha! They are really challenging the way data applications are traditionally made, and think that will prove to be a very disrupting force.

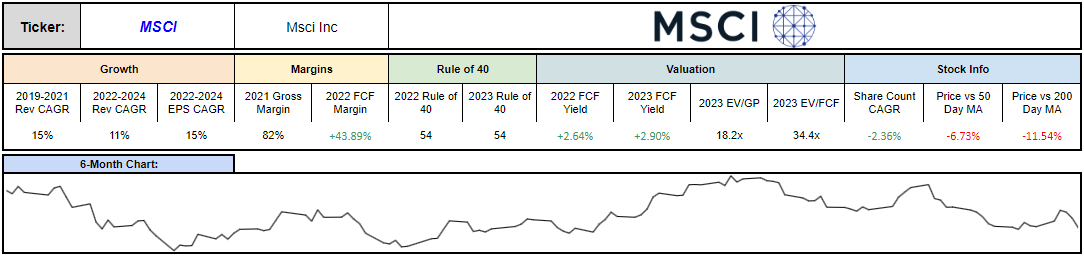

Msci MSCI 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: This is another 401(k) rollover addition and is a stock I feel like I should’ve owned a while ago. MSCI is such an interesting company being levered to AUM benchmarked to their ETFs, a great information services arm and pristine financials.

My knowledge of this company is still building, but this is a company that should compound EPS at 15%+ for many years to come. Valuation is much more reasonable at 35x Fwd P/E than it has been for much of the last three years (although this got into 20’s back in 2018).

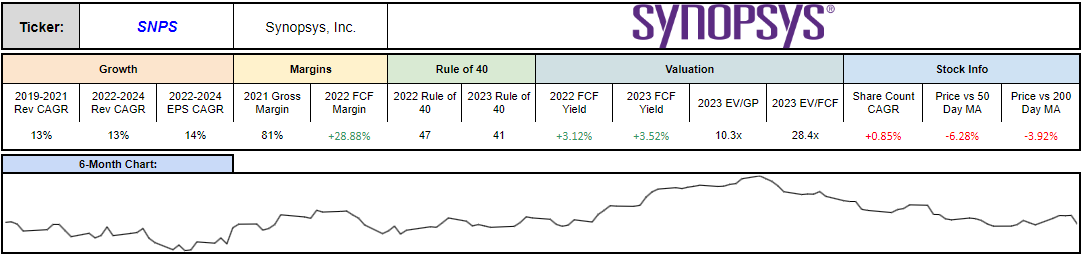

Synopsys SNPS 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: Synopsys is a fun company where once I understood what they did as a business, I almost immediately decided to start a position back in March. One of the biggest pleasures of following this company is listening to the great founder and CEO (of almost 40 years) Aart de Geus.

The software design layer to the semiconductor value chain seems to be about as durable as one might expect being tied to R&D instead of CapEx. Semiconductor companies have continued to say they will not be contracting R&D spend irregardless of demand, because that is how these companies come out better on the other side of this cycle!

Another sneaky angle to Synopsys outside of their EDA and IP business lines is their Software Integrity arm, where they have a portfolio of DevOps tools in spaces like Application Security Testing (AST).

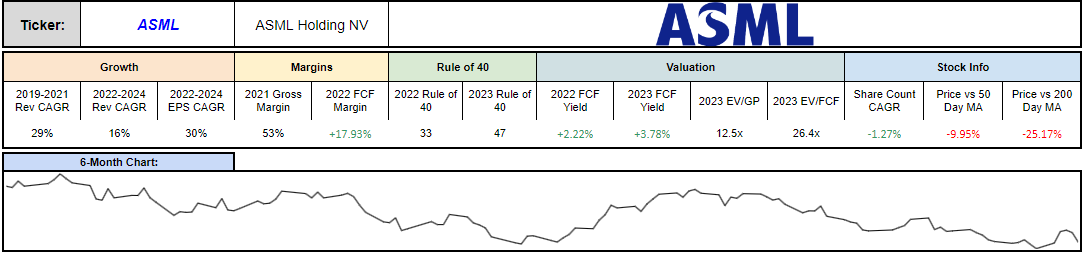

ASML ASML 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: ASML being my only SemiCap in the portfolio was a funny road to get here where at one point or another this year I owned AMAT, LRCX and KLAC. Around the time of my 401(k) rollover in May, I decided that with the market selloff that ASML presented the most attractive company to invest in between the group.

The one thing about ASML is investors really don’t have to worry about demand for their products, given their market presence as a monopoly in EUV and market leader in DUV. Given also the amount of Fab buildout we will see in the EU & USA for strategic reasons over the next decade (and APEC will still have serious capacity buildout like always), it feels the driving forces behind ASML are special to the rest of semiconductor companies who will be facing demand challenges.

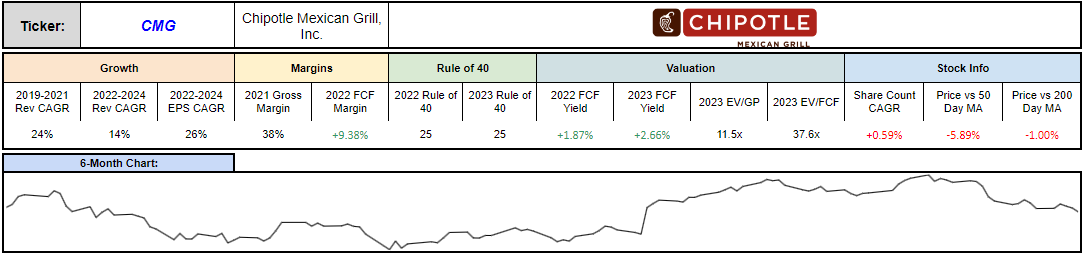

Chipotle CMG 0.00%↑

Company Snapshot:

Fundamentals Snapshot:

Commentary: I find great humor in Chipotle — a burrito company — being my best performing stock this year. This was a 401(k) rollover addition to my portfolio in May, and is a stock I’ve always followed since I first started investing due to my deep love for the company as a consumer (I actually briefly owned this stock back in early 2020).

Chipotle is a stock where it feels like as long as they make incremental margin gains, the stock will keep going up lol. Their unit economics are unchallenged, and their model of owning all Chipotle stores has proven to be a winning strategy in challenging macro/commodity environments, where they have much more control at the store level.

I will say as a consumer their quality of experience as drastically dropped over the last five years or so, and I’m not sure their price increases will prove to be a sure thing on keeping customers around. I think they’ll come to find a balance in all of that, but I’ve actually reduced this position pretty considerably over the last couple months for that reason (and the valuation has quickly gone back to relatively expensive).

Conclusion

If you’ve made it this far — seriously bravo and I appreciate you. One thing I’ve always tried to be is open minded and humble to how much I don’t know and how much of an idiot I still am while having the time of my life investing.

If you look at my early 2021 tweets and portfolio updates, it’s pretty stark to see how much of a different process I have now and just how different I think about companies. I think this is just the natural progression of an investor figuring random things out piece by piece day by day, and the compounding nature of that.

I feel I’ve put myself in about as best a position so succeed with my current portfolio as I have ever previously done. I’m at the point where focusing on maximizing my returns at my day job is the most impactful thing I can do for my portfolio, and just keep chipping away at that with my high reinvestment rate.

I hope this was a semi-coherent post and gave a better insight into my portfolio and how I think about things, and I plan on posting a much more detailed portfolio update at the 2022 year end version.

- Sean