Q3 2022: Earnings Review

The Jiggy Capital Newsletter #17

In this newsletter I will be highlighting various earnings reports of the companies I own in my portfolio.

The length of each company’s write up section will vary on the amount of KPIs the company discloses and the amount of good insights to share from their numbers. My hope is you’ll get an idea of how the company performed against expectations, the trends behind their numbers, some quotes from the Q&D portion of their earnings call, and my personal take on the quarter.

This newsletter edition is mostly about just the raw numbers and performance, and I walk through my portfolio decision making and thought process in my quarter-end Portfolio Reviews.

If I had to segment the quality of reports between the remaining nine companies, it would go as follows:

Great: MA 0.00%↑, TEAM 0.00%↑ , SNOW 0.00%↑

Average: MSCI 0.00%↑, CMG 0.00%↑, HUBS 0.00%↑, DDOG 0.00%↑, TOST 0.00%↑

Not So Great: ASML 0.00%↑, NOW 0.00%↑, CRM 0.00%↑, GOOG 0.00%↑

Although I try to stay objective when assessing progress of companies I own, I’m no doubt biased when I say I honestly thought all of the reports were quite solid with pockets to get really excited about in each.

I’ve not included any recent additions to my portfolio such as META 0.00%↑, DOCN 0.00%↑, TWLO 0.00%↑, who will all be in my next quarter's Earnings Recap.

Now let’s get into individual reports!

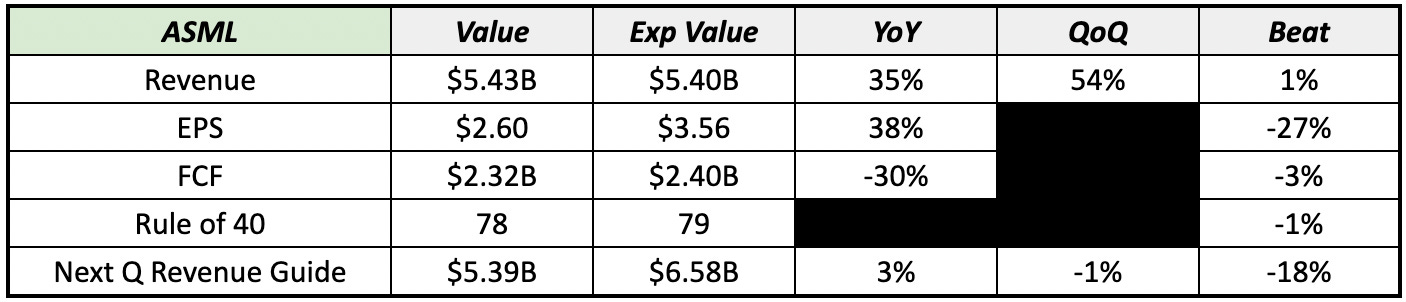

ASML ASML 0.00%↑

The Numbers:

Earnings Call Quotes:

In an effort to recover from these delays, we are increasing the number of fast shipments to get systems to customers as quickly as possible. And as a reminder, a fast shipment process skips some of the testing in our factory. And final testing and formal acceptance then takes place at the customer site. This leads to a deferral of revenue recognition for those shipments until formal customer acceptance but does provide our customers with earlier access to wafer output capacity. As fast shipments delay revenue recognition to subsequent quarters, we are seeing more delayed revenue that will move into next year.

The value of fast shipments in 2022 leading to revenue recognition in 2023 is expected to increase from around €1 billion, as previously communicated, to around €2.8 billion, an increase of €1.8 billion. This then also leads to €1.8 billion lower revenue recognition in 2022 and we therefore now expect year-on-year revenue growth of around 10%. As a reminder, we began the year expecting a revenue growth of around 20%, or approximately €22.3 billion, and €1 billion value of fast shipments at the end of this year. We are now expecting a revenue growth of around 10%, which is approximately €20.5 billion, and €2.8 billion value of fast shipments at the end of the year. So, the total business volume for 2022 is essentially unchanged.

- CEO Peter Wennink

On difficulties with supply chain and what ASML is doing to combat that:

Yes. I think the delays in delivery times, we're trying to -- we're not trying, we're actually doing. We are helping our customers with the fast shipments, which actually means that if you look at our production value, so the value of the system coming out of our factory with and without fast shipments, that's actually, as I said, not as fast as we planned, but it's definitely growing. It is ramping.

So, the delay in the delivery times is really delaying the revenue recognition. I mean we are delivering. This is why we include -- this is why we go to fast shipments. And as we can point out and just looking at our production value coming out of the factory, the second half is higher than the first half. And this is also exactly why we are still working on getting a production capacity in our factory. That helps us to ship over 60 EUV systems next year and over 375 deep UV systems because as you pointed out, the backlog is there. And the customers say, "Whatever you do, please ship those systems." because we are under shipment -- we are undershipping the demand.

- CEO Peter Wennink

On current backlog:

Yes. So, the backlog of EUV is well over 100 at this stage. So, -- and we talked about EUV capacity for next year of over 60. Of course, we still have the second half to go. But yes, the answer is well, well covered for next year.

- CFO Roger Dassen

My Take:

This is a company where I’m learning an immense amount about the business in each quarterly report, since I’ve only owned this company for a couple quarters and ASML such a highly complex company.

I’m not sure if the company has outlined Fast Shipping and has reverted to using that in previous times of increased shipping time needs, but it seems like Fast Shipping is a pretty sleek way of keeping things moving out the door, although makes revenue recognition quite noisy.

The semiconductor industry is still quite chaotic and while ASML is a monopoly in EUV and still innovating in DUV, they’re not shielded from the cyclicality. I’m not a huge fan of their FCF takedown, although understandable.

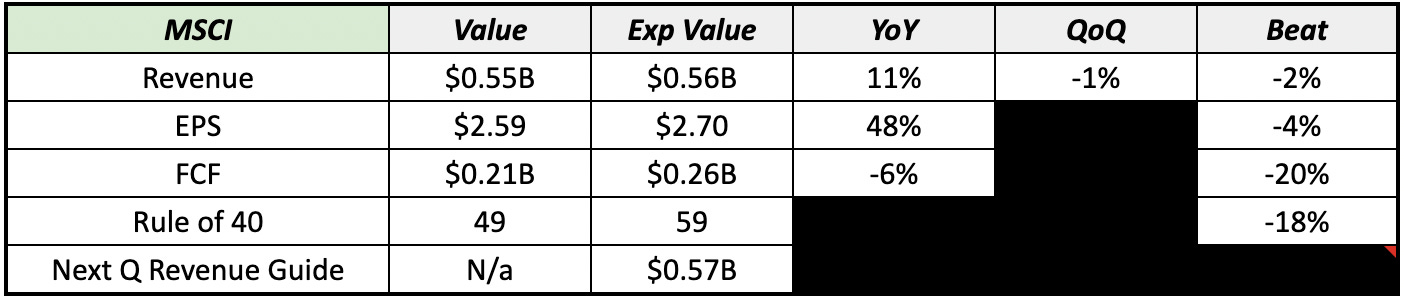

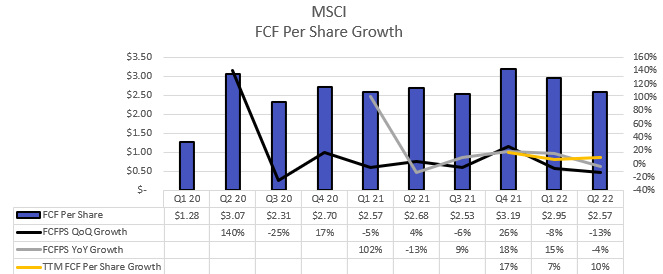

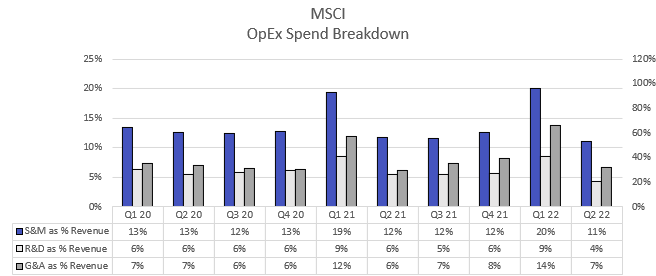

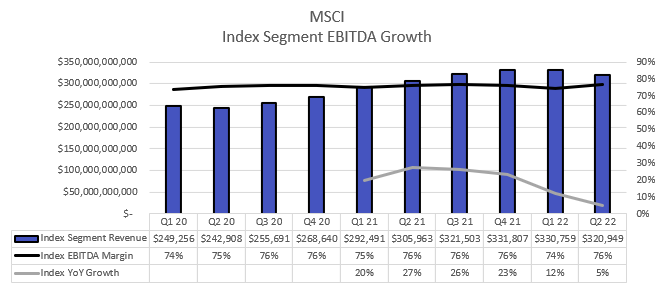

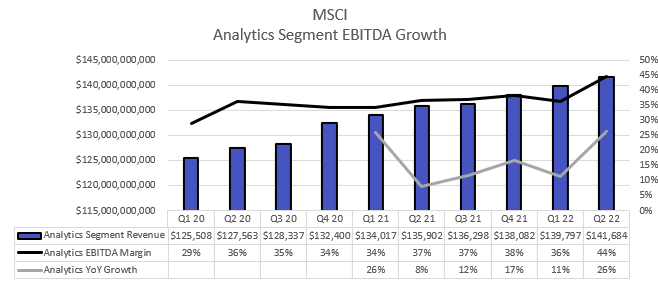

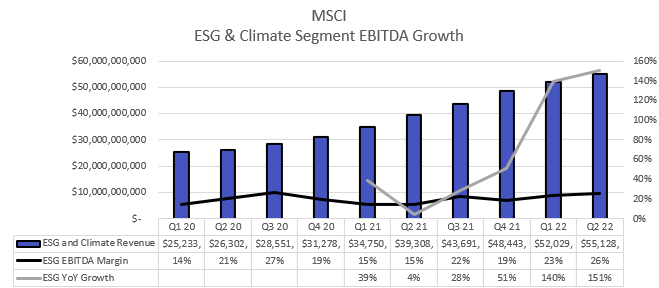

MSCI MSCI 0.00%↑

The Numbers:

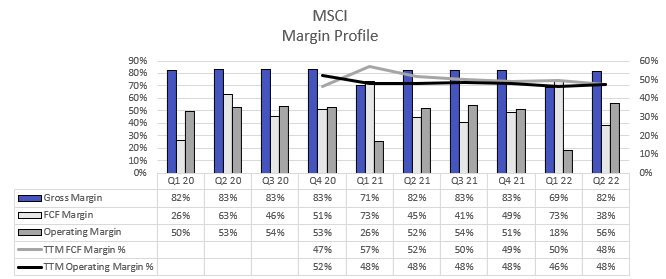

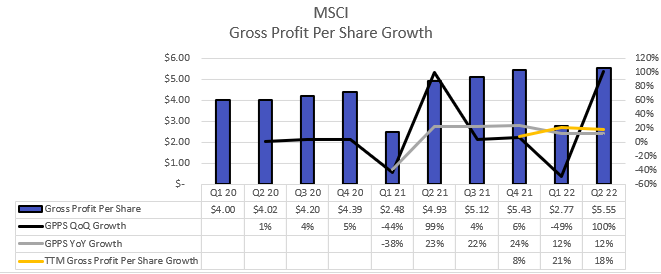

The Trends Visualized:

Earnings Call Quotes:

Should note that CEO Henry Fernandez is usually on earnings calls but evidently was feeling under the weather and couldn’t join.

On guidance assumptions for market outlook:

Before we open the call for Q&A, I would like to discuss our outlook for the year. We published our updated guidance earlier this morning, which reflects a cautious but constructive view on the balance of the year. While we expect some continued volatility, we expect generally flat to gradually improving market levels from current levels throughout the balance of the year. As mentioned earlier, we have begun to activate our downturn playbook, with a focus on flexing certain less critical expenses and moderating our pace of hiring in selected areas.

Fun Snowflake callout in Prepared Remarks:

In the second quarter, MSCI launched a series of new equity factor models, including the first models to offer sustainability, crowding, and machine learning factors. The sustainability factor includes both ESG and carbon efficiency components. This is a significant model update aligned with our strong index franchise. We will make these models available through several distribution channels, including Snowflake's Data Cloud.

Using Snowflake will help us dramatically accelerate the client onboarding process. We're also developing capabilities to create an even better user experience by combining analytical results from Risk Manager and BarraOne. This will greatly enrich our content and capabilities. We are further enhancing the user experience in Analytics through our Investment solutions-as-a-service applications.

On new business mix:

Roughly half of new recurring subscription sales were generated from emerging client segments, including wealth managers, insurance companies, hedge funds, broker-dealers, and corporates. And our climate run rate reached $55 million, which is an increase of 88% from a year ago.

- CFO Andy Wiechmann

On plan to action after Q2 market volatility:

We mentioned last quarter that if AUM stayed at current levels at the time or deteriorated further, we would likely go to our downturn playbook. From the end of Q1 to the end of Q2, we saw AUM levels drop about $200 billion or 14%. And as I mentioned, our guidance at the time, assumed markets remained fairly flat.

And so as a result, we're turning to our downturn playbook. Just to give you some color on some of the levers that we've been flexing here. We are moderating the pace of headcount growth on a very targeted basis. And so we are prioritizing our key investment areas to continue investing in, but other areas, we are slowing down the pace of growth.

We're also identifying efficiencies in less critical areas. We are selectively flexing down some of our discretionary noncomp areas around areas like professional fees.

But to Baer's point, I do want to highlight that our business remains healthy. Client buying behavior remains generally healthy despite the lower ETF AUM levels. And it's important to keep in mind that we have a global diversified all-weather franchise with a very strong subscription growth and retention rate here.

- CFO Andy Wiechmann

On raising $350mm term loan during the Q2 quarter:

Yes. So I mean, part of the rationale for raising the term loan, the additional $350 million, was to give us dry powder. We want to continue to be nimble on the share repurchase front. We think there are opportunities to get our shares at attractive values, but we also want to have some dry powder for bolt-on MP&A.

- CFO Andy Wiechmann

On ESG & Climate segment growth vs margin expansion outlook:

Obviously, we don't give margin targets by segment, but I would say that within the ESG and climate, our focus is really on driving top-line growth, not margin expansion. And so we're not targeting for the margin to expand from current levels. We're really trying to invest to continue to fuel that growth that you're asking about across so many different dimensions.

So the client segment dimensions, the asset class dimensions, the solutions dimensions and then really, really accelerating our growth in Climate, which we think is going to be a massive opportunity. And so our goal right now is leadership and growth. It's not on margin expansion within the segment. I would highlight that longer term, the nature of what we do in ESG and climate is similar to what we do across many other product areas, which is we develop IP and we sell it to many different clients for many different use cases across many different applications.

- CFO Andy Wiechmann

My Take:

Probably the most interesting part of this earnings report was that their ETF-based fees guidance included the assumption that markets stay flat for the rest of the year.

The actual numbers weren’t too strong which was to be expected given the large volatility we still saw in Q2 relating to ETF-based fees, but I will call out that ESG & Climate segment margin expansion and growth has been quite impressive, as shown above. Analytics segment also ticked up in growth which was nice too see if their core ETF fees are going to be unpredictable for the foreseeable future.

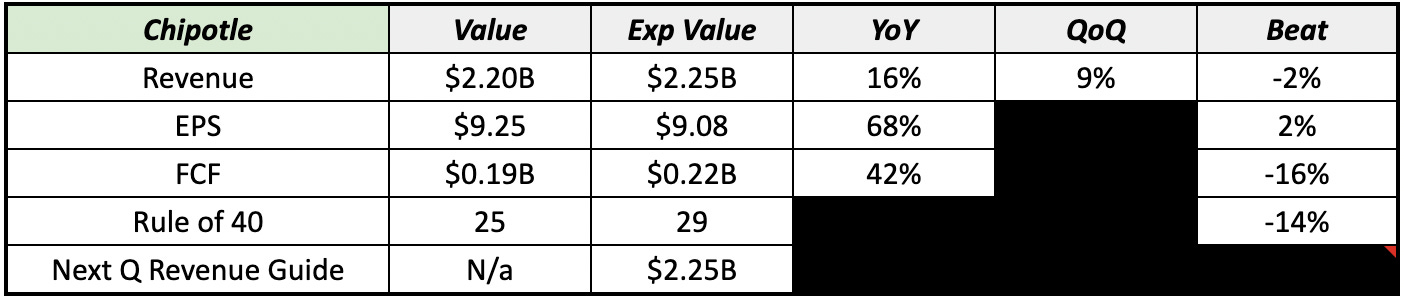

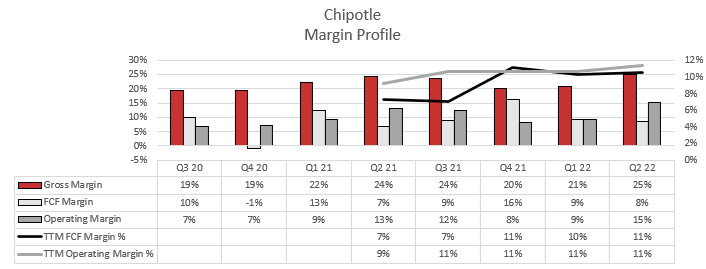

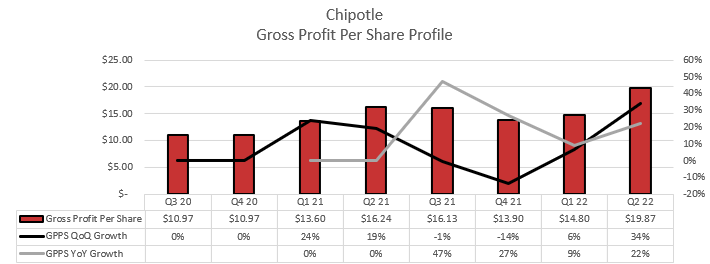

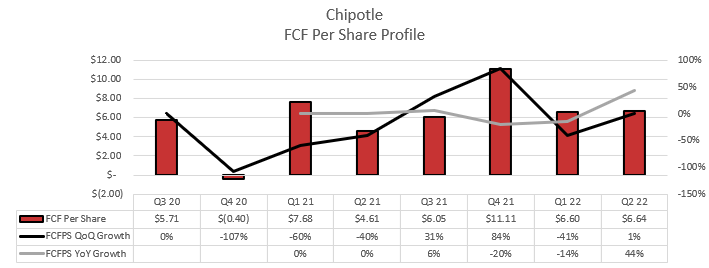

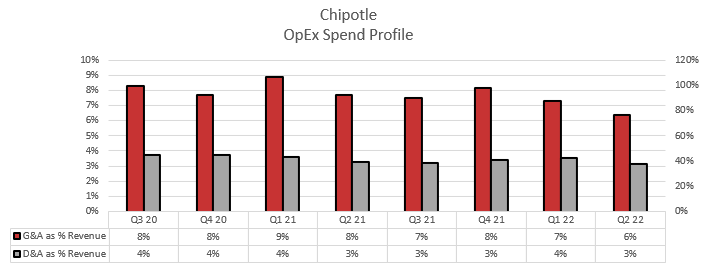

Chipotle CMG 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On current business environment into Q3:

I would like to spend a couple of minutes providing insight into current trends and our outlook. Regarding Q2, through mid-May, comparable sales were on track to reach the top end of our guidance range. Since then, the underlying trend has decelerated and we anticipate mid- to high single-digit comps for Q3 with planned pricing in August.

- CEO Brian Niccol

Rewards program launched in Canada and soon in UK & France:

Additionally, we're excited about the recent launch of the rewards program in Canada, which will provide another way for Canadian guests to engage with the brand and provide Chipotle with the ability to further delight its Canadian Rewards members. Finally, our digital ecosystem is rolling out in the UK, and France will follow shortly thereafter.

- CEO Brian Niccol

Further color on current business environment and seeing normalized college town summer seasonality for the first time in 3 years:

Regarding our sales trends. As Brian mentioned, we were on track for comparable sales to reach the upper end of our guidance range for the first half of the quarter. Since then, we've experienced a step down due to a combination of macro pressures, our ability to handle the growth with relatively new workforce and a return to normal summer seasonality for college-based restaurants. For perspective, about 15% of our restaurants are in college town, and we've not seen normal seasonality in 3 years.

- CFO Jack Hartung

On in-store dining surging effects on average group size:

Yes. David, the transactions were up in the quarter between 3.5% and 4%. We also had a mix shift. We didn't talk about that for a number of quarters now as our business has moved more towards in-restaurant. The average group size -- well, the mix shift was about a negative 6%. The average group size dropped by about 4.5% and that drop is mostly a drop from the business moving from digital into in-restaurant.

So, as we move to Q3, we do expect that -- because of the downturn that we saw the macro effects in the second quarter, we do think that transaction comp will ease a bit, but we also think that the negative mix shift should ease a bit as well.

[After follow-up on if transactions will go negative]

David, it's going to be right around slightly positive or right around flattish, right around in that range.

- CFO Jack Hartung

On the planning pricing increase that went into effect in August:

Yes. What we've seen is -- unfortunately, a lot of things have stuck versus gone away as far as inflation. And then we've got some key items that have frankly continued to be inflationary. And I think Jack highlighted it right. We've got avocados, we've got dairy, tortillas, some packaging.

So, unfortunately, we were hoping we'd see some of the stuff pull back. We haven't seen that. But there are other parts of the business that we have seen plateau, which gives us optimism that, hopefully, we won't have to continue to pull the pricing lever. And I think you've seen this with us. We really do try to wait until we truly understand what feels like is something that's an ongoing cost that we need to handle with pricing versus, hey, we're going to wait this one out and see if it pulls back. So we figured best to share where our heads are on this one now.

- CEO Brian Niccol

On Restaurant AUV is now running at 2.8mm/store, the high end of restaurant peers:

Yes. Look, I think one of the things that truly special about Chipotle is we are not capacity-constrained with our front line or our digital make-line. So I mentioned, right, there's restaurants doing $5 million, $6 million, $7 million. And obviously, it presents an opportunity for us to build a lot more restaurants without having really any meaningful impact. But I think it also just demonstrates the four walls that we're already running Chipotle has tremendous upside as well.

So I'm feeling really confident we're going to get past $3 million, and I'm sure we'll probably be talking about how we get to $4 million at some point. But I first like to get past the milestone of $3 million. We can celebrate that milestone. And the good news is I don't see any capacity constraints that would prevent us from saying $4 million is next up.

My Take:

This is a company where they just continue to chip away at their long stated growth story playbook with these updates every 90 days. Chipotle is able to operate nimbly because of their store-owned restaurant business model, and the surge back of in-store dining was nice to see. This was the first quarter that more sales came from in-store vs digital in quite some time if I recall.

Their continued price increases is something that’s interesting for me to watch, as we will see how far they can push what is already easy to achieve a $20 burrito (delivery etc), but this could more be the consumer in me talking than the shareholder haha.

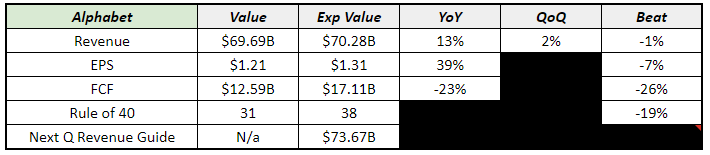

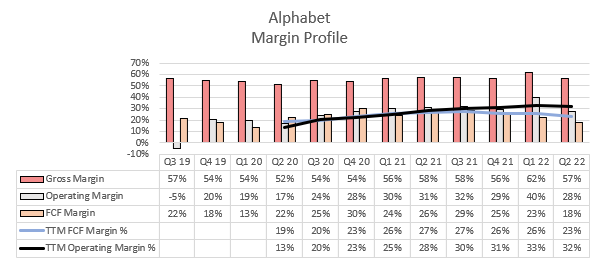

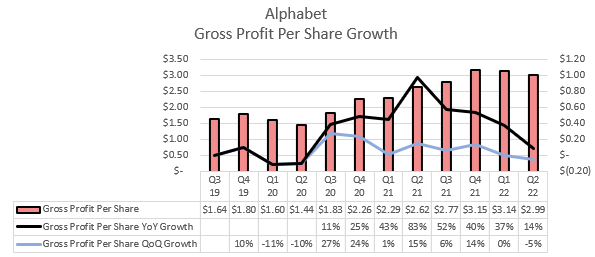

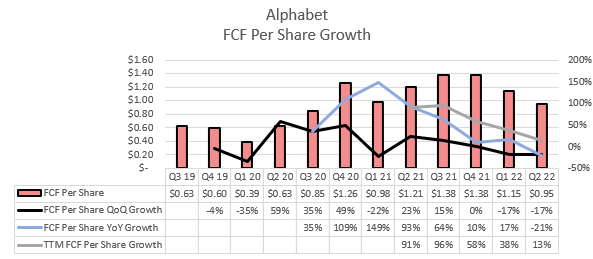

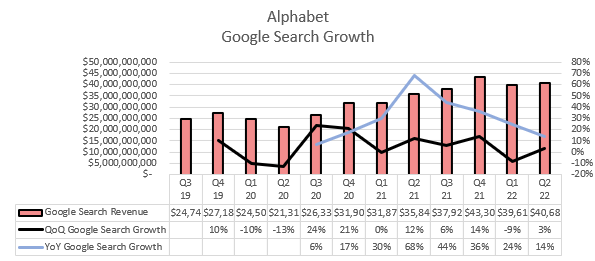

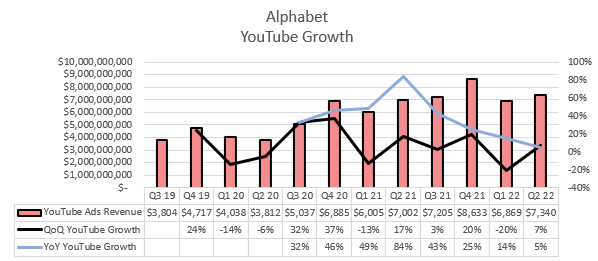

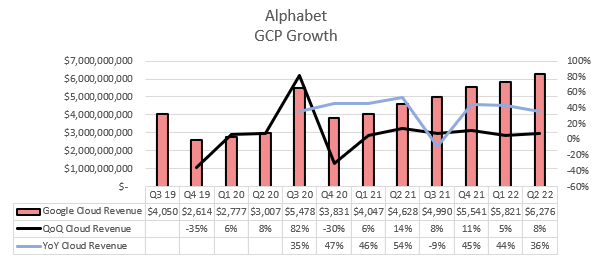

Alphabet GOOG 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On how the current macro environment is having Alphabet prioritize their investments:

As I said to the company, I think it's a good time to sharpen our focus. Personally, I find moments like these clarifying. It's a chance to digest and make sure we are working on the right things as a company with taking a long-term view, making sure we are continuing to invest in deep technology and computer science and doing differentiated work.

And it gives a chance to assess everything we are doing with the critical lens and reallocate resources to our most critical priorities. So it's a constrained optimization problem. I think it gives us a chance given the strong -- given a few years of strong growth to double down and focus and we're going to be very disciplined in terms of how we will approach it.

- CEO Sundar Pichai

On GCP:

On Cloud, we continue to see strong momentum, substantial market opportunity here and still feels like early stages of this transformation. Constantly in conversations with customers, big and small, who are just undertaking the journey. So it kind of shows you the opportunity ahead. I would just say nothing noticeable other than -- given we are in different geographies and different sectors.

You do see a varying mix of some customers impacted in terms of their ability to spend, some customers just slightly taking longer, longer times. And maybe in some cases, thinking about the term for which they're booking and so on. But I don't necessarily view it as a longer-term trend as much as working through the macro uncertainty everyone is dealing with.

- CEO Sundar Pichai

On growth opportunity vs margins improvement for GCP:

And then in terms of your margin question, our view continues to be that this is an extraordinary opportunity. It's a long-term opportunity and enterprise customers are still early in their move to the cloud. And so, we do very much have that debate that same question that you posed is the right one, which is a trade-off as between revenue growth and immediate profitability. And what we're focused on is ensuring that we're investing to support the long-term growth and given the upside that we see.

And so, continue to focus on it and are looking at the path to profitability, path to free cash flow positive to drive attractive returns. That's obviously in the overall model of it, but I very much believe in the long-term growth and believe this is the right level of investment across the business, go to market, the product teams continuing to build it out globally.

- CFO Rush Porat

My Take:

Overall I would say things aren’t too rosy at Alphabet and they know that. They’ve moved through some of their toughest ever comps post-covid and to me is now just a question of how macro impacts search strength. Cloud re-accelerating QoQ was nice to see, but YouTube slowing to 5% YoY revenue growth is pretty nasty, although on some pretty intense comps.

If this isn’t the bottom and things get worse for Alphabet in Q3, things could get hasty for the already troubled stock since they don’t provide any forward guidance.

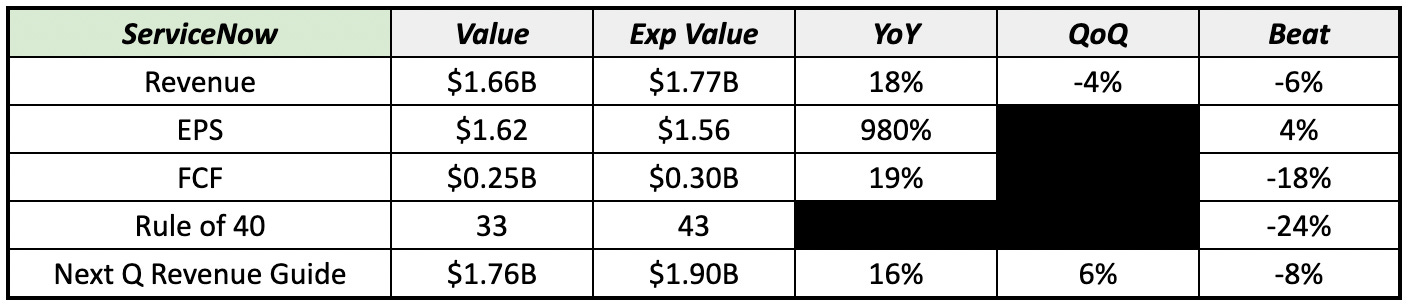

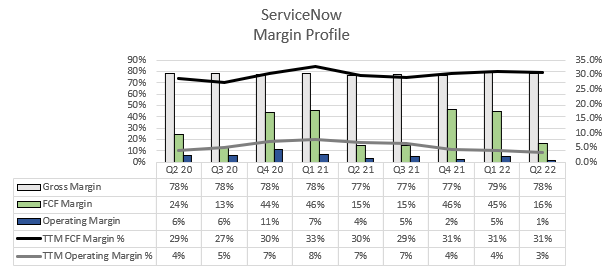

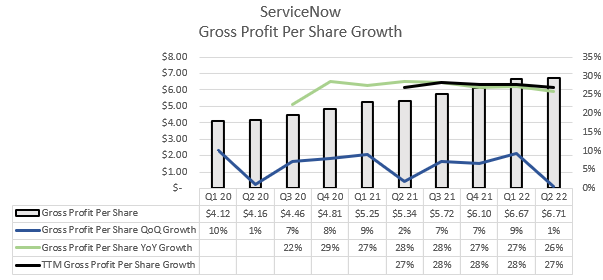

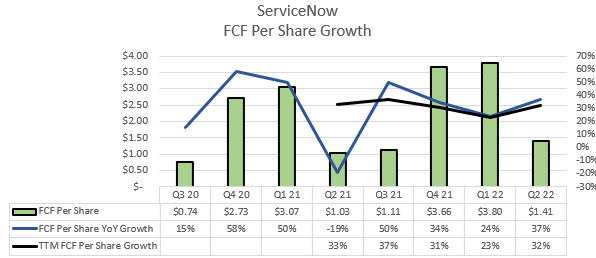

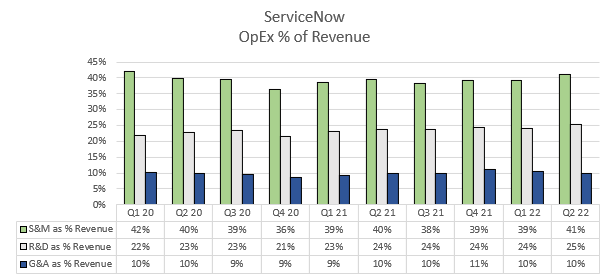

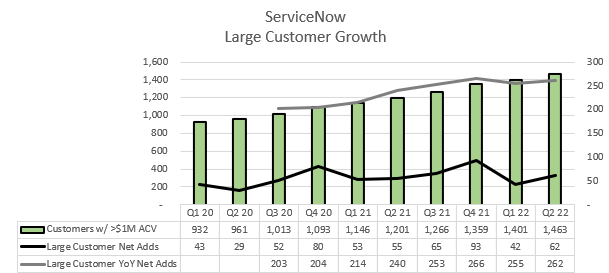

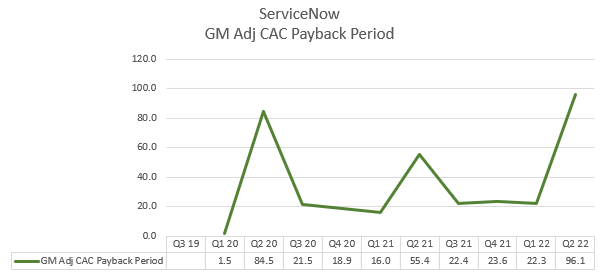

ServiceNow NOW 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On cRPO forward guide of 20% coming in a bit lighter than some might expect:

Sure, Kash. I'll take the cRPO question first. And if you remember, we've been talking about this for several quarters now that with the renewal cohort that Q3 was going to be the bottom, right? So if you think about a renewal of 1 million at the end of Q4, at the end of Q1, it becomes 750,000, end of Q2, 500,000, end of Q3, only 250,000, it'll pop back up in Q4. And so, Q3 is absolutely the bottom of that renewal cohort, and we'll see that reacceleration as we move into Q4.

- CFO Gina Mastantuono

On the strength of >$10 ARR ServiceNow customer group:

We're talking about making that amazing platform the business platform for digital transformation for the world's largest companies. And I think Gina pointed out the $10 million and above growing at 50% year over year. So even as you might need to wait a little bit longer in certain cases, when you do, it just gets bigger. And Kash, I think this is now the moment where ServiceNow really gets a big, big tailwind from a macro that forces customers to really think deeply about where they're spending their money.

And they're not interested in long drawn-out projects that might take multiyear to get there. They have to perform for the capital markets now. So we are bringing a calling card with the fastest ROI in the enterprise, hard stop.

- CEO Bill McDermott

On hiring outlook to have a full capacity for 2023 by Q4:

We will have a full capacity to achieve our '23 objectives at the Q4 mark. So please know that we're covered, and that actually intensifies along the lines of each month and this year to actually expand furthermore in our indirect or our digital sales effort. We're doing some very unique things there to not only cover existing but also to get net new logos.

- CEO Bill McDermott

On deal closing environment elongating, but still active:

What we also are trying to emphasize is that the deals aren't going away, right? They're elongated, but many of the deals that were elongated in Q2 have already closed in July. And so, those digital transformation tailwinds that we talked about, the platform relevancy that we continue to talk about is very relevant and as relevant as ever, which is why we felt very confident in reasserting our mid- and long-term guide of $11 billion by 2024 and $16 billion by 2026. And so, close rate, we are taking into account the macro environment that we see in place today.

- CFO Gina Mastantuono

On sales rep productivity compared to last year:

So I'll take the second part first, and then I'll pass it over to Bill. So sales productivity remains strong and is better this year than even last year. And so, we expect that to hold, Phil, and feel really good about where we're leaning. We certainly have continued to hire feet-on-the-street go to market.

- CFO Gina Mastantuono

Funny Wall St Analyst interaction from my first quotes on cRPO:

Question:

Thank you, guys, for for taking the question. I Gina, I think this one is for you and two for you. I think Kash was trying to put some words in your mouth and talking about sort of no change in the cRPO outlook for Q4. I wanted to ask you that question directly.

Like are you guys adjusting your view on sort of the cRPO growth that you're exiting Q4 with? And any chance that you give us that number, so we have more of a sort of a perspective on sort of how we're entering calendar '23?

- Analyst Keith Weiss

Answer:

So I think, Keith, listen, I'm not guiding to Q4 now, but what I wanted to make the point, and I think what Kash was trying to allude to as well is, is Q3 the bottom when we think about that renewal cohort and how do we think about the back half, right? And so you could imagine from our slight return to our January revenue guide that we are absolutely continuing. And I was very explicit in my script that we're factoring in throughout the back half of the year slightly longer deal cycles. And so, that will impact Q4 cRPO. But again, just a timing perspective, right, why we are also very confident in reiterating our mid- and long-term goals of $11 billion by '24 and $16 billion by 2026.

So I know you'd love to hear a Q4 guide. Give us a few more months, and we'll give it to you then.

- CFO Gina Mastantuono

My Take:

ServiceNow is usually the lucky first contestant of standalone enterprise software companies to report earnings. What was different about this earnings for ServiceNow is they had a huge selloff from a Mad Money interview where CEO Bill McDermott mentioned lengthening sales cycles.

With that out there going into the print, it still wasn’t too rosy even though I was told to expect macro effected numbers. What analysts and investors have talked about the most was a 20% cRPO forward guide which was below street expectations really showing that macro effected environment for ServiceNow. Overall this wasn’t a particularly strong quarter for ServiceNow, and in general for large multi-national enterprise software companies.

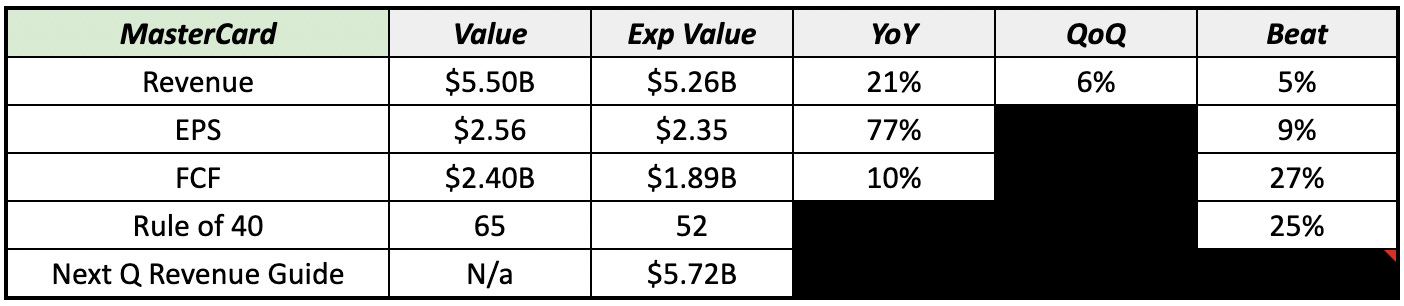

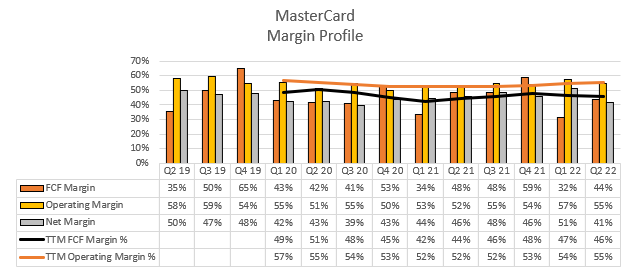

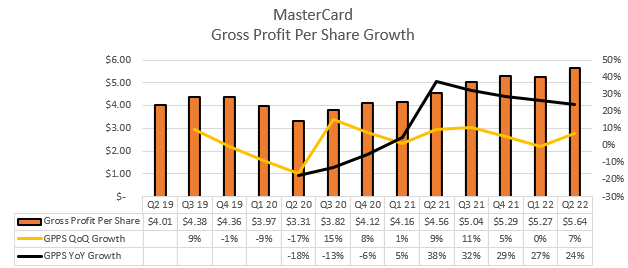

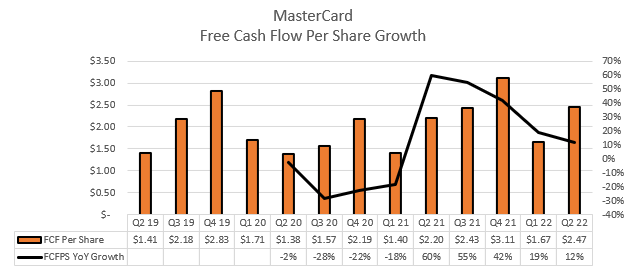

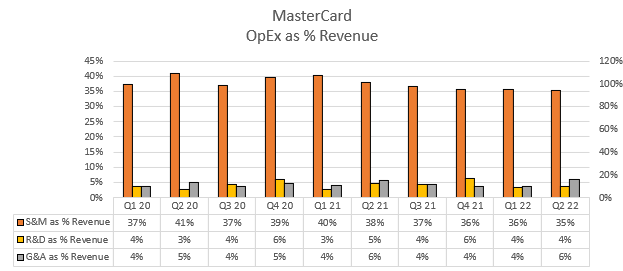

Mastercard MA 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On cross-boarder travel outlook and region opportunity in Asia-Pacific:

Sure, Sanjay. So what I shared was that we are thinking ahead in terms of cross-border travel seeing a modest improvement relative to 2019. And as you can see in our metrics, cross-border travel in Q2 was at 118%, and the first three weeks of July is at 126%. Without getting too specific as to what exactly we're building in there, the point we've got is the following: we expect a modest improvement in travel when indexed back to 2019, and it's predicated on certain data points.

And the data points are: if you think about what's going on in Asia Pacific, we've talked about how Asia Pacific from a cross-border travel standpoint has been lagging and has historically not come back over the last few years since COVID hit in the same way, say, as intra-Europe has come back. In fact, I shared with you the metrics as to where we stand from an inbound cross-border travel standpoint in Asia Pacific. So there's a lot of room to grow there. We think that opportunity exists.

- CFO Sachin Mehra

On why Europe has continued to perform so well in face of macro headwinds:

We're well-positioned with our tools in Europe, which is pushing on open banking, which is then pushing on open -- on account-to-account, which is pushing bill pay solutions. So we have all of that in the hop. So we feel that there is significant opportunity. And as I said before, there is uncertainty on the European macroeconomic front, but on the other hand, macroeconomic GDP, overall economy, in our baskets are two different things, and we'll have to kind of see how that will play out.

- CEO Michael Miebach

On increased non-GAAP OpEx spend forecast for the year:

Sure, Bryan. So a couple of things which are -- you're right. We had previously guided to high single digits and now are guiding to low end of low double digits on this non-GAAP metric on opex. A couple of things going on.

One is we have taken foreign exchange-related losses on the remeasurement of our assets and liabilities during the first two quarters, order of magnitude about $70 million. And you'll see all of this in our reports, which we've kind of publicly put out there. So that's certainly impacting it. And then a couple of other things which, to me, are more critical, which is we continue to invest in the long-term growth of our business, that which includes investing in our people.

In a hot talent market, we want to make sure we've got the best people. We want to be there. In terms of having those best people help us execute on what we've laid out as our strategic priorities, which is what we're doing right here. We've always kind of followed the philosophy of let's keep an eye on the top line and then kind of also as to what we want to do from an expense and investment standpoint, and that's the philosophy we're following.

- CFO Sachin Mehra

My Take:

With Visa reporting another stellar quarter a few weeks before, the street and myself were expecting strong numbers from Mastercard which were delivered. What’s interesting is their increased strength in Europe, as they callout the region is incredibly diverse in situations and have strong growth drivers firmly in place.

I think we can all see it around us from co-workers, friends and family that people are still increasingly spending and especially going on those international trips they had planned over the last almost 3 years at this point. This quarter was firmly in the “rinse-and-repeat” category for me.

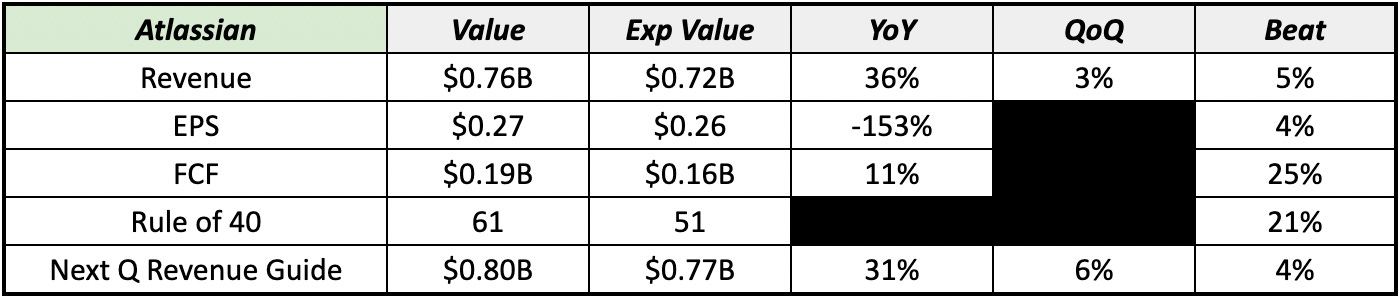

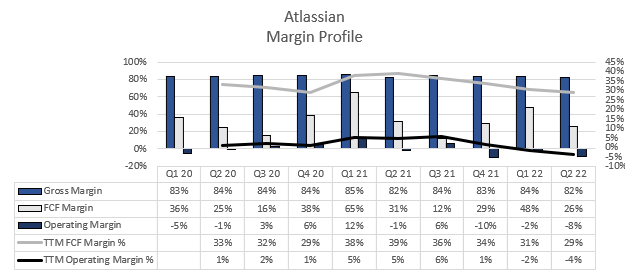

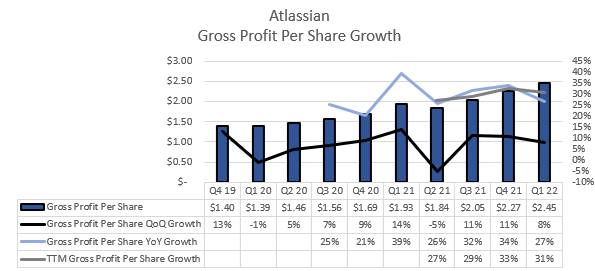

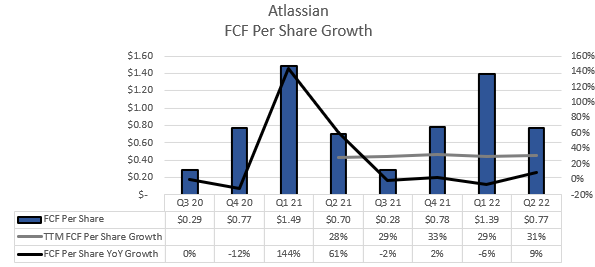

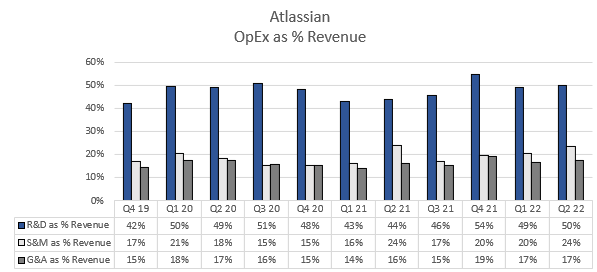

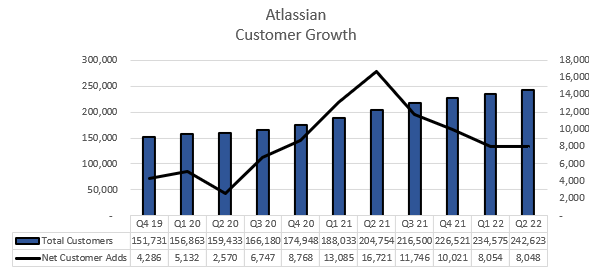

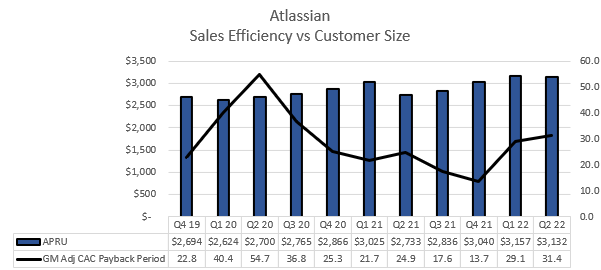

Atlassian TEAM 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On cloud revenue coming from license-migrations, and general outlook color:

As we mentioned previously in our Investor Day, a few months ago and reiterating now on this earnings call, we expect cloud growth to be approximately 50% year on year for FY 2023 and FY 2024 and so that remains the same. We've also said that there's high single-digit of that growth comes from migrations, in any given year. And so we expect again, that could continue.

We haven't looked in terms of the FY 2024 dynamic, of how that goes. What we do see though are migrating customers, expand at a similar rate to the customers we have in our existing instances. And we've also stated that previously, we have a net expansion rate of 130% in cloud, and 140% for our larger customers in cloud.

- Co-CEO Scott Farquhar

On EMEA region trends:

We have been keeping a very special eye in the EMEA region. The good news as of to date is we have yet to see any specific trend geographically or even in industry segments or in customer size that gives us pause or worry to date. So something we continue to watch like a hawk, but there's no new news to share today.

- CRO Cameron Deatsch

On opportunity to invest into the business, mostly into R&D:

But as a result of all these opportunities we made a decision to invest heavier behind these opportunities than we had before. And then we said in our Investor Day that we expect margins for FY 2023 to be in the mid-teens. And so those areas of investments are as you mentioned are largely in R&D. We are sort of really seeing huge investments there because of the features and getting our cloud to the stage where we can accommodate 100% of our customers require some more features.

You will also see some investments turn in other areas of the P&L, because for example they are some handholding to get our customers across that doesn't show in R&D, as well as it shows up in other areas in the P&L. So largely R&D but you may see some other areas of P&L impacted just to the way that we're helping our customers migrate..

- Co-CEO Scott Farquhar

On freemium upgrade trends they’re seeing:

We're about two years into this experience, but we continue to have many, many, many thousands of customers signing up in free plans and they either need to add an 11th user which then they had a pay to get the 11th user or simply they want more premium capabilities in our standard and premium additions.

Those are the reasons people enter their credit card. And the one thing that's worth calling out, that we've seen literally just in the last month is that the cohort of customers that came in the April, May and June timeframe are converting to those paid plans at a slightly slower rate than what we've seen in previous quarters. Now I'd love to say that's specific to a product, or a geography, or an industry. There's no specific customer segment there.

- CRO Cameron Deatsch

Further color on playing offensive with business:

Look we've been pretty clear right that we're playing offense. We continue to tell that quarter in quarter out. We're using this period of time to deepen our strategic position and increase the advantages we have over the competition, right? There's less -- they say that they would go as cash funding competition. And so we think we have a really good opportunity going forward.

We also have spent a lot of time retooling our hiring pipeline over the last two years and are really, really excited with where we stand at the moment. So we've had I believe our two biggest quarters of hiring in the last two quarters and we continue to do so. Obviously, we don't just look at the volume multipliers or that's sort of an absolute number marker. We continue to push quality of the talent that's available and we think that that will get easier in difficult circumstances.

And also obviously making sure that the cultural fit and other things that are in which is incredibly important and incredibly difficult and a huge challenge for us to do as we continue to scale. There's no doubt as Scott mentioned, the majority of that hiring is going to R&D to try to again deepen those strategic positions that we already have. The last thing I would say is just a reminder that we made the same or similar sort of play in the 2008, 2009 period. We paused for a little while then and then we realized that we were in a very strong position as a company relative to other companies out there.

- Co-CEO Mike Cannon-Brookes

On strength of Atlassian App Marketplace:

I can go on but one I want to touch on is also our third-party application marketplace. We have one of the best marketplaces in enterprise software and customers can easily adopt incremental functionality or whole new areas of functionality in our marketplace. And so we see expansion across all of those vectors in various ways. And there's not typically one specific part that we see our customers take, but we're very comfortable and feel very great about that going forward given how sticky our products are and how much additional functionality they can unlock across the organization once they start becoming a customer.

- Co-CEO Scott Farquhar

My Take:

This was quite the complicated quarter, where on one hand they are absolutely killing it on top-line and beating Billings estimates by 8% (a great sign for quarters to come), but they are sacrificing profitability at a stage in their life at 2.8B in TTM revenue and 60B in market cap at the timing of writing this. Is it unreasonable for me to question that haha?

This company has always been incredibly well run by their two founders and Co-CEOs, but at some point lets get some GAAP profitability eh? I don’t think this is a company where they can lean on the “growth” narrative indefinitely, although their cloud migration is one of the cleanest growth stories in software in my opinion. Still, this is something I’m watching.

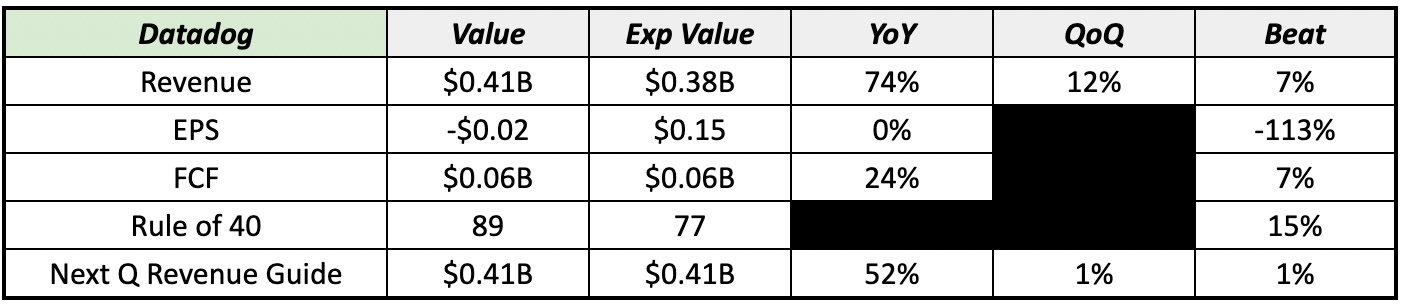

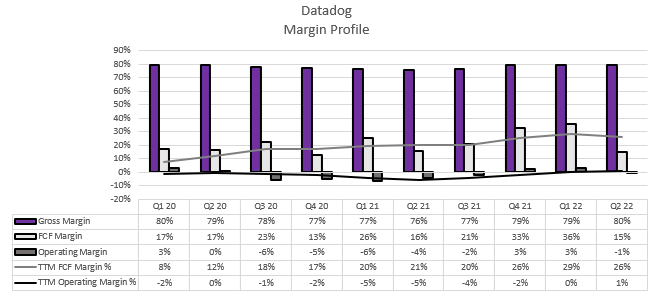

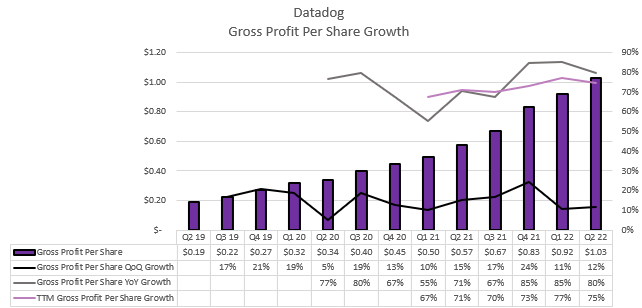

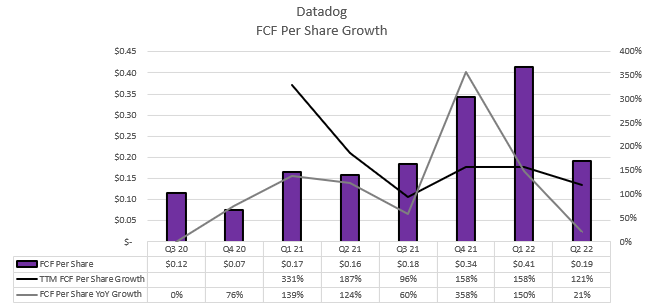

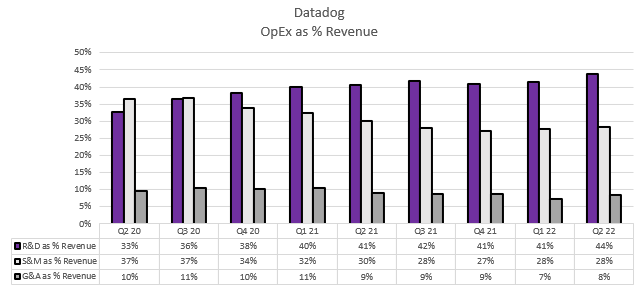

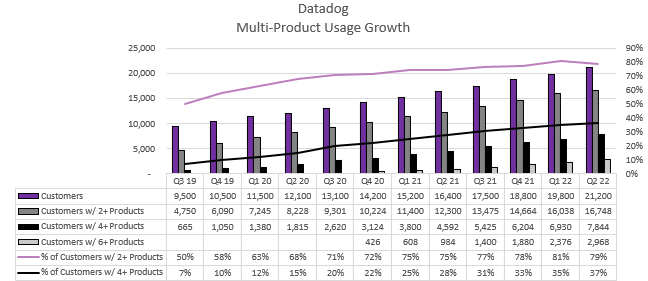

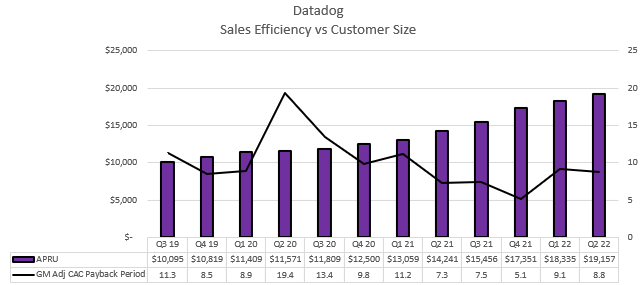

Datadog DDOG 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On baked-in assumptions in guidance:

In July, we did see an improvement in trends, but we still remain conservative in our outlook for the short term because of the noisiness of the data we're seeing there, it's -- there's a few more valuations, a bit more noise. And all of that is underpinned by some macro uncertainty. So we want to derisk that a little bit and give it more careful.

- CEO Olivier Pomel

Further color on guidance philosophy:

Yes. On guidance, as you know, we have always been conservative in our guidance by using lower organic growth and other metrics than seen historically and continue to maintain that philosophy. I would note that if you look at the raise here and the percentage of the beat that was passed through into the raise from Q2, it is lower, more conservative than we have done in previous quarters. And the reason for that is the macro uncertainty where we can't be as confident about what happens given the macro uncertainty.

So I would say there, if you want to take that, there were some incremental conservatism put into this. But I'd remind everybody that we've always been quite conservative in using assumptions that are lower than the past when we give guidance.

- CFO David Obstler

On how being land-and-expand focused can create variability in Billings and RPO:

I remind everybody that with our land and expand where we start getting used by clients, they scale up the growth and when they get to a certain point through, they go to an increased commit.

Because of that, there's variability in the billings and RPO that net-net, over time, on average, go toward the ARR growth. Again, remember, we mentioned that the ARR growth is the best metric. And the way to look at that is that you look at the revenues. You take -- you use the linearity, which is 34%, 35% of that and multiply that times 12, and that is pure because it doesn't get altered by when a bill goes out either in timing or whether the bill is a previous commitment plus an on-demand or a new commitment.

- CFO David Obstler

On looking at potentially larger sized M&A:

It's possible. Everything is open. We've looked at some of those in the past. We're raising the higher for larger businesses like that.

But we're really looking at valuations coming down and some more opportunities presenting themselves to us there. So everything is possible. But in general, we're very active on the M&A side. I think we'll only be more active as markets temper as they are right now.

- CEO Olivier Pomel

On Datadog’s aggressive but thoughtful approach to hiring and growth initiatives:

Right now, we're aggressively recruiting. We're building capacity. We're successful at it. And I really see it as a predictor of future success.

We're in an interesting situation because -- as a company, we are very efficient. We've been very disciplined from the funding of the company. For those of you who have followed us for a long time, we burned less than $30 million on our way to IPO, and we've generated a lot more cash than that since then. So no discipline be into the DNA of the company.

We also built the business around model that is frictionless and extremely efficient. And we've shown this efficiency, I would say, over the past two quarters by growing very fast while being fairly profitable. So we did no doubt in our minds about the long-term profitability profile of the company. So what this does is that it affords us opportunities to invest in times like this, that the rest of the market will not have.

Last year, everybody would invest everybody could spend money, it didn't matter. This year, I think it's a little bit different. So we really see that as an opportunity to break from the back even further and innovate, build self capacity and all those things.

Now obviously, as I said earlier, discipline is in the DNA of the company. So we're always looking at with our margins are or the macro environment is. And we have all the levers we need to adjust so we can maintain profitability in the future.

- CEO Olivier Pomel

My Take:

There’s a couple different ways to slice this quarter up. For all things considered for the stock, Q2 numbers didn’t really matter and all leads to 2H 22 where they, alongside Snowflake, have some of the toughest YoY comps to go up against.

Now with that said, you noticed that Datadog also was increasingly pessimistic with its guidance which can make investors quite nervous on the surface level (I think if you roll forward their guidance, they would exit Q4 with a ~32% YoY growth rate).

To me, this was just prudent caution by the Datadog team and I personally expect them to have a great second half to the year. I feel they really thread the needle of a core mid-market customer base with increasing penetration and a cost-savings pitch towards the enterprise level which has seen sales cycles lengthen. Their strong Q2 numbers and sales efficiency holding steady already in a challenging environment provide me with that confidence.

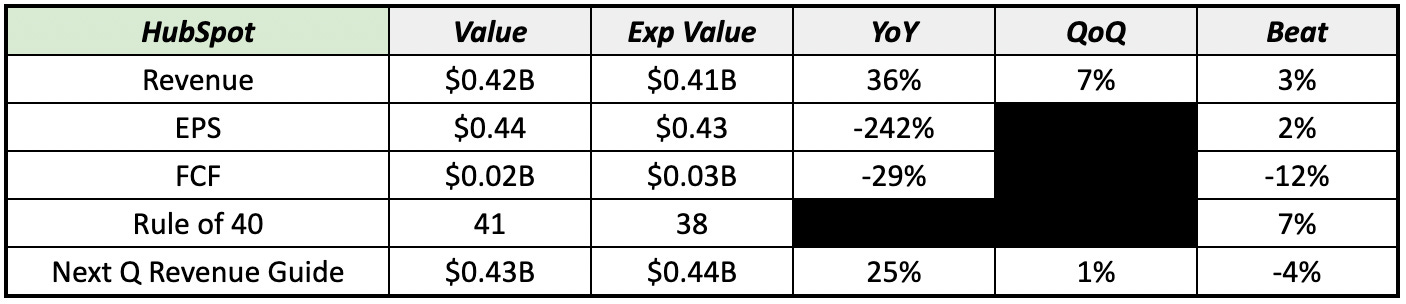

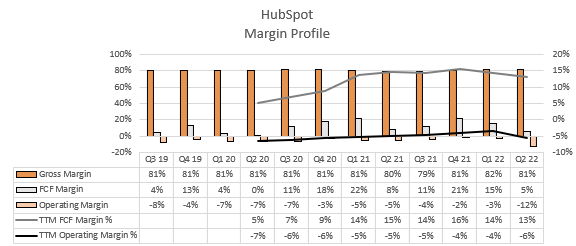

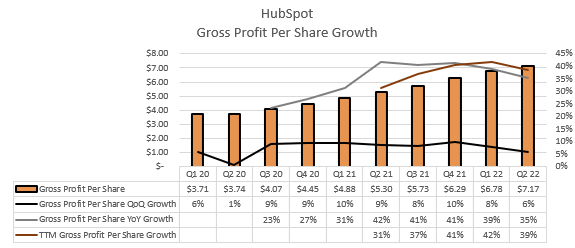

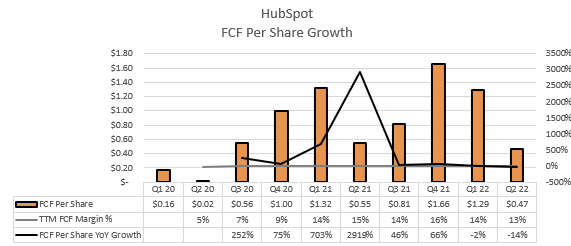

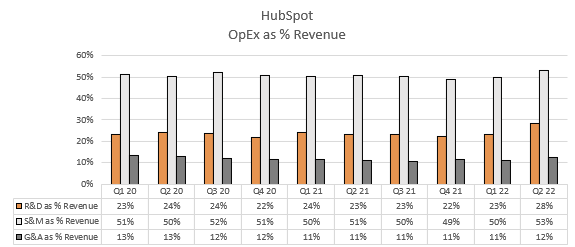

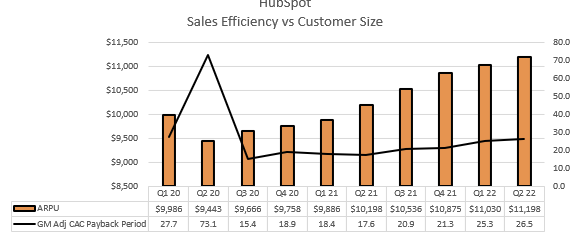

HubSpot HUBS 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On HubSpot’s deal environment:

We are seeing two trends. First off, deal cycles are lengthening and more decision-makers, specifically CFOs and CEOs are getting pulled into deals for approval.

Now, in early May, we were one of the first companies to transparently share that we saw deals taking longer in Europe. And in June, we saw these trends become more broad-based across our segments and the geos that we serve. Now, while these trends will have impact in the short term, and it is reflected within our guidance, we are confident in HubSpot's long-term growth opportunity for a couple of reasons. First off, while these deals are taking longer, they are coming down to platform and multi-hub decisions.

SMBs are figuring out how to spend effectively, and they're looking at HubSpot as the platform to run their front office. So we see deals close favorably but taking a little bit longer. And second, we're not a discretionary point solution. We're the backbone for small and medium businesses.

All these businesses still need to market, they need to sell, they need to service their customers. And HubSpot is a system of record and engagement for customer data. So we're mission-critical and we're sticky. So while we're seeing the demand trend soften a bit in the short term, we are very confident in our strategy and long-term growth.

- CEO Yamini Rangan

On retention outlook for the rest of the year:

Yeah. Sure thing. As you know, we think about retention in two ways. We have a gross retention.

That is the base of what we then ultimately have as net revenue retention, which happens after the net upsell. Net retention in our quarter was comfortably above that 110 target that we've been talking about despite really the more difficult environment that we saw toward the end of the quarter. I think the good news there is that underneath that the gross retention remained really solid in the high 80s, which is the range that we've been talking about for a year or two now. And then, on the net retention side, we had another quarter of really strong installed base selling, which in particular, edition upgrades and cross-sell really led the way for us here in Q2.

In the back half of the year, it's a good question. I would expect that net revenue retention will hang in there, I would call it, around 110 for Q3 and Q4.

- CFO Kathryn Bueker

On how HubSpot can differentiate itself in a higher scrutinized B2B buying environment:

So from our perspective, we are leading with a clear impact from having marketing, sales, service tie together. The other part that's changing is that customers want to be able to do more with less. That means they are OK giving up 1-point solutions, and they're looking for more platform-level solutions that are very cost effective. So we're leading with our CRM platform, as well as multi-hub value proposition to have very clear TCO-saving decisions for our customers.

[Different answer but similar topic]

And examples of that are sales and marketing that continues to help them grow. And so, I think it's really a question of where they are prioritizing. I think more broadly speaking, there is a look at how many point solutions do we have? Do we need all of these? And is there an opportunity to eliminate some of these point solutions and consolidate on a platform like HubSpot? And that's certainly a value proposition that we are leaning into for both multi-hub sales, as well as our entire suite sales.

- CEO Yamini Rangan

On guide outlook for 202:

Yeah. Maybe I'll dive in there. What we guided in May, Alex, the midpoint of our guide was 32.5% growth for full year revenue and on an as-reported basis. And our update is for 30% at the midpoint on an as-reported basis, which is a 2.5% slowdown.

one point of that is from FX, and then the other point and a half is associated with macro and business performance. I would like to remind you that our guidance includes six points of FX impact for the full year, up from five. So our constant currency revenue growth has moved from 37.5% to 36% growth for 2022. And then, in terms of payment terms, we really haven't seen anything of note.

- CFO Kathryn Bueker

On the strong KPI performance of the Q2 quarter:

And I think that the KPIs we saw in Q2 really demonstrated that balance pretty nicely. We added 7,000-plus new customers, and we were able to grow double digit both in constant currency and on an as-reported basis, our ASRPC.

That being said, I think as you look forward, and we've talked a lot about the moderating macro environment, we'll probably see a little bit of a moderation similar to what we're seeing in revenue across our KPIs. And so, we don't really give guidance there, but we do think we would anticipate kind of back half of the year, something that looks like 6,000 to 7,000 new customers added in Q3 and Q4 and ASRPC growth that looks closer to the 10% end of the double digit in constant currency.

- CFO Kathryn Bueker

On price increase philosophy and announced price increase for Marketing Hub enterprise edition:

We talk innovation and build powerful features within the enterprise tier, and over time, we will bring those high-end features down to professional, starter and premium editions. That's been our pricing and packaging philosophy for a while. When we have added tremendous value, then we look at pricing changes, and that's been very consistent. So what I mentioned in the prepared remarks today is that with marketing hub, we have innovated, we have added tons of incremental value over the last few years.

And the last time we increased price for marketing hub enterprise was INBOUND 2018. So that was like four years ago, and that certainly added a lot of value. So what we did in July is that we announced an upcoming modest increase in terms of pricing that will be effective one. For new customers, it's kind of in the 12% range.

And that announcement has gone out. We are tracking the feedback from customers, and it has been fine so far. So broadly, we'll continue to stay focused on driving a lot of value with our products. And when we deliver value to customers, we look at pricing and packaging decisions and changes.

- CEO Yamini Rangan

On the uptick in SBC for Q2:

Yeah. You're right. So Q2 stock comp expense every year is a high watermark for us as a percentage of revenue because we do a catch-up in expense for two quarters. And so, that 19% in Q2 will be the high watermark for 2022.

The increase is driven by a few things. One, there's an impact -- we had a bunch of notable executive hires over the last six months, and that is -- that impacts. And then, the other big change is that we made a shift in our RSU vesting from four years to three years for all of our employees. We think it was an important change for us to make it increase the attractiveness of the RSU and increase the retentive value of the RSU.

And so, those are really the two big drivers of the SBC increase. Even with those changes, we pay a lot of attention to stock comp as a percentage of revenue. We also pay a lot of attention to dilution. And we look at our management of those relative to our peer companies, and we still compare very well against the software companies in general.

- CFO Kathryn Bueker

On Service Hub reintroduction:

Brad, thanks a lot for both of those questions. I'll start with the Service Hub one. We're very happy with the traction that we're beginning to see following the relaunch. And just as a general reminder, we launched a number of features in both Q1, as well as Q2, including SLAs, mobile helpdesk, inbound calling, you name it, like there's a very long list of really needle-moving features.

And the focus for us with Service Hub has been providing a modern helpdesk that provides omnichannel support and great AI-powered automation. And the question that we asked after a major relaunch of a project -- product like that is, are more customers buying the product, are more customers using the product and are more customers happy with the product. And all three are trending positively and in the right direction. And in the past quarter, we've seen customer usage of features like ticket and inbox tools increase.

And so, overall, the feedback from Service Hub has been very positive. Our partners are beginning to see this as traction in terms of the conversations they're having and so is our direct sales team.

It certainly means more platform and multi-hub deals. And that's exactly what we're seeing in conversations. As you get a CEO or a CFO getting involved in the field, the question they're asking is what can be eliminated, what can be consolidated. And therefore, for us, it has been leaning into our platform message, as well as the value proposition, which is we deliver a very cohesive, connected, easy-to-use platform.

- CEO Yamini Rangan

On product innovation roadmap and customer feedback:

One quick thing to add on demand is we just had our product strategy meeting, which is -- we spent eight hours talking about what customers are asking for, what partners are asking for. And one continuing trend we've seen is that customers still have ideas. It's not like they've kind of crawled into holes like, OK, we're done here.

They're still asking for new features. They're asking for new developments. So there are years and years of innovation left across the front office. So this is not a static industry where everyone's kind of said, OK, well, we're done here.

We're seeing just as much kind of demand in terms of innovation from our customers and partners as we have in the past. So that has not slowed down. And the list of things that we want to do over the coming years is just as long as it's ever been.

- CTO Dharmesh Shah

My Take:

This was the first company to report where my thesis after ServiceNow reported on SaaS companies selling into the mid-market would be most successful in this macro environment with the lengthened sales cycle at the enterprise level and headwinds at SMB level, since these company’s salespeople are already talking to top decision makers and business owners to begin with:

HubSpot is probably my favorite story stock I own with just the culture of innovation and strong leadership. I was quite happy with this report as they called out being cautious with their guide, but they still beat their billings street estimates by a healthy 2% which shows that caution.

With the upside of Service Hub reintroduction, Operations Hub continuing traction, Payments being in very early stages still, and even their Sales Hub still at an early maturity point in terms of ARR opportunity (HubSpot last updated this hub was growing 70%+ in November 2021 at their investor day), and amazing culture of innovation, I feel pretty confident holding this name through SMB challenges that they might continue to face.

Also worth mentioning, in Q2 they purchased the domain name “connect.com”, where they are using it as an internal HubSpot based LinkedIn type community platform (2,206 users on the site as I type this for my own tracking haha). I had a couple tweets about the backstory from Dharmesh potentially owning that connect.com domain name personally, and he talks about his ambition for a LinkedIn challenger in this clip of a 2021 The Hustle podcast.

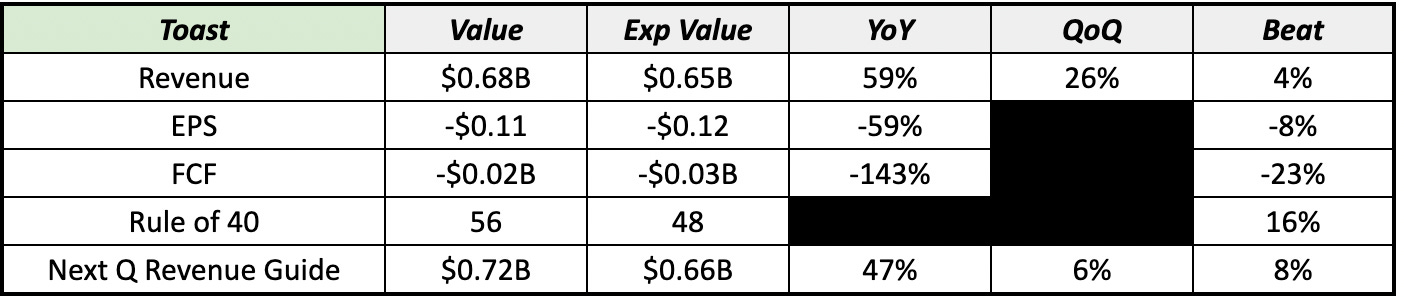

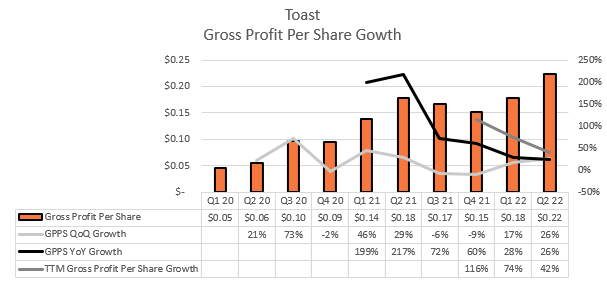

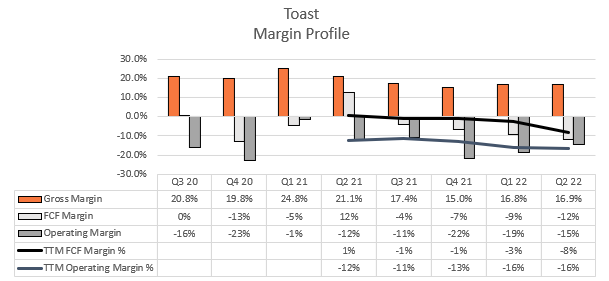

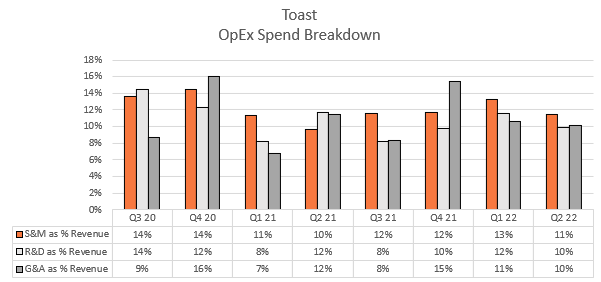

Toast TOST 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On priority around profitable growth:

Yes. Thanks for the question. So hopefully, you can tell that improving profitability is one of our biggest priorities. And we've made great progress in the first half of the year on EBITDA, and you can see that reflected in our guidance.

And we believe we'll exit this year in a position to balance the investments of growth and margin improvement. And I just want to be mindful of the macro. So I mentioned in my prepared remarks that our guidance reflected some of that, which is also part of the reason we didn't want to give guidance beyond 2022 because we want to be incredibly balanced in that. And we also, frankly, want to take advantage of this market opportunity that's presented to us.

We still believe and have a ton of conviction that there's a lot of growth to come, and we're in the early innings. So we're trying to balance that growth with also cost discipline, as you guys can see in our results.

- CFO Elena Gomez

On restaurant environment and consumer demand:

Sure. Thanks, Stephen. First, we're not seeing any signs of a drop in consumer demand or pull back in spending in our business. Restaurants are seeing healthy demand.

Consumers continue to spend on services like dining, and the GPV trends are strong. That said, we're pretty mindful of the mixed macroeconomic signals, and we're monitoring closely. We still have -- and even through July, we haven't seen any pullback on consumer demand. And while we're not immune, consumer spend at restaurants has held up relatively well during past recessions, and we've been looking at past recessions.

And we feel pretty confident in what consumers will spend within the restaurant market. And then the last point I'd make is for restaurants, our platform becomes even more valuable in a tough market. So if we did see signal, you could rest assured that we've got scenarios planned, and we feel like our platform is in a good spot to help restaurants adapt and navigate uncertainty. So we feel pretty good on that consumer dimension.

- CEO Chris Comparato

On prioritizing spend to high ROI areas in uncertain macro environment:

Yes. I mean I think the way to think about it is what you guys probably don't see is we're metering our hiring and really focusing on investments in high ROI areas. We're taking a deep inspection in areas that don't drive revenue today and being incredibly ruthless in our prioritization there. And so as we think about margins, you should see a steady improvement over time and a commitment from this management team to get to breakeven and profitability over the near term.

- CFO Elena Gomez

On how they split up R&D initiatives across different time horizons:

Yes, DJ. It's a good question. I'm not going to comment specifically on that opportunity. But as Elena had mentioned in her script, about 20% of our R&D investment goes toward medium- and longer-term growth initiatives.

This includes opportunities that sit within our existing product portfolios. For example, xtraCHEF and what we could be doing with xtraCHEF over the long term. You look at team management and what we could be doing with payroll, now with Sling and with Pay Card in the future. So each of our product lines of business within the platform have substantial innovation ahead of them.

And then on top of that, we continue to experiment and invest in new ventures. And these are things that I'm not going to talk about today, but we're planting the seeds for how restaurants will thrive in the future. And we're talking five to 10 years down the road, basically the next acts for how we think restaurants will operate. So this 20% of our R&D is super important because you'll continue to see us experiment, listen to our customers and then adapt to their needs.

- CEO Chris Comparato

On how they’ve been able to execute in uncertain environment with record net new location adds in Q2:

It's really a balanced growth across our bookings and our net adds. We certainly see restaurants that are already operating move to Toast, and they believe in a digital platform.

And these are existing restaurants that are hyper local go-to-market team, knows how to tap into, and we see those restaurants move to Toast. Secondly, we're seeing restaurants already on Toast expand, and those are net adds as well. So we're seeing quite a bit of expansion within our portfolio from existing customers. And then thirdly, we certainly see net new locations in the form of new constructions.

And it's always been a sort of a balanced attack across those three. I think as a reminder, I want to remind you that we're still [Inaudible] of the U.S. total addressable market. So our reps in these markets have a lot of surface area to go after, and we're in the early innings of them penetrating these markets to create, call it, flywheel market.

So it's a little bit of a balancing attack in these markets across those three dimensions. The other thing that I'll mention is beyond net adds -- just remember that net adds on locations is only one lever that we play with. The second lever is ARPU. So as we win a customer and build trust, we're growing more of the platform that the average restaurant is using.

And that's a really important lever for us because restaurants are adopting more and more of our modules. So it's a little bit of a balanced attack across those growth levers.

- CEO Chris Comparato

On continued sequential ARPU expansion:

Yes. No, I think it's a good call out. So as you can tell from our prepared remarks, increasing ARPU is such an important part of our growth strategy. And we continue to see the sales team execute.

We talked about Toast shop. We talked about our growth team and our sell team. And then really, our go-to-market team, our reps are very good at positioning the entirety of the platform. They've been trained to do that and to really position that upfront.

So all of that, combined with the innovation that you're seeing in team management and xtraCHEF, is really coming together to drive that outcome that you're seeing. So we feel confident that we'll continue to see progress on ARPU. I won't guide to it specifically, but you continue to see -- as we add new customers, our newer customers are actually having higher ARPU as well, which I mentioned in my prepared remarks. So really encouraging.

And if I look at what's really driving that, it's a combination of our core products -- our core commerce products, but also xtraCHEF and payroll, which are very early for us. So really encouraging to see that growth.

- CFO Elena Gomez

On International investment and opportunity:

Yes. No, we're still very committed to international. Our investment, as you guys know, wasn't a significant investment, but it's perceiving as planned. We have some early customers.

The feedback is really good with those initial customers. And just as I’ve mentioned, 2022 is really a year of building the foundation. So this is a multiyear journey for us. And like you said, very early innings, but we're encouraged by what we see with the initial customers we have.

On seasonality into 2H 2022:

Yes. I think the way to think about it is two things. One is both from a location standpoint, typically, Q2 is our highest -- or seasonally higher than Q3, and then it comes back in Q4. So that's the location side.

GPV per location also tends to be higher in the summer months. So just keep that in mind. So that's probably the two things I'd say about seasonality.

- CFO Elena Gomez

My Take:

Toast is another company that is just continuing to execute on their stated growth playbook. What I also love and something I noticed listening to the Q1 call before entering, is they make it a large focus that they care about profitability and driving operating leverage, all while they have blowout quarters in net location adds and ARR.

The tailwinds around the digitization of restaurants is quite strong, and although very competitive, Toast’s GTM strategy of basically giving away their hardware and software for free to drive GPV in payments is highly differentiated and hard for competitors to go up against even without factoring in Toast being a superior product, which shows up in their earnings reports.

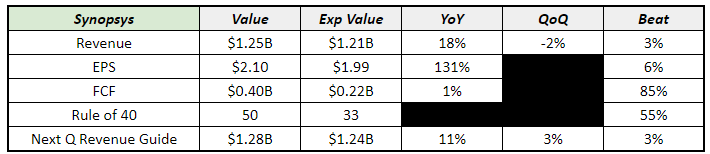

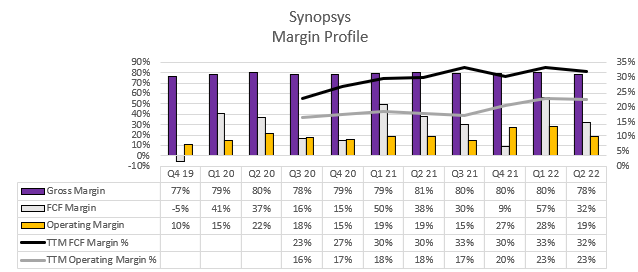

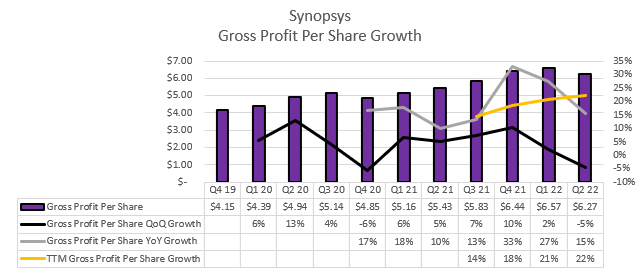

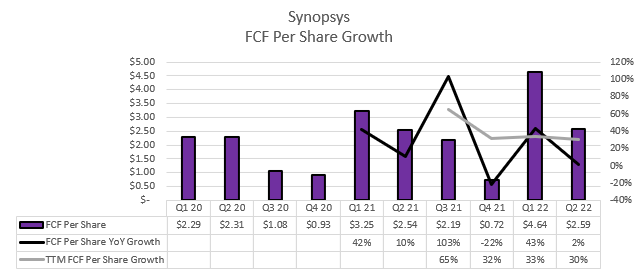

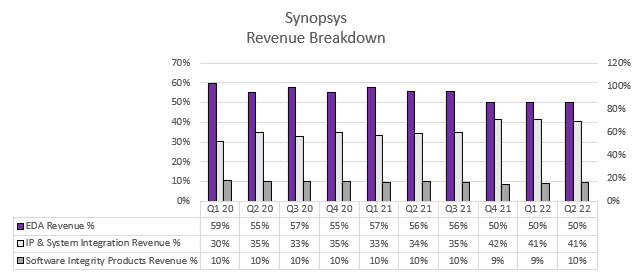

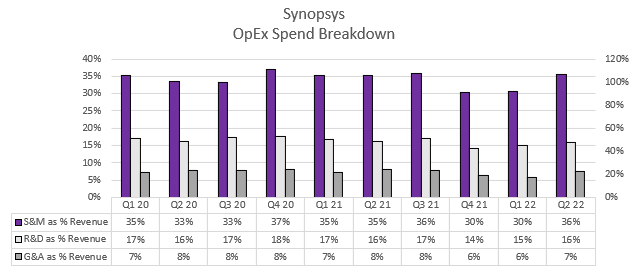

Synopsys SNPS 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On backlog:

Well, I'm glad you started with that question and added some caveats to it. So backlog for the quarter ended at $7.1 billion. And as you alluded to, it will fluctuate quarter-to-quarter, depending on the timing and recognition of revenue. The one thing I'll add to backlog, too, is that we duration target in the 2.5- to 3-year range. This quarter was on the lower end, running closer to 2.3 years. So it's slightly outside of our range.

- CFO Trac Pham

On the resilience of EDA and Synopsys being tied more to R&D spend than CapEx:

We are well aware of companies having reduced their hiring at least temporarily somewhat. I have not heard of any significant pullback or hesitation. The design activities typically don't mirror immediately what happens in the market because the market is really a function of the end sales, i.e., the quantity of chips being sold.

And so R&D is very stable against that. And more often than not, when there's a flat period of even -- or even a downturn, people invest in R&D to make sure that they have differentiation coming out of it. So as we, I think, said in the preamble, we feel that our business is actually very robust right now.

- CEO Aart de Geus

On how they’ve executed so well this year raising full year guidance again:

Yes. If you look at the guidance that we just gave for this first to the year and compare it to where we were back in December, at the midpoint, we're up north of $300 million in terms of the outlook for the year. And what we're seeing in terms of the better outlook is just really strength across all of the products.

We -- going into the year, we did expect it to be a strong year, but the traction that we've gotten on the new products, the continued strength on our IP business, and it's just the continued momentum on SIG that we saw with the last previous four quarters continued. So, we really saw strong growth across the customer base, across all geos, across all product lines. So business is doing really well.

- CFO Trac Pham

On competitive landscape:

I don't know actually that we see much of our competition, not to put them down or anything like that. I'm sure they're doing good stuff. But the advances that we've made in the last year, even in my own book, are quite remarkable and are broadening, by the way, to more and more capabilities going forward.

So I think we're into a whole next phase of what EDA will mean to our customers. And very often, advanced users try very quickly and then they're very careful. They tried very quickly, and they're absolutely adopting.

- CEO Aart de Geus

On how Synopsys’ AI portfolio differentiates themselves in the market:

Okay. Let me start with AI. The first thing to understand with AI is AI is a very advanced, different way of programming the solution to a variety of problems. And of course, we use the traditional approach, but we also use what's called pattern matching where you find situations -- where the recognition of the situation allows you to improve something for the better. Now that statement applies to the domain that you apply it to.

And so if we took our DSO.ai and say, "Hey, tomorrow morning, we're going to do, I don't know, blood diagnostics and learn something about patients," we would have initially 0 to offer because the AI needs to be matched in its intent to the area of the problem.

Secondly, AI for IP, of course, we use it ourselves. And a very simple reason would be one could consider Synopsys as one of the most advanced design companies in the world for what we do. And so, we don't use our designs to put chips on the markets. We don't design chips. We design IP blocks. But the concept is actually similar.

Third, you mentioned something interesting that I'm well familiar with, which is the need and the desire to sometimes take an existing design and migrate it to a different technology node. Sometimes it's called remastering. Sometimes it's called retargeting. That's the word you used, I think. And initially, we did some experiments already a year ago for knowing -- going from one node to another node that was pretty similar.

And we've got excellent results, and we've got them fast. And we could learn from the existing design and apply it to the new one. Meanwhile, we've vastly improved on that because we've been able to move many clicks forward in terms of nodal technology and still get much better results. And so I'm the first one to say we're at the beginning of a big journey. But so far, it's a pretty cool journey.

- CEO Aart de Geus

My Take:

Synopsys’ quarter was much to be expected after their EDA counterpart Cadence Design Systems also reported a strong quarter early in the reporting season. Their tailwinds being centered around R&D instead of CapEx (like ASML) shows how resilient of a semiconductor name this can be in all types of macro environments.

I found it funny how management got multiple earnest questions from analysts about how exactly we got to guiding so far above the original FY guide, for a more mature state company. Listening to how fired up a very seasoned Founder and CEO Aart de Geus still gets on these earnings calls about the future opportunity they have is always a joy.

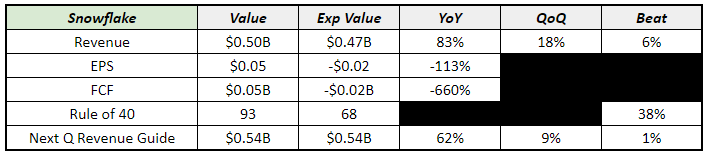

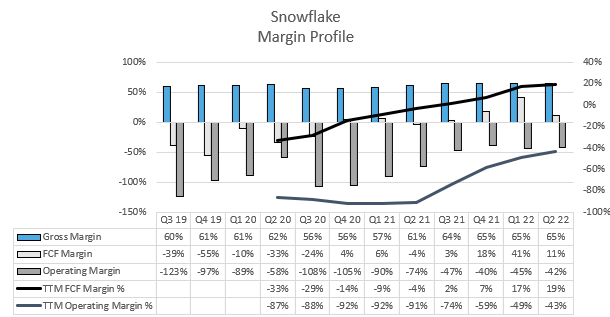

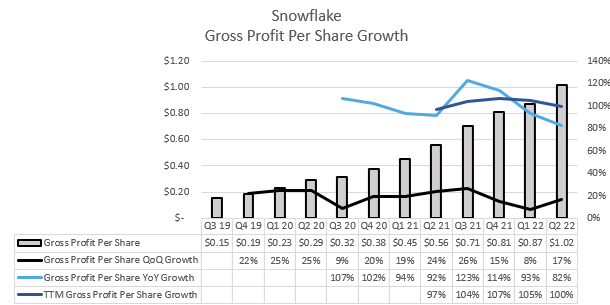

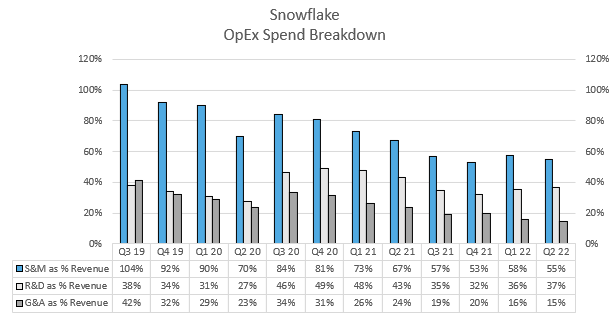

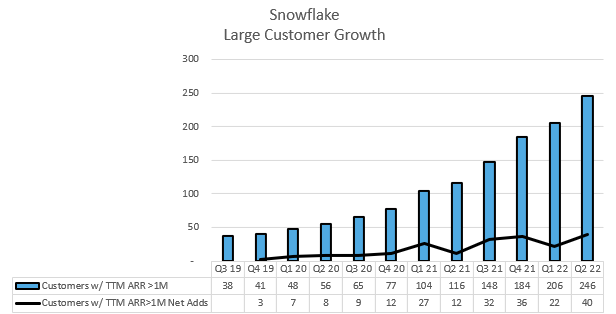

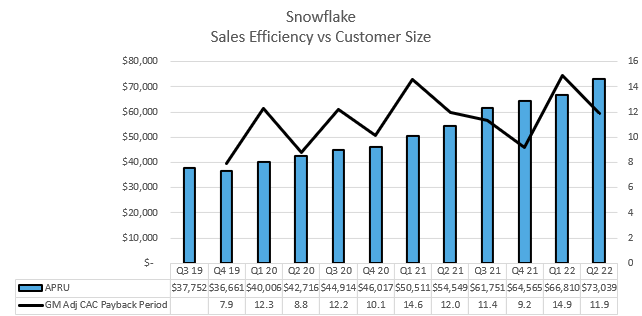

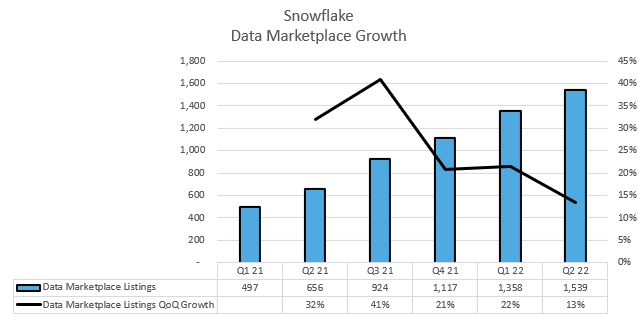

Snowflake SNOW 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On resilience of consumption numbers in Q2:

In general, I would say that Snowflake gets prioritized fairly high inside the enterprise. And the reason is we're sitting right on the intersection of cloud computing, artificial intelligence, machine learning, advanced analytics. Customers are -- they picked up the scent of the opportunity that is in front of them.

- CEO Frank Slootman

On being a consumption model vs traditional SaaS:

Yeah. I'll also add, Mark, just to remind, this is a consumption model, not a SaaS model. So even if we sign up a customer, it takes some months before they go into production.

As I mentioned, there was a Global 2000 technology company we signed in the last two years. It's now one of our top 10 customers. That customer didn't start really ramping until the end of last year, and they're going to continue to ramp. And there's many more that started ramping this quarter that we would have signed last quarter. So you can't just do a quarter over quarter.

And because it is a consumption model, we do see patterns. Some customers do go down consumption based upon specific projects. But by and large, most of our customers are still ramping, moving workloads to us. And we think that is going to continue on average with our customers.

- CFO Mike Scarpelli

Hyperscaler customer mix update:

With that said, the majority of our customers, 80-plus percent run in AWS, and about 18% is Azure and 2% is GCP.

- CFO Mike Scarpelli

On how Q4 is setting up to be a large renew quarter, and the unimportance of Billings for Snowflake internally given their business model:

With regards to the cRPO, that 57% of the total RPO, that is more of a function that we have a lot of our contracts that are starting to get burned down that were multiyear that we do expect in Q4 there will be a number of renewals of those contracts. So I do think the current cRPO as a percent of the total in Q4 will come down more in line with that into the low 50s where it historically has been. But that's really a function of -- think of our largest customer. They signed a three-year contract.

And I think it was September of 2020 that they're going to burn through that contract in advance, and there will be a big renewal with them. Whether they do it one year or multiyear, that's up to them. That will happen in our Q4. And then you'll see that as well.

We have a number of customers like that. One of the things that we're seeing more and more is customers because they're consuming faster than their annual amount in their actual contract term, they're doing what we're calling co-term or they're bridging to their annual renewal. And a lot of those annual renewals are really moving toward Q4 for us.

Well, I have to tell you, I don't even look at billings because it's a meaningless thing for our business because we're not a SaaS company. We're really focused more on cash flow and revenue consumption by our customers.

- CFO Mike Scarpelli

On how consumption models give customers for flexibility in times of uncertainty to throttle spend up and down:

I mean we sort of invert that whole way of thinking because it's actually quite attractive for customers to have a consumption model because they can sign a contract with us but then they can throttle up and down how much they want to use. You can't do that in a SaaS model. You're going to pay no matter what, whether you're using it or not.

So this gives customers actually more confidence to contract with us knowing that they can throttle up and down. So we actually think it's an advantage in the type of times that we're living in as opposed to a negative, which is what has been portrayed on the sell side and in the media.

- CEO Frank Slootman

On customer journey to Snowflake:

Yeah. I'll add to that, too, Raimo. As a reminder, new customers when we land them, they generally start very small, and it takes some nine months to really start to consume. So it's very low risk to come on.

And once we have an existing customer that is looking to buy more, they already have a path for what they want to do workloads, and they want to do that on Snowflake because we will save them money from what they're doing. And the other thing I want to remind you, too, is we have many different models. You can sign a one-year commitment. You can sign a three-year commitment.

Or you can go on to on-demand as a customer if you're not comfortable making a big commitment upfront. And we do see customers -- I think last quarter, about $7.2 million of our revenue was actually on-demand. These are new customers that are just trying us out before they sign a capacity deal.

- CFO Mike Scarpelli

On cloud transition still being in full effect with more old-guard dominoes falling:

I mean I will tell you that just in the last week, I've heard some -- two very, very iconic names in two different industries that were staunch on-premise people who would never ever go cloud and that are now going. So I just feel that the resistance is completely breaking and people are going cloud. I'm sure they have their own reasons.

But a lot of this is what you said as well, is that they are -- they're going to get left behind. You can't take advantage of innovations that are only available on the cloud. So, if anything, I tend to agree with you that we're going to see acceleration out of this as opposed to people holding back.

- CEO Frank Slootman

On Global 2000 customer average revenue and trends:

And what I will add, too, is we have 510 Global 2000 customers. The average revenue from them today is $1.2 million. That's up from $1.05 million last quarter, and that will continue to grow.

- CFO Mike Scarpelli

On hiring outlook and growth plans:

And with regards to investing in the business, we are continuing to invest in the business. You can see the headcount we're adding. Principally, headcount is the main investment we're doing in the business because that's what drives R&D.

That's what drives sales. But we're very thoughtful about where we invest those dollars and how quickly we do. And we think we're investing at the adequate pace, and we will continue with that.

And nothing has changed in our philosophy, we will continue to show leverage year after year.

- CFO Mike Scarpelli

On how Snowflake is becoming a de facto cloud application development and run-time platform:

Snowflake has become de facto a cloud application development and run time platform. People are building and deploying applications on Snowflake.

I mean we have customers like Western Union who were starting whole businesses on top of Snowflake. Those are the conversations that we are having with customers. Workload modernization, we'll be doing that until the end of time, but that's no longer the reality that dominates our daily existence

- CFO Mike Scarpelli

My Take:

I think this quarter can best be summed up with their record net adds of 1M ARR customers in a challenging software environment just shows investors how critical and value driven Snowflake’s platform is.

As management mentioned multiple times throughout the call, these outperformance quarters are years in the making given the nine months it takes customers to fully ramp into normalized consumption. So just remember back to all those insane quarters that Snowflake had over the last two years with Global 2000 customer adds and remember that those are now just starting to show up in the PnL.

Having two seasoned operators at the wheel who are insistent on driving operating leverage in their margins every year, and still doing so this quarter while having their huge Summit conference event, was really nice to see and I’m overall quite happy with this quarter.

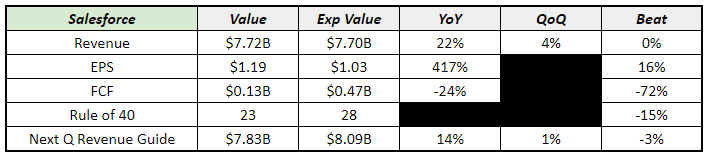

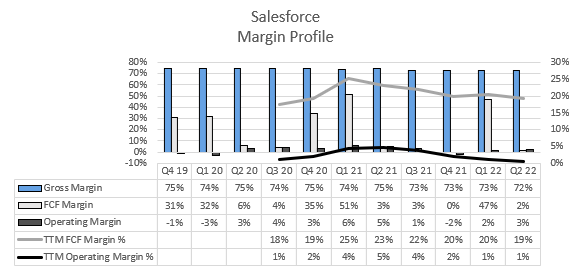

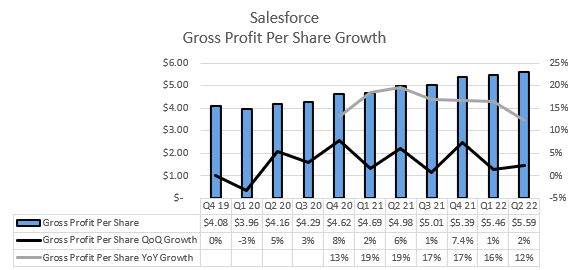

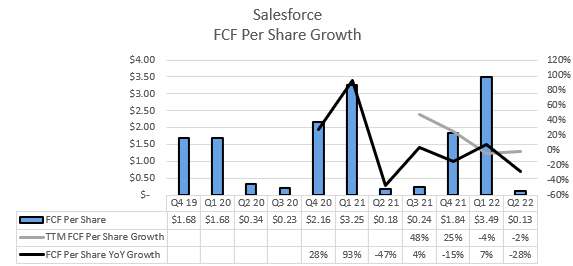

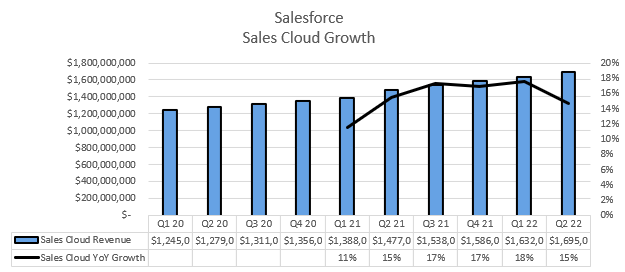

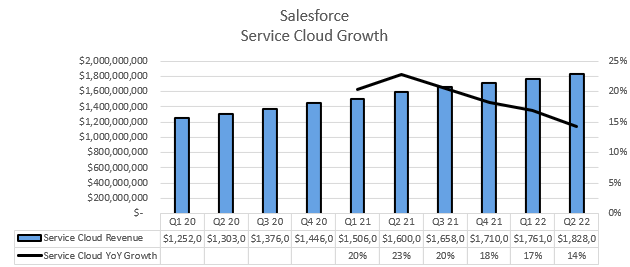

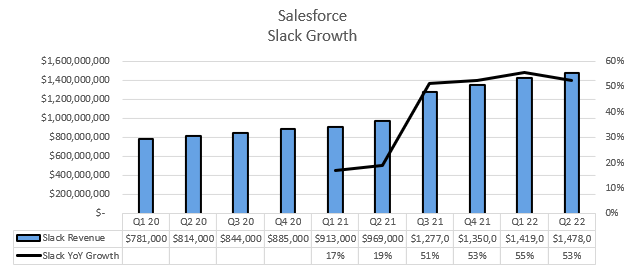

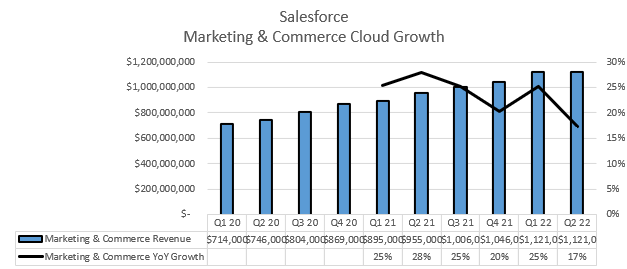

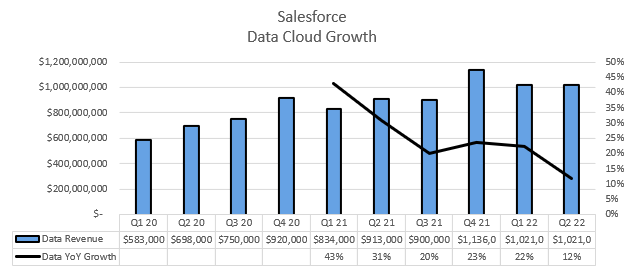

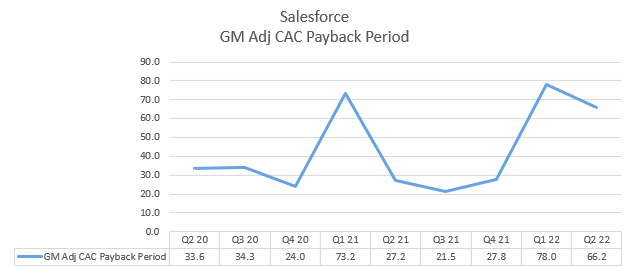

Salesforce CRM 0.00%↑

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On first announced share repurchase in prepared remarks:

We always get questions about our M&A strategy and what company we're going to acquire next and what we're going to do next from an acquisition cycle. I think we get this question every single earnings call that we do like this. And it's always one of my favorite parts of the call. And I'm excited to tell you we have found a great cloud company, growing revenue for 73 consecutive quarters through every economic cycle.

It's got great cash flow, No. 1 market share, an incredible brand, one of the most admired companies in the world, great values, fantastic community of 17 million Trailblazers, fantastic commitment to its community, runs across 90 countries. And that company is Salesforce. We're thrilled that our Board of Directors has authorized up to $10 billion in our first-ever share repurchase.

- Co-CEO Marc Benioff

On thinking into full year guide down:

When we look at the guide, I believe the guide is appropriate under the circumstances we're seeing right now. And as you know that there's two key drivers.

The first part is FX, the key currencies, the euro, the pound, the yen, they've all weakened to near historic levels, and we're seeing that impact on our top line as we look forward to the rest of the year. For the remaining part, as we called out, there was a distinct shift in customer buying behavior that we saw near the end of the quarter. And for purposes of the guide, we're assuming that those conditions endured through about the half of the year. Now, turning to your second part of your question, which I think was on op margin.

As you know, I was very happy that we are committed to 20.4% and holding that despite bringing down the top line. This is largely coming from a more disciplined approach. It is not a result of one single change. We are continuing to unlock incremental efficiencies across the business.

We're asking each leader to step up and look at their businesses and prioritize. I do believe that we are continuing to invest into growth, which still remains our No. 1 priority. In terms of the specific drivers, definitely continuing to take a measured approach and a very deliberate approach on hiring.

T&E, we are prioritizing for customer-facing travel. And again, we are continuing to benefit from some of the decisions we've made over the last few years on real estate.

- CFO Amy Weaver

On buying environment and customer priorities:

Yeah. Thanks for the question. First, I'll tell you, I think that trend continues. Digital transformation remains our customers' top priority, and digital transformation starts and ends with the customer.

And fundamentally, all of our customers are really investing into the secular trend of the digitization of their customer experience, their employee experience and with our portfolio, we're at the top of that list. I think what you're seeing is an increased focus on, I say, three things. One is time to value. The other is ensuring that these projects drive cost savings in addition to customer satisfaction and top line growth.

And then, the third is reducing complexity and vendor consolidation. Some of the stories I mentioned like Uber Eats, I think, are great examples because it's really about how do you put up things like digital service technology, whether it's chatbots or self-service, to really take out cost and make these projects pay for themselves as opposed to having protracted multiyear implementations. I think vendor consolidation is also a trend that we're seeing.

And if you look at some of the innovation we're bringing out like our Sales Cloud Unlimited edition, or Salesforce Easy, which I mentioned earlier in my script, they are really efforts to enable our customers to do more with less, to enable them to use Salesforce as their sole vendor, take out some point solutions that perhaps aren't getting the return on investments our customers are looking for, and sort of taking advantage of this opportunity to be the most strategic vendor for our customers right now as they look to really hold their technology to high standards, which is to drive top line and bottom line performance.

- Co-CEO Bret Taylor

On challenges Data Cloud business has seen, and opportunity to re-accelerate in 2H:

On the data business, it's a unique business for us because some of it is license based. And you can tend to see some of the headwinds we saw in July show up more immediately there. We feel very good about where both those businesses are right now, particularly in MuleSoft that as you heard Bret say is on a great trajectory and will be a tailwind to our revenue growth in the second half of this year.

We feel great about that. Tab is a critical component of our digital transformation with every customer wanting to leverage data to have better insights to the way they operate their business. So clearly, a lot of focus on these businesses because it is such a critical component of every digital transformation. We feel great about that, both those integration and analytics as a category for accelerated growth in the second half.

- COO Brian Millham

On thinking behind announced share repurchase:

And one of the things, we have such massive cash flow that I think it's completely appropriate for us to look at how we're handling our dilution, for example. I think that's been on the table for a while, and a lot of my conversations with investors they bring it up. We've waited for that moment.

I think now is the right moment where we can say we're going to directly address this with our kind of first-ever share repurchase, $10 billion. I'm very excited about it. At the same time, I don't think that that takes M&A off the table. I think that we continue to look for opportunities.

We want to be able to use our cash constructively. This is important for us. It doesn't mean that we're not going to have different kind of guardrails for M&A

- Co-CEO Marc Benioff

My Take:

The moment we have all been waiting for is finally here with Salesforce’s announced $10B share repurchase program. The bad news is their actual quarter was pretty unimpressive, with a big cut to FY guidance due to FX and lengthening sales cycles. It’s pretty puzzling to see the continued underperformance of Tableau and Mulsoft, whereas very mature products like Sales and Service cloud are still growing at pretty impressive clips at their large run-rates.

The silver lining has to be the continued outperformance of Slack and their platform cloud, and I’m pretty excited to see what they have to show in their Investor Event at the end of September.