Q1 2023: Portfolio Earnings Review

The Jiggy Capital Newsletter #19

In this newsletter, I will be highlighting the earnings reports of companies I own in my portfolio. My hope is you’ll get an idea of how the company performed against expectations, the trends behind their numbers, and some quotes from their earnings call.

This newsletter edition is mostly about the raw numbers and performance, and I walk through my portfolio decision-making and thought process in my quarter-end Portfolio Reviews.

If I had to segment the quality of reports between the nine companies highlighted, it would go as follows:

Great: ServiceNow, HubSpot, Procore

Average: PayPal, Chipotle, MasterCard

Not So Great: Amazon, Datadog, Texas Roadhouse

Companies I own that are not included in this newsletter due to being more recent additions are Adyen, Aritzia, Nintendo, CD Projekt Red, and Robinhood. I’m also going to edit Lululemon into this post when they report near end of the quarter.

The newsletter is in order of their reporting date, so feel free to skip around to the ones that interest you most. I also include my overall take at the bottom as well. Now let’s get into individual reports!

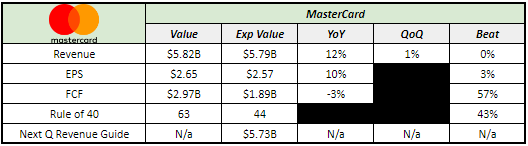

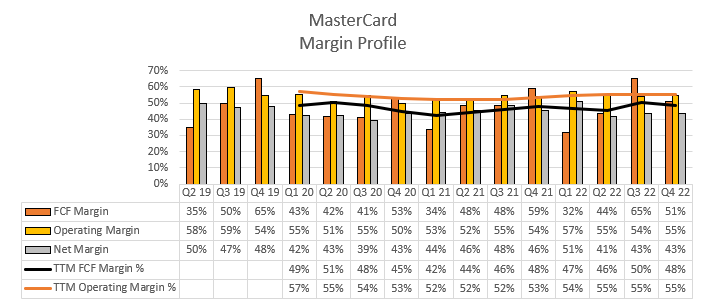

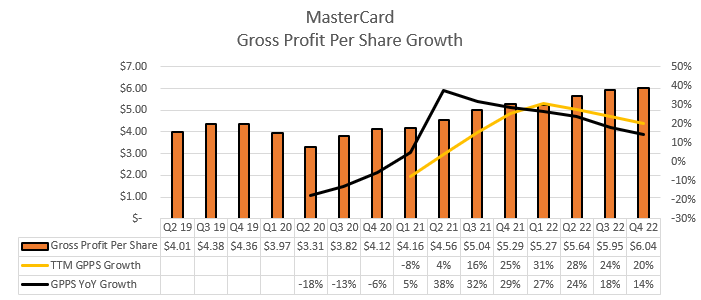

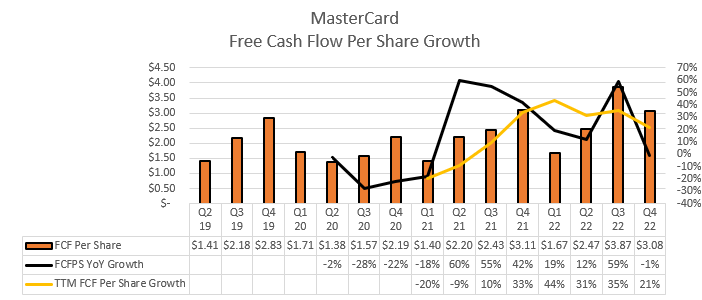

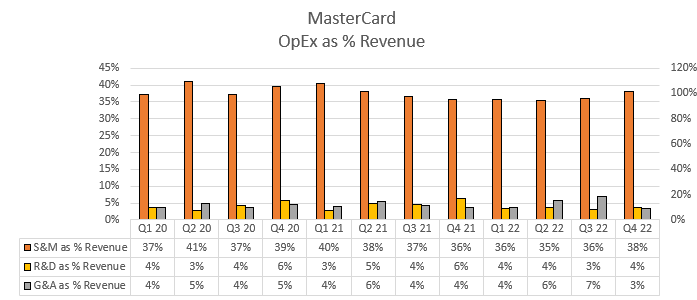

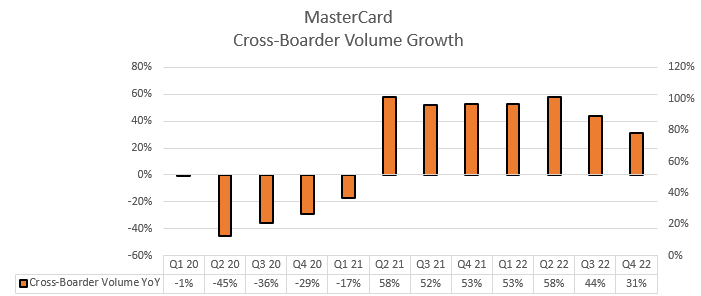

MasterCard MA 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Michael Miebach on Virtual Card opportunity for B2B space

So, the opportunity here lies really in taking our existing set of tools, namely from the card ecosystem, very specifically the virtual card capability, which came through an acquisition many, many years ago that we've now built out ourselves into the leader here. So this existing set of tools and a huge opportunity in terms of flows to be addressed and make them more efficient, we're looking at $14 trillion from an opportunity perspective…Cash and checks dominated existing tools, existing partners. This is right for us to go after it, and we're leaning in.

CFO Sachin Mehra on what China opening up means for Mastercard:

But suffice it to say that the opportunity is pretty sizable. The fact that we were in Q4 at 20% of 2019 levels from an inbound travel standpoint -- cross-border travel standpoint is just suggestive of the fact that if you just think about what's going on in the regions and how they've recovered and bounced right back and gone well above 2019 levels, there's a significant opportunity both on inbound and outbound as it relates to China.

CFO Mehra on the general state of cross-border travel heading into 2023:

Look, I mean, our cross-border proposition sound -- is very sound and stable. And I think at the end of the day, like I said, most of the regions are now back to what I would call the stable growth rates that we would normally have seen in the pre-pandemic phase. The one exception is Asia, and there's a little bit of opportunity which we have in Asia, which we've contemplated in our thoughts for 2023.

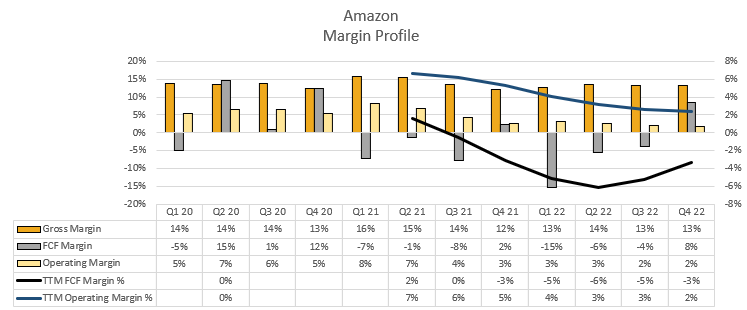

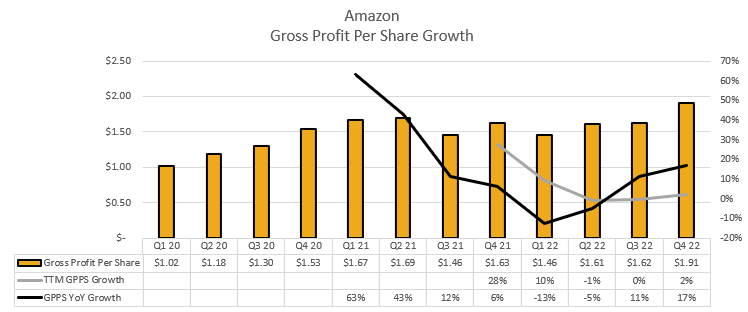

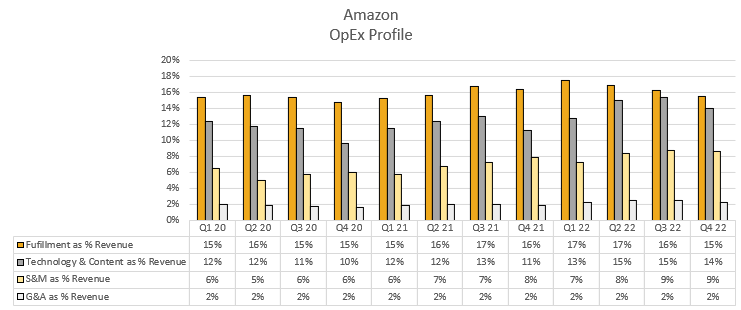

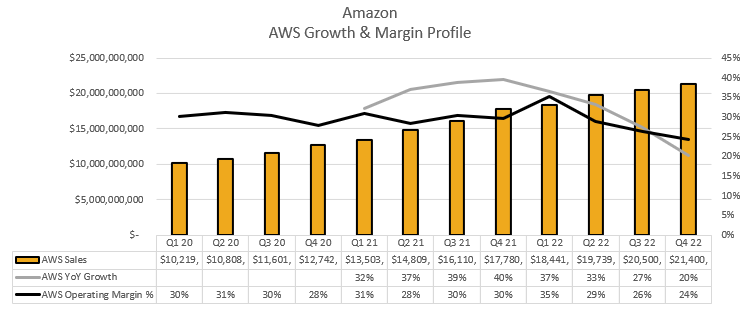

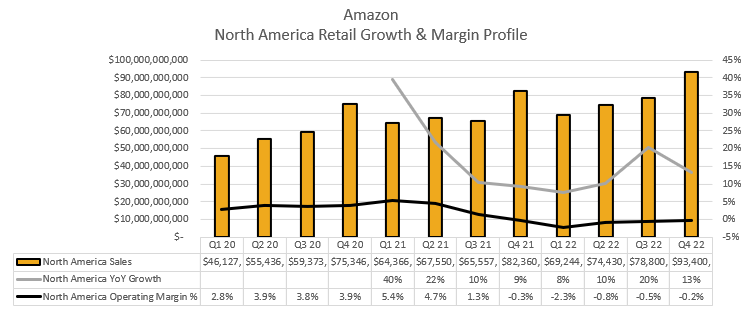

Amazon AMZN 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Andy Jassey on North America logistics business priorities:

As I addressed directly the North American stores questions, I think our -- probably the No. 1 priority that I spent time with the team on is reducing our cost to serve in our operations network. And as Brian touched on, it's important to remember that over the last few years, we've -- we took a fulfillment center footprint that we've built over 25 years and doubled it in just a couple of years.

And then we, at the same time, built out a transportation network for last mile roughly the size of UPS in a couple of years. And so when you do both of those things to meet the huge surge in demand, you're going to -- just to get those functional, it took everything we had. And so there's a lot to figure out how to optimize and how to make more efficient and more productive. And then I think at the same time, if you think about doubling the number of fulfillment centers you have and then adding a very large transportation network and you realize that all of those facilities have to link together to get products to customers, that's a pretty big expansion in the number of nodes in the network.

It becomes a little bit different network. And so to figure out how to be really efficient across all those links and have them be highly utilized and to get the flows in those facilities working the right way, it takes time. So we're working very hard on it. I'm pleased with the progress we made in Q4, and you can see that in some of the results.

CEO Jassey on AWS optimization trends they’re seeing from clients:

I think most enterprises right now are acting cautiously. You see it with virtually every enterprise, and we're being very thoughtful about streamlining our costs as well. And when you are being cautious, you look for ways that you can find -- you can spend less money.

And where companies can cost optimize or, in some cases, they may be used to doing analysis over 90 days of information and they say, "Well, can I get away with it for two weeks, doing two weeks' worth," it's not necessarily the best thing long term. But a lot of companies will do that when they're in uncertain economic situation. And the reality is that the way that we've built all our businesses, but AWS in this particular instance, is that we're going to help our customers find a way to spend less money. We are not focused on trying to optimize in any one quarter or any one year, we're trying to build a set of relationships in business that outlast all of us.

We have a very robust, healthy customer pipeline, new customers, migrations that are set to happen. A lot of companies during times of discontinuity like this will step back and think about what they want to change strategically to be in a position to reinvent their businesses and change their customer experiences more quickly as uncertain economies emerge, and that often means moving to the cloud.

We see a number of those pieces as well. And we're the only ones that really break out our cloud numbers in a more specific way. So it's always a little bit hard to answer your question about what we see. But we, to our best estimations, when we look at the absolute dollar growth year over year, we still have significantly more absolute dollar growth than anybody else we see in this space.

CEO Jassey on Prime buildout over 2022 and value that provides compared to other subscription services:

Just to add really one piece here, which is just, if you step back and think about a lot of subscription programs, there are a number of them that are $14, $15 a month really for entertainment content, which is more than what Prime is today. If you think about the value of Prime, which is less than what I just mentioned, where you get the entertainment content on the Prime Video side and you get the shipping benefit, the fast shipping benefit you can't find elsewhere and you get the music benefit, you get the Prime Gaming benefit and you get the photos benefit and you get the Buy with Prime capability, use your Prime subscription on websites beyond just Amazon and some of the grocery benefits that we provide, and RxPass like we just launched to get a number of medications people take regularly for $5 a month unlimited, that is remarkable value that you just don't find elsewhere. And we will continue to add things to Prime and continue to experiment with lots of different features and benefits. But it's still early days.

CEO Jassey on company optimization trends on further color on RIF announced:

We want to actually do a pretty good, thorough look about what we're investing and how much we think we need to, but doing so without having to give up our ability to invest in the key long-term strategic investments that we think could change broad customer experiences and change Amazon over time. And you saw that process led to us choosing to pause on incremental headcount as we tried to assess what was happening in the economy, and we eliminated some programs in fabric.com and Amazon Care and Amazon Glo, and Amazon Explore.

We decided to go slower on some -- on the physical store expansion in the grocery space until we had a format that we really believed in rolling out and we went a little bit slower on some devices, and until we made the very hard decision that Brian talked about earlier, which was the hardest decision I think we've all been a part of, which was to reduce or eliminate 18,000 roles. And so those were all done with an eye toward trying to streamline our cost but still be able to invest in the things that we think really matter over the long term.

Now we have a way of looking at investments that is different maybe from some other companies. I'm not saying it's right or wrong. It's just the way we look at it, which is when we think about big areas to invest in, we ask ourselves a few questions. We ask, if we were successful, could it really be big and move the needle at Amazon, which is a high bar at a place like Amazon? Do we think it's being well served today? Do we have a differentiated approach? And do we have some competence in those areas? And if we don't, can we acquire them quickly? And if we like the answers to those questions, we will invest.

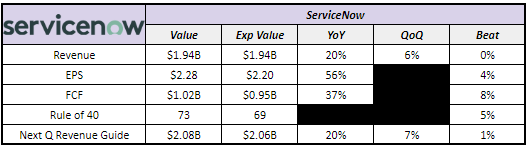

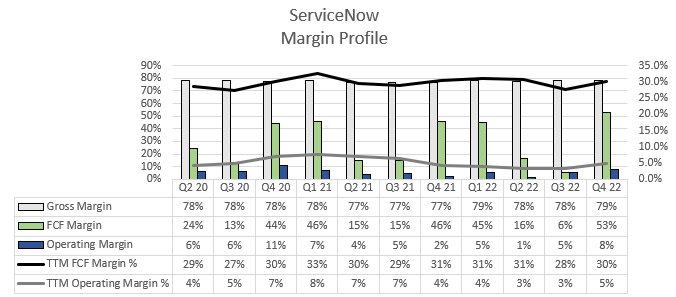

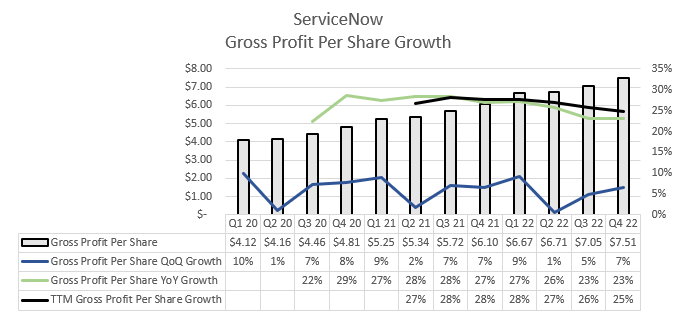

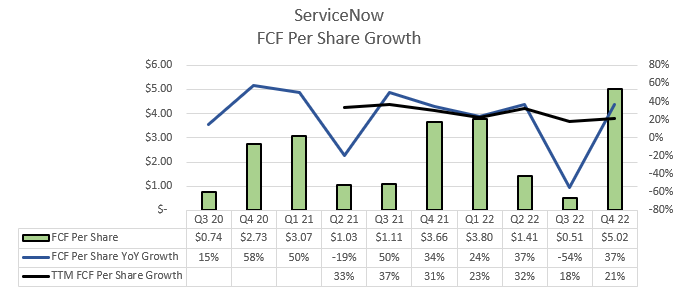

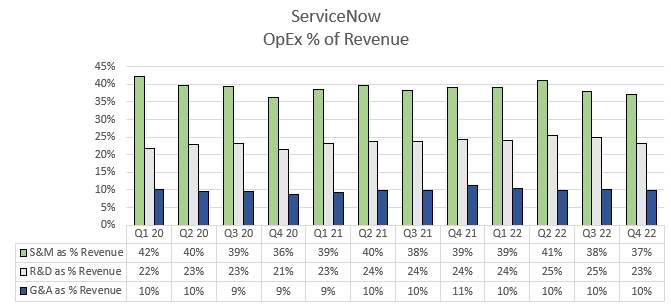

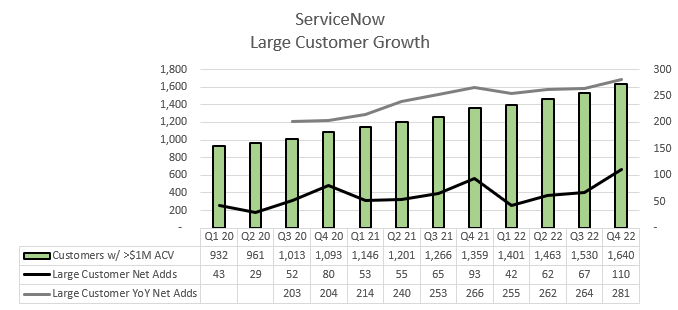

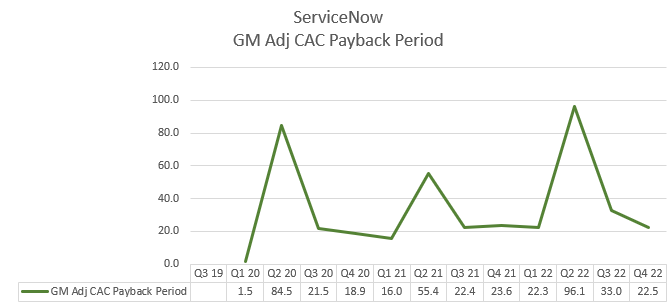

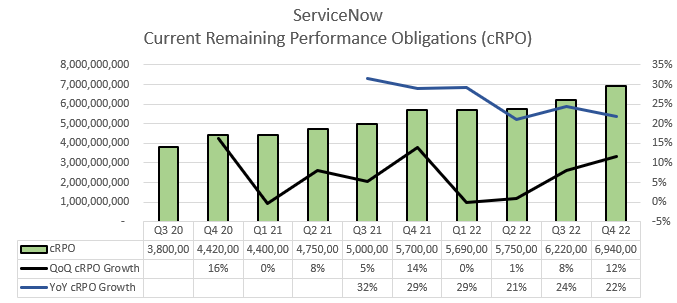

ServiceNow NOW 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CFO Gina Mastantuono on expansion vs renewal trends:

With respect to the early renewals, what I would point to is the strong net new ACV growth in Q4 tells you. And by the way, very strong expansion rate in Q4 tells you that customers are not changing their behaviors with respect to renewals, on-time renewals or with net new expansion. What you're just seeing is a little bit of the lack of meeting to do co-terms and bring things forward in the current macro. Again, with 98% renewal rates across the board, we remain as positive as ever that not only will we continue to expand in '23, as you've seen us do in '22, but also continue to renew those best-in-class renewal rates.

and later again:

And what I keep telling folks is the fact that we are not having to rely on early renewals as much as we've done in the past, shows the resilience and the strength and the power of the Now Platform. But yes, I also think that in this market, people are holding on to cash a little bit longer.

CFO Mastantuono on LT guidance dynamics given macro headwinds:

What I would say is, overall, the underlying growth that we're seeing remains healthy. FX headwinds have eased slightly, but certainly are still material. And with the uncertain macro backdrop, we're going to continue to monitor the market and provide an update on our long-term targets at our analyst day in May. So I'd say, again, underlying demand, really strong; operating margin, well on the trajectory to hit 27%; with respect to top line and free cash flow, with the impact of FX, and that keeps moving along, we'll update those targets for you in May.

CEO Bill McDermott on progression of macro trends he is seeing (long quote but thought this was best answer on call):

I think maybe we were the first ones to call it out that there were some clouds on the horizon back then with the macro, and we all know the forces that were blowing between Ukraine, inflation, tightening monetary policies and supply chain dislocation, and everyone sees that to a pulp so we don't need to go there. I think what happened back then is most businesses were not ready for that market.

And we immediately revamped our go-to-market in the way we approached the customer because we knew the customer would have to do more with less, automate their business, take cost out and improve productivity per person. And the work wasn't going to go away. It still had to be done, and step ServiceNow's platform. And then, we also knew at the same time that CEOs, 98% of them, this is a fact have a digital-first strategy…. Worried about the other 2%, but I'm good with the 98% because that makes a lot of sense. It's just a question of what equilibrium between growth and cost takeout would be necessary for them to achieve their goals. The good thing is, with ServiceNow's platform, you could say yes to both.

So what I see in the market, I see commodity tech that was at the peak of the hype cycle during the pandemic being dialed down or eliminated. And I see that investment freeing up to platforms that actually matter. So I do think our circumstances are actually improving because of this particular macro, because it's well known now that ServiceNow can take the cost down, if that's what you need immediately.

And given the layoffs that we're seeing and the stories that we're reading, I clearly see that our company is rising accordingly. And I see that in the pipeline. I see that in the maturity of the pipeline which is a really important fact. And this year, we came in with sales productivity at least 20% better than I had at the start of last year based on the feet on the street and the readiness of those feets because they've been well trained and certified to do their job.

All these forces are coming together in a way that gives me a feeling the market will be on our side, but our executional excellence will never have to rely on the weather conditions. We're ready.

CEO McDermott on hiring trends at company:

As Gina said, we're going to be very intentional about how we manage the headcount in the corporation. We are protecting this house as a primary objective. And we have invested very heavily now for the last three and a half years, for sure, on headcount. And we have what we need. Where we are investing, and we'll continue to invest, primarily will be coders, people that actually write the code and also people that are actually responsible for the customer relationship and carry a coder. So we're going to be very, very intentional. And I'm really super because we're in great shape on our workforce. We are really happy workforce. Our retention rates are better than ever.

CFO Mastantuono again on topic of hiring trends:

If I could just add, we're entering 2023, and Bill alluded to this earlier, we're entering 2023 with significantly more ramp reps than we entered into '22. So that growth. Yes, we might have had a little bit of a slowdown in hiring in Q4, but that was not on coder-bearing sales or engineering. We're entering 2023 from a ramp rep perspective, very strong, which gives us confidence not only with the pipeline we're seeing, but with the productivity that we'll get out of those ramp ups.

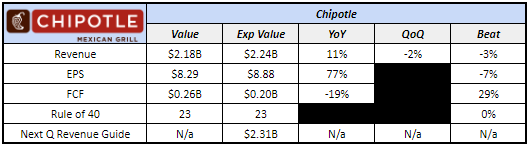

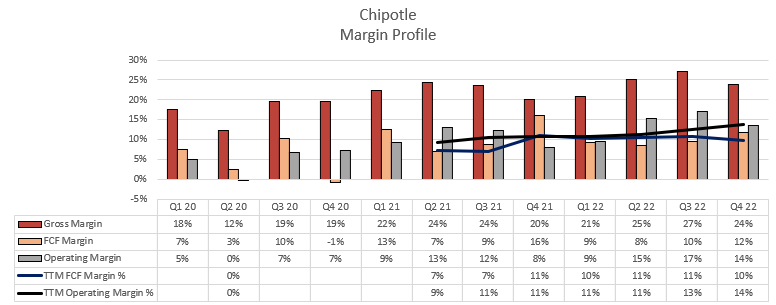

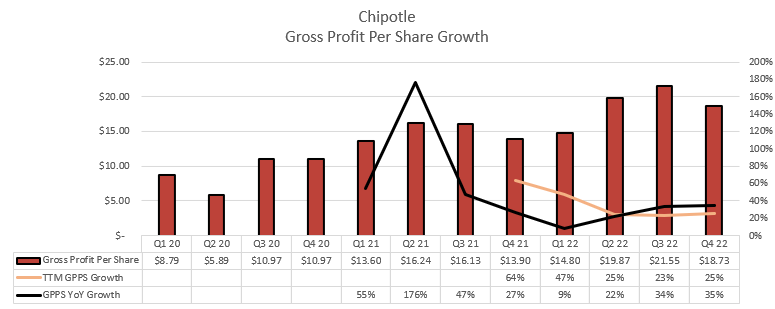

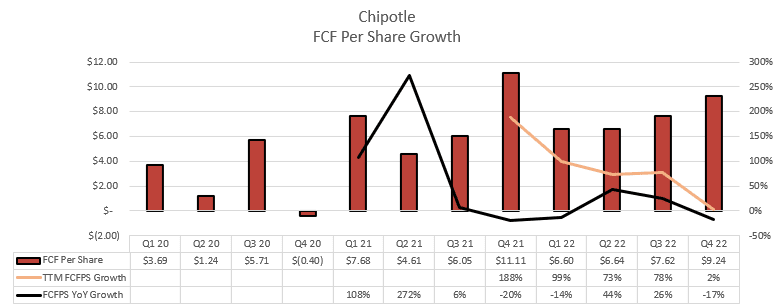

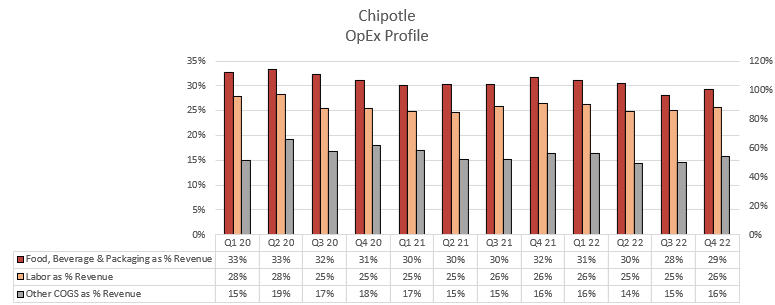

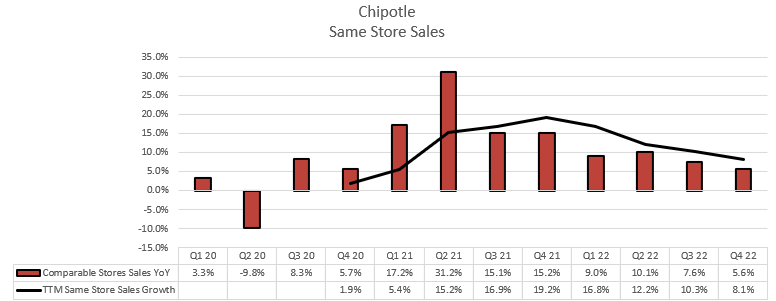

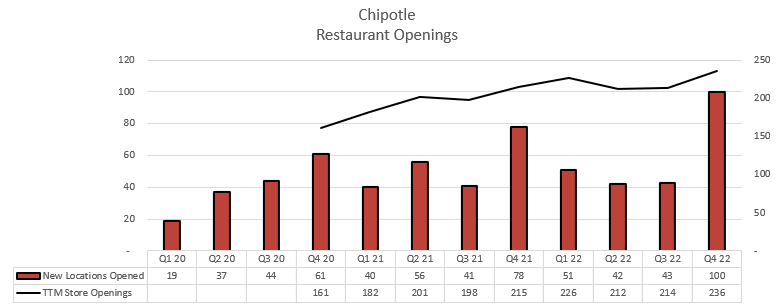

Chipotle CMG 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Brian Niccol on Expansion Plans for 2023:

We plan to open 255 to 285 new restaurants in 2023 with over 80% including the Chipotlane. Within our 2023 expansion plans, we will accelerate new restaurant growth in Canada and continue to open restaurants at a measured pace in Europe. In Canada, we have built out a strong local field leadership team that works closely with our U.S. team to ensure best practices and a consistent culture, while adapting to local needs. We are now ready for accelerated growth and plan to add around ten new restaurants in 2023, which will be the fastest development growth rate since we entered the Canadian market.

We also remain encouraged by the performance in Europe despite a challenging macroeconomic backdrop. In 2023, we plan to add a few additional locations in the UK, and we are also rolling out our digital capabilities to further expand access.

Niccol on Trends for beginning of 2023:

And basically, what we saw is as we exited the quarter, our transactions turned positive, and then we saw that continue to build in January. You are right, there was some Omicron and then there were some good weather. But what we've also seen is our staffing is at the best it's been.

Our turnover is at the best it's been in two years. And I think the combination of focusing on the basics, meaning no menu deactivations, keeping the lines open, both our frontline and digital make-line from open to close, teams deployed correctly, is also a key driver in why we're seeing the traffic progress in January throughout that whole month.

Niccol on different dynamics a Chipotlane location has in startup phase and compared to previous trends:

So for example, today, our restaurants open up on average around 85% of what our existing comp stores are doing. If you look back three years or four years ago, we were in kind of the high 70% range or so. So there’s been a step change. And the biggest thing that’s happened from the three years, three and a half years ago to today is we’ve moved from having just a handful of Chipotlanes to having the majority of our portfolio is Chipotlane.

And we still – when we look at what our Chipotlanes are doing, the 85% compared to 15% without a Chipotlane, they continue to outperform that non-Chipotlane cohort. So, we think the main driver is the Chipotlane and the convenience that our customers find with that digital drive-through.

Niccol on digital eating trends:

One is, we’re having a surge in return to in-restaurant. And so that part of our business is growing very, very healthily throughout the last year and a half or two years since we’ve been moving away from the pandemic.

But secondly, delivery has been declining as well. Delivery transactions in the fourth quarter declined 15%, and that’s I think just again a normal kind of move away from people getting out and about. And we figured that digital would kind of settle in this high 30% range. And so we’re at 37% range now.

CFO Jack Hartung on pricing outlook for 2023:

We’re running right now in that kind of 9% to 10% range. And as I mentioned, it rolls off early in Q3. And then in – I’m sorry, early in Q2 and mid-Q3. And then there were a couple of delivery adjustments, target adjustments in there as well. We’ll end up being somewhere in that kind of mid-single-digit because by the time you get to the end of the year, we’re running basically zero pricing. So overall for the year, it will be somewhere in that kind of mid-single-digit.

Hartung on early volume and mix trends for 2023:

I mean, right now, we're running, call it mid-single-digit positive traffic. We expect for the quarter, that guidance range assumes that we're also going to be positive transactions more in the low-single-digit as we move away from Omicron. Pricing will be that 9% to 10% range that I mentioned. And then there's going to be a mix component. We think it's kind of probably be in that low maybe 2-ish, 3-ish percent something like that. Mix is a little harder to predict, but those are the main components.

Hartung on timing of company record 100 restaurant openings in Q4:

We opened a record 100 restaurants during the quarter, but it was very, very back-loaded. Our teams did a great job of just scratching, clawing and doing everything that they could to get the restaurants open. And I think we probably had a record opening in the month of December as well. We had more than half of the openings or in the last month of the year. So yes, you're not – you didn't see a typical sales flow-through, considering we opened 100 restaurants.

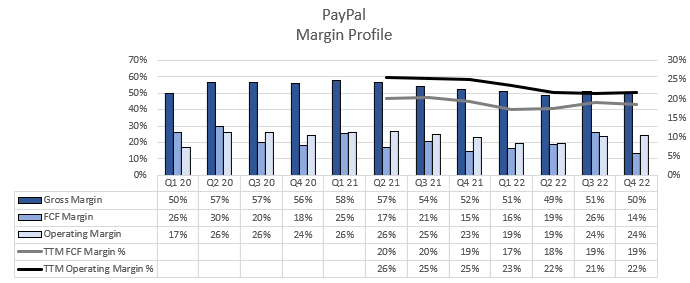

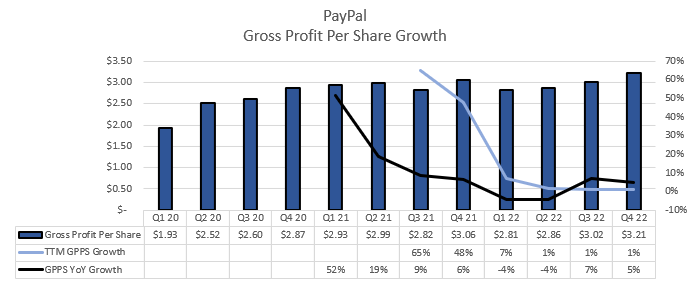

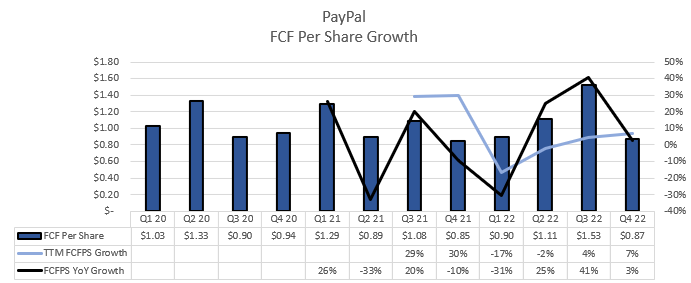

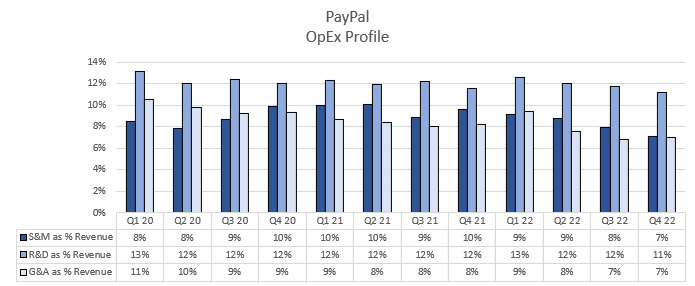

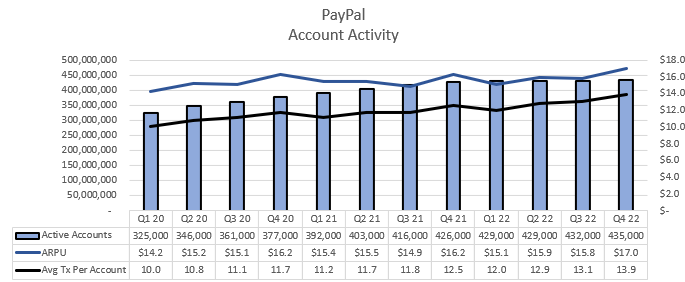

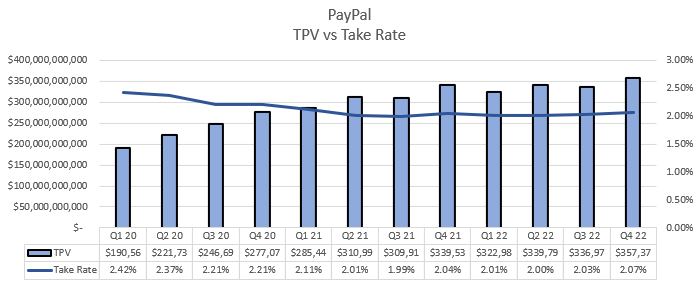

PayPal PYPL 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Dan Schulman on cost structure outlook for 2023:

As we look toward 2023, I want to lay out our thinking about the year ahead. First, we have identified an incremental $600 million of cost savings on top of the $1.3 billion of cost savings previously identified. This includes the very difficult decision to reduce our headcount by 7% as we continue to improve our processes and sharpen our focus. We will also continue to reduce our external vendor spend and real estate footprint.

CEO Dan Schulman on migration process for latest checkout tech:

In 2021, approximately 20% of our top 100 merchants were on our latest checkout experiences. At the end of 2022, one-third of our top 100 were in our latest checkout integration. And in 2023, we are targeting to be approximately 50%.

CEO Dan Schulman on guide considerations and early signs of Q1 performance:

And frankly, Darrin, Q1 is off to a very strong start for us. We're seeing widespread acceleration both in January and February. We're seeing it in branded checkout, which has stepped up quite nicely from Q4. We're seeing it in our Braintree services as well. Buy Now, Pay Later continues to accelerate for us. So, much stronger than we expected.

We wouldn't say 9% if we didn't feel confident in that number, as well as the 24% at the midpoint on our EPS guide. There's still a lot of the year ahead of us, right? We're five, six weeks into the first quarter, but it's clearly off to a very strong start, and we will have more as we report out Q1 earnings, as we look into Q2 that may inform how we're thinking about the full year.

CEO Dan Schulman on success of new mobile checkout technologies:

What's interesting is when you look at mobile checkout, it's clear that somebody like Apple has some inherent advantages in authentication, exclusive use of the NFC chip. But if you look at where we have implemented our most advanced checkout flows, and as I mentioned in the script, now about a third of our top 100 of our most advanced checkout flows, there, even in mobile, we are gaining share.

CEO Dan Schulman continuing of topic of next gen checkout and how they’ve gained share of developer with new checkout technologies:

I mean, whether you look at what we've done in Braintree to harden the infrastructure, to create additional capabilities over the holiday season during the Cyber 5, we were five 9s and above in terms of availability. And you see that in terms of kind of the new sales, people moving more volume over to us. Braintree's auth rates, something like 390 basis points better than the competitive set. And so, a ton of investment there and making a lot of progress.

We've put a lot of investment against PPCP, which is our unbranded, small, and midsized and channel partner play. And by the way, it's not just unbranded. It has our most advanced checkout flows in it, and we're going to probably take about 20% of our TPV through PPCP with integrations through Shopify, Adobe, TikTok, and move that to our most advanced checkout flows. And so, that, we've invested in, and obviously, the rest of checkout, right? Like things like our SDK and APIs, two years ago, we were not really playing in that developer market. And today, if you go to Postman, which is like one of the largest sites that developers go to, to look at SDKs and APIs, we're now one of the top 10 requested SDKs and APIs based on both popularity and quality of that. We actually are No. 7, No. 8 to Stripe. And so, we have really gone from almost nowhere to top 10 in terms of our SDK and APIs.

CEO Dan Schulman on balancing Braintree overall strength and margin pressure to overall PayPal margins:

So, there are a number of high-margin businesses that we add on to Braintree. Braintree itself is a lower-margin business. And by the way, we're serving the highest end of the customers that always have a lower margin structure for us. But a lot of the higher-margin businesses that we had into PayPal or things like risk as a service, we'll be introducing FX as a service, payouts is a higher margin. We're expanding Braintree into both Europe and South America, which are higher margin for us. So, we expect to see unbranded, as a whole, that margin structure move up.

And then as we go into the small and midsized merchant with unbranded, that obviously is a much higher margin. PPCP, is more of a, call it, sort of a mass customization platform. Braintree really is a customized platform because each one of those merchants have unique needs that we need to customize for.

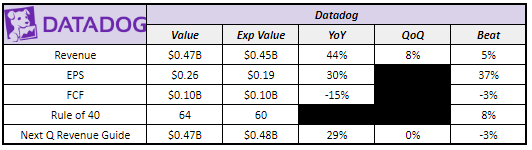

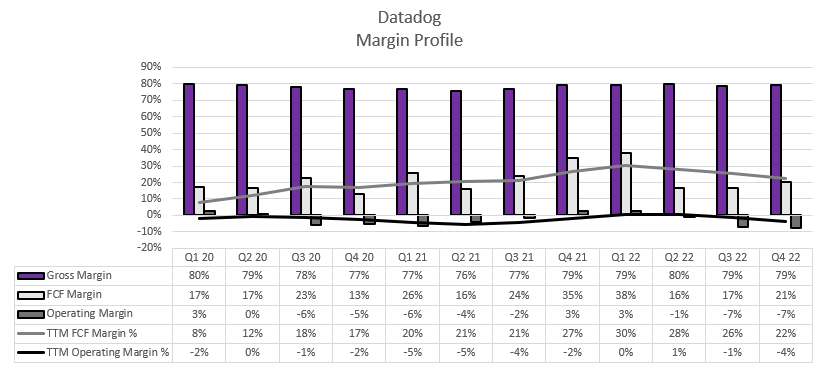

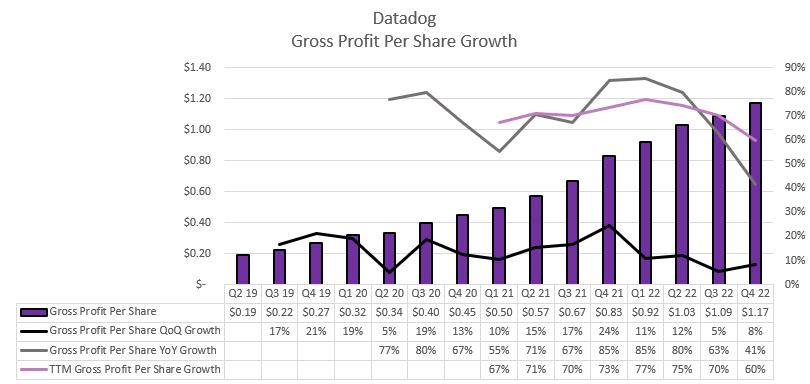

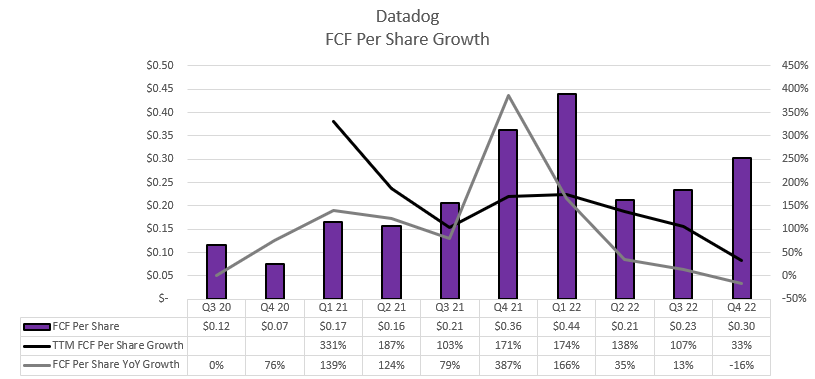

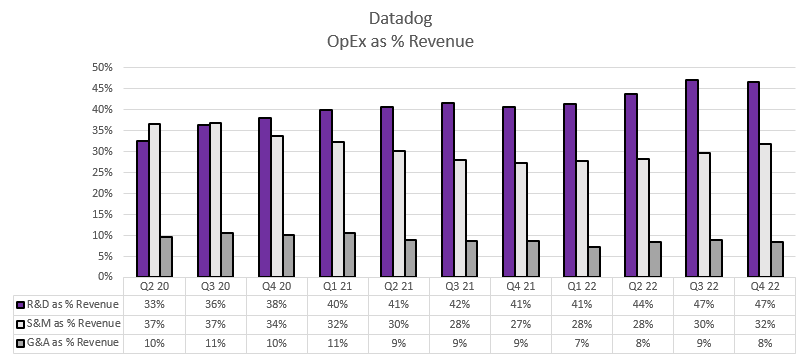

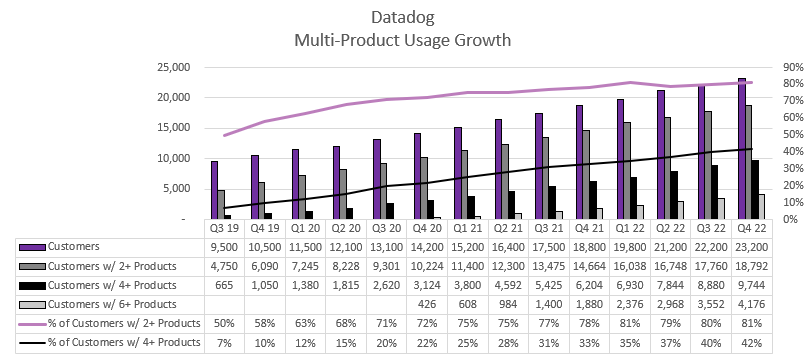

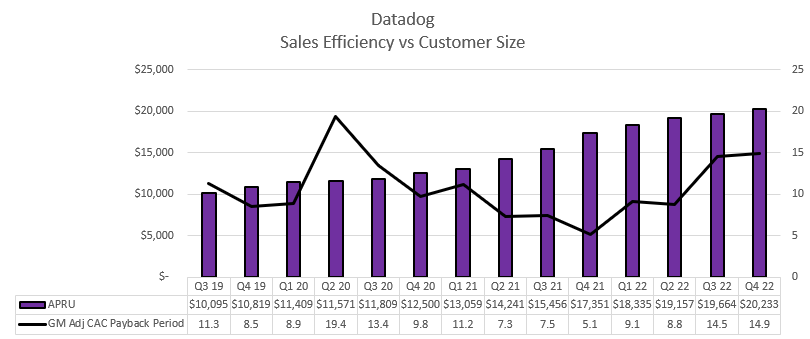

Datadog DDOG 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Olivier Pomel on usage trends in Q4 compared to the rest of 2022:

Overall, we observed slower user growth with existing customers, while continuing to scale on new logo acquisition and new product cross-sales. Starting with usage. Usage growth of existing customers in Q4 was overall slightly lower than what we observed in Q2 and Q3, which we attribute, first, to a continuation of cloud cost optimization by our larger-spending customers; and second, to a seasonal annual slowdown in the second half of December that was more pronounced than in previous years.

CEO Pomel on net new logo lands in Q4 and F500 update:

First, we had our strongest new logo quarter to date with a record level of new logo ARR bookings. Second, our sales pipeline remains healthy as our pattern of new logo and cross-sales is scaling above the levels of the past years, and we see demand growing along with our investments in go-to market. I'd also like to point out that although we have made steady progress, we still see significant opportunities to grow our penetration in total spend amounts with larger customers. As a data point, as of January 2023, 37% of the Fortune 500 are Datadog customers, up from 30% last year. For these customers, the median Datadog ARR is in the hundreds of thousands of dollars.

CEO Pomel on 7-figure federal contract won in quarter with recently awarded FedRAMP Moderate authorization:

Next, we signed a seven-figure land deal with a major federal government agency. This agency was looking to reduce tools sprawl and aimed at a rapid rollout to hundreds of different programs while saving money on engineering and issue resolution. This agency is among a number of new government customers in 2022, following our FedRAMP moderate authorization. And this deal is expected to displace at least eight commercial legacy monitoring tools.

CFO David Obstler on what drove the record new logo ARR in Q4:

In Q4, and I think going forward, we continue to see greenfield and new projects, new workloads being the majority of the driver, but have seen over the quarters. And we talked about some of them in our prepared remarks, consolidation opportunities. When a client is already in their cloud journey and has workloads and is looking to get a platform, create efficiencies, etc., they have increasingly been consolidating on Datadog, and we see continued opportunities for that.

CEO Pomel further color on optimization trends they’re seeing:

What we see, though, is that customers save money where it matters, which tends to be the very large line items, which for customers that are fairly far along into the cloud, is going to be, first, their cloud provider deals that are, again, one or two others are larger than their observability bills. And then, we're going to be affected by that and maybe with some optimization more specific to observability as well. So, that's what we see there.

The last thing I will say is on the very low end of our customer base, we do see impact of the macro environment. We have a little bit more churn at the very, very low end, which is what you see our customer count not going up as much despite us having very strong notable quarters.

CFO Obstler on guidance philosophy and conservatism embedded:

I think we've continued to use the same approach, which is to look at the history and discount the major assumptions, which are the organic growth or the expansion of existing customers and new logos. I think the difference in the actual results were the periods of times where we saw more than pro rata or more than historical adoption and growth of existing customers, the ratio between that discount and where it ends is up actuals ended up larger. But the intent and the strategy of providing this guidance on conservative assumptions relative to that has not changed.

What we've seen over the past few quarters, basically in the second half of 2022, we assume it's going to continue. We know it's going to end at some point, but we don't know when exactly. So, we're not building that into our guidance.

CEO Pomel on why they’re continuing such large investment into S&M for 2023 with a challenging macro backdrop:

In the end, the reason for that is we still have ground to cover. We still have segment and geographies to cover. And also, as we mentioned earlier, we're having actually great success when it comes to landing new logos and new products with customers. So, our sales interactions are productive.

Our return on investment is there. So, we need to keep doing that. Again, these are the seeds of future success we are planting, and we don't intend to stop.

CEO Pomel if they’re seeing optimization efforts in specific Datadog products more than others:

Some of it happens more directly at the observability level, logs in particular or some aspects of APM that are transaction-based where we see customers optimizing there and making sure they get the best value and cut the noise. But as a result, we see fairly similar trends across the products, so that's why we didn't call out anything specific in there.

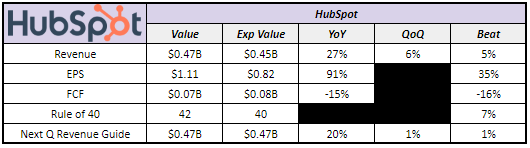

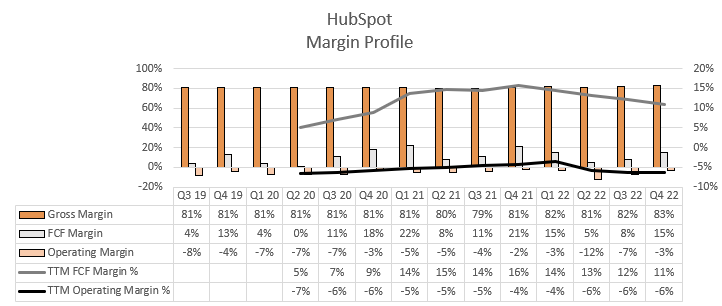

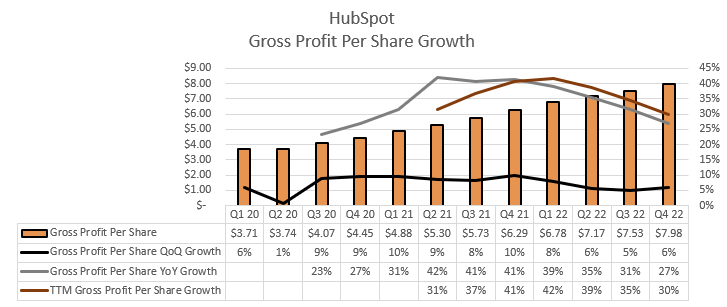

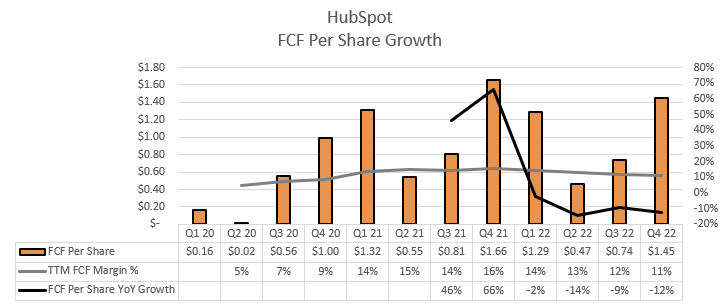

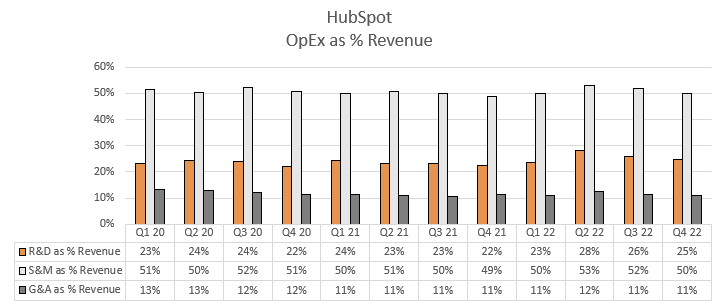

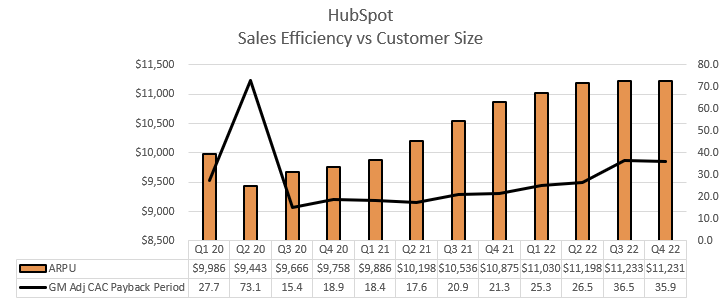

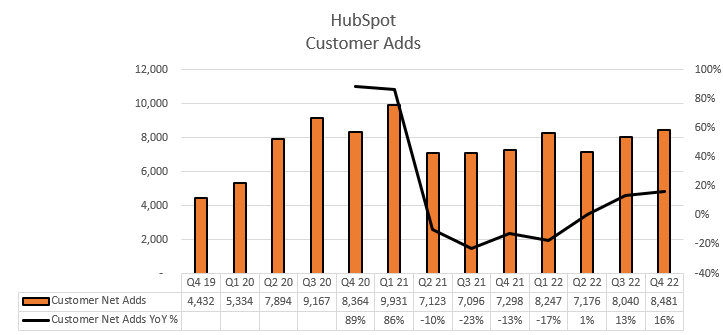

HubSpot HUBS 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Yamini Rangan on the decision for 7% RIF and what that means for 2023:

And if we step back, this is not simply a short-term cost-cutting decision. This was a strategic realignment of our people and investments so we can drive long-term profitable growth. And there are two reasons why we got to this decision. The first is that we had areas within the business where headcount had grown faster than revenue, areas like recruiting and services. And even when we consider 2023 growth, we had that excess capacity. So we wanted to ensure that our people and our resources are clearly aligned to the growth in 2023 and our strategy in 2023.

The second rationale is that we want to invest thoughtfully in key areas of the business to drive profitable growth over the next decade. We want to invest in product innovation so we can drive customer outcomes and emerge stronger from the cycle. We want to invest internally in our own systems and automation, wherever we find there are manual processes, so we can be even more efficient and innovative as a company.

CFO Beuker on margin outlook for 2023:

Most of the operating margin increase we expect from our restructuring will be realized in Q2 through Q4 of 2023 and is included in our guidance. We expect non-GAAP operating profit margins to be between 9% and 10% in the first and second quarters, low double digits in the third quarter and high teens in the fourth quarter. We expect capex as a percentage of revenue to be roughly 5% and free cash flow to be about $225 million for the full year of 2023, with seasonally stronger free cash flow in Q1 and Q4.

CFO Bueker on guidance assumptions for macro environment in 2023:

The baseline assumption in our 2023 guidance is consistent with Yamini's description of the environment, which is it stays difficult, but it remains very consistent with what we saw throughout Q3. It doesn't get materially better, and it doesn't get materially worse.

Now that said, as you know, we always try to set guidance that contemplates a variety of outcomes, and we did the same thing this time. And so we feel good about our guidance with that set of base-case assumptions, but we also feel good about that guidance even if the external environment gets a little bit worse from here.

CEO Rangan on partner channel commission updates and strength of channel:

And our partner-influenced MRR or ARR is about 45% compared to the overall. So it's a good split between direct and partner-influenced MRR. We have momentum. We are co-selling much better over the last three years, and partners are behind us.

Now I did mention that we are making a structural change to the commission. If we step back, our partner commission was initially set up when HubSpot had one hub and just a couple of additions. This is like 10 years ago. And then as you all know, over the last couple of years, we have expanded our product portfolio. We have added Operations Hub, we've added CMS Hub, and we've added more additions to the hub. So as we step back, and we looked at our partner commission strategy, we want to incentivize our partners who are now coming along this journey with us to do a couple of things.

CFO Bueker on NDRR outlook after tipping a couple of points from Q3:

And it's really that net upgrade motion that has been challenged in the economic environment as customers are both slowing the rate at which they are upgrading, but also have a bit of a sharper eye on their overall spend with HubSpot. And so we're seeing pressure, both on the upgrade side and also on the downgrade side. And in the near term, we expect that, that pressure will remain. We actually think that net revenue retention is likely to tick down again in Q1.

But we feel really good about our ability to hold net revenue retention above 100%. Over the longer term, we continue to believe that we can deliver net revenue retention of 110% in any healthier macro environment.

CFO Bueker on the puts and takes of two consecutive strong quarters in net adds on free tier:

This is now our second quarter of really strong net customer adds at the low end. We are seeing really nice sign-ups of our free CRM. We're seeing the free CMS really resonate. And it's that sort of sign-up volume converting into our Starter tier that is driving a real strength in net customer adds. Now like -- as you know, there's push and pull across ASRPC and net customer adds when it's being fueled by that low end of our bimodal.

CFO Bueker on what has driven those strong customer adds in the free tier:

We do feel like the momentum in the Starter customer adds is a great long-term strategy for us. In terms of what we're seeing today around Starter upgrades, the newer cohorts that have started with us are actually upgrading at pretty healthy rates.

We took a number of actions last year to solve for the customer to really drive that volume that we're seeing at the lower end. We talked about things like bringing marketing automation down, introducing the free CMS. And we continue to experiment around pricing and packaging. All of that has resulted in like a nice expansion of the number of Starter customers that are joining us.

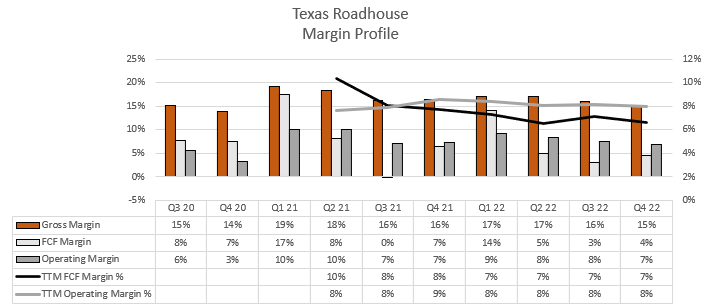

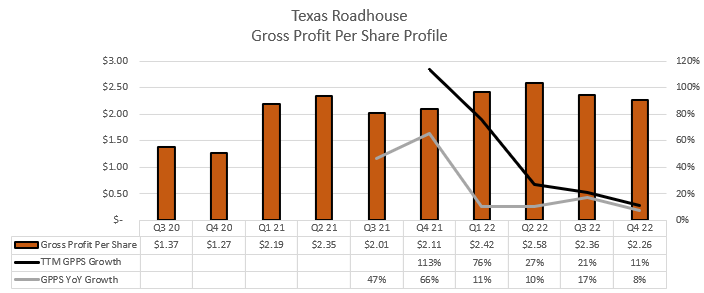

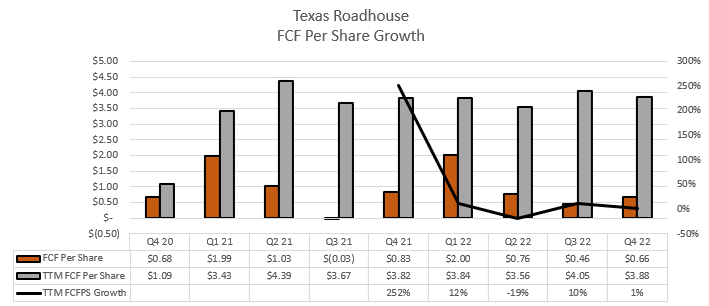

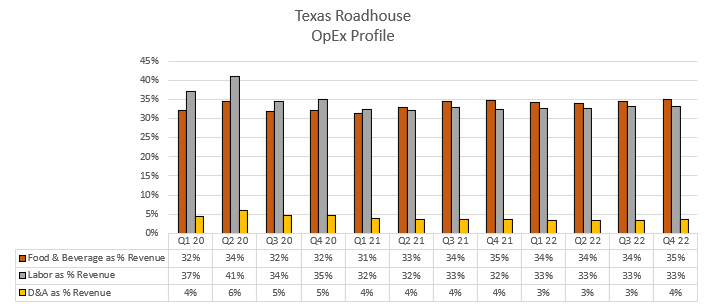

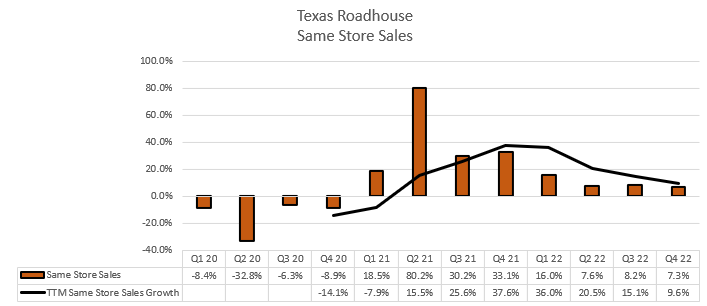

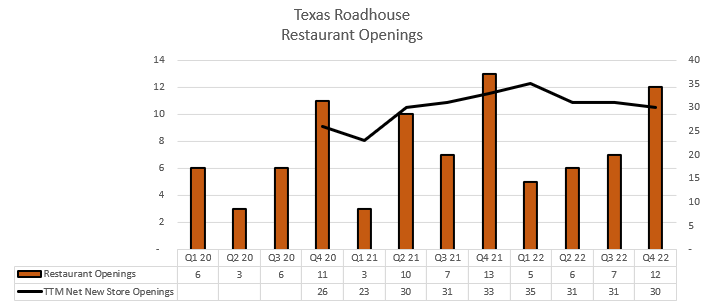

Texas Roadhouse TXRH 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Jerry Morgan on Store Location growth in 2022 and guidance for 2023:

Moving on to development, we opened 23 company restaurants across all concepts in 2022. And in 2023, we expect between 25 and 30, Texas Roadhouse in Bubba's company openings, as well as three daggers. Our franchise partners open seven international Roadhouses in 2022, and we expect them to open as many as 12, International and Domestic locations in 2023.

CFO Michael Bailen on 2023 traffic trends comping over Omicron:

Turning to 2023, weekly sales averaged over $146,000 for the first seven weeks, with comparable sales of 15.8% as compared to the same period in 2022. We do not expect this level of comp growth to continue, as we move past the lapping of Omicron and go up against higher traffic levels in the coming weeks. At the same time, we do not want to downplay the current results, as our restaurants averaged more guests over the past seven weeks than in any period in our history.

CFO Bailen on commodity inflation outlook for 2023:

For 2023, our commodity inflation guidance remains unchanged at 5% to 6%. We also continue to expect that the majority of inflation for 2023 will be driven by higher beef costs.

CEO Morgan on the driving forces to a strong start to 2023 past easier early comps:

Yeah. And I would say, we've been very good on gift card redemption, and there's been some driving forces with some great weather across the country and some enthusiasm out there. But I think there's a couple of reasons why it's being aggressive right now, which we're excited about, how long it will hold at that level.

CEO Morgan on the path for yearly restaurant growth to eclipse that 25-30 range in the future:

I do believe that we will continue to focus on the growth of Roadhouse at that low-20s. And as we kick Bubba’s in also as we start working towards a double-digit number, and then you know, Jaggers is still a little bit early to see what we can put into the pipeline. I am excited about it. I do believe that it will continue to add to our portfolio. So I do believe that we can get to the high-20s and low-30s in the next couple of years is where our target focuses and our pipeline.

And then I do see it escalating from there. It will be incremental, but it's not going to be a big jump. But as we do get more aware of what we can do with Jaggers and Bubba’s, they will be there. But we're very comfortable with where Roadhouse is in the pipeline for the next three years, I would say, we could be at that number and the other two will be the driver to kick us up over into the 30s or higher.

CFO Bailen on pricing mix through each quarter this year without any further announced increases:

So first quarter, with a 2.2% and assuming, we don't take any pricing in October, we will have about 5.9% pricing for the first quarter 5.6% in the second quarter, 5.1% in the third quarter, and then 2.9% in the fourth quarter.

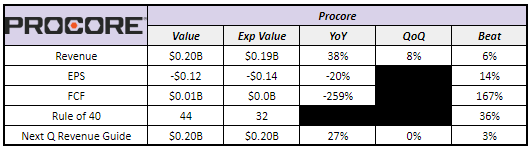

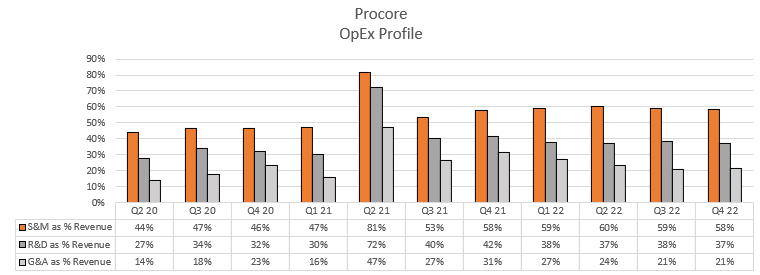

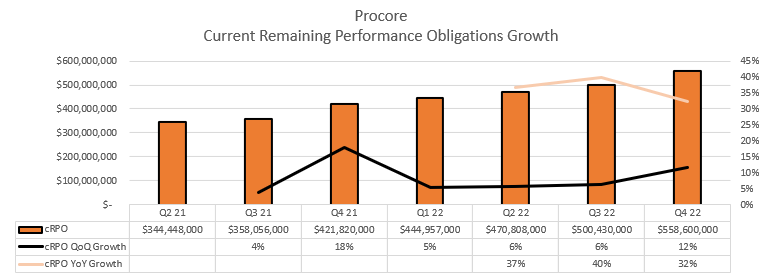

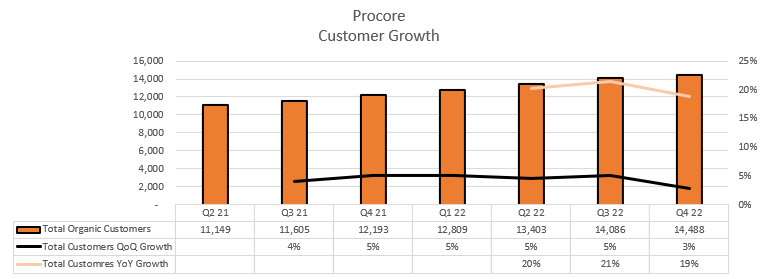

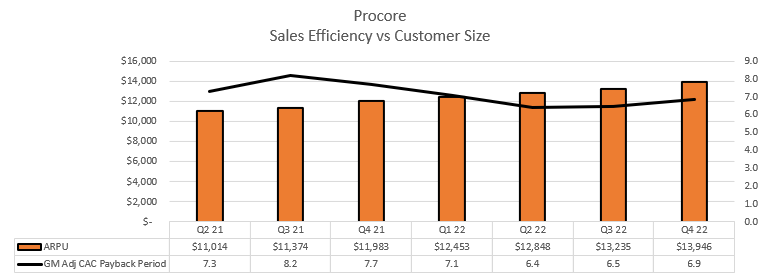

Procore PCOR 0.00%↑

Quarter Results:

PnL & KPI Tracking:

Earnings Call Quotes:

CEO Tooey Courtemanche in prepared remarks on competitive environment:

Our strong performance was underpinned by the strengthening of our leadership position within construction. For example, in 2022, we saw one of our largest competitors less frequently than we did in 2021, yet we won more ARR against them. We believe this is a testament to our significant value proposition and the widening of our competitive moat as well as cementing Procore as a clear leader in the industry.

CEO Courtemanche on priorities for 2023:

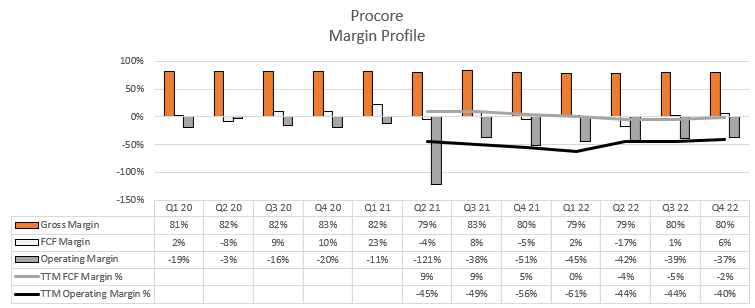

Historically, we have typically delivered one or the other from significant margin expansion in 2020 during COVID, to investing over the last 2 years to reaccelerate growth. We believe the business has reached a level of scale where we can accomplish both, delivering growth while showing efficiency.

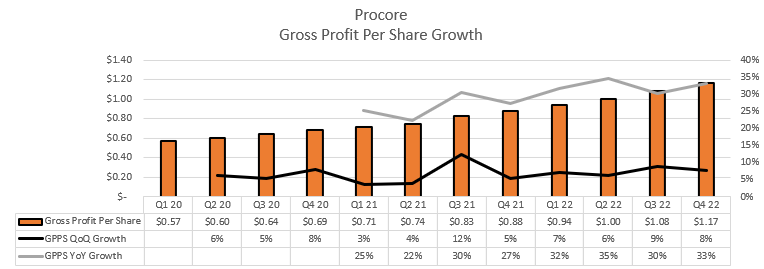

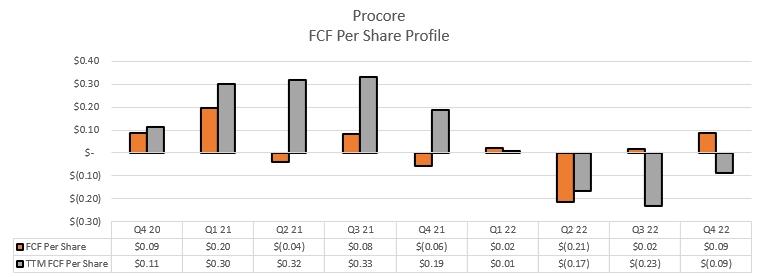

I want shareholders to know that efficient growth is a mantra we are instilling in the DNA of Procore. We discuss it at every chance we get at the leadership team level and within employee all hand meetings, because every team member has a role to play in ensuring we operate more efficiently without sacrificing our growth objectives. Ultimately, I expect our commitment to efficient growth to translate to continued improvement in free cash flow and per share metrics.

CFO Paul Lyandres on philosophy behind 2023 guidance:

We set our revenue guidance at a level that we have a very high conviction we can deliver on in almost any environment, though we do not optimize for a consistent magnitude of upside to that guidance. We are taking a prudent approach and have factored in continued external uncertainty and potential for weakness in the economy.

CEO Courtemanche on hiring outlook for 2023:

So we are being very intentional and trying to be very thoughtful as to our hiring strategy. The headline is that we are going to continue to hire through the end of the year. We are going to be very focused to make sure that we have the quota carriers online in order to make our numbers. But ultimately, what I want to kind of state to everybody is that we’re being very intentional here because of that – the concept of efficient growth. And so we’re making sure that every head that we add is absolutely necessary in order for us to meet our objectives.

CEO Courtemanche on M&A outlook after now fully lapping Levelset acquisition:

I think right now, we feel really good about the depth of our product portfolio. We feel like we still have more work ahead in terms of just the areas we want to drive our own business value, that we are certainly always staying close to our partners, the benefit of our app ecosystem and what we have built in terms of our community means that we have incredibly strong relationships with these folks, continue to drive more and more partnerships. But you shouldn’t look to us for doing any meaningful acquisition anytime soon.

CFO Lyandres on Free Cash Flow outlook for 2023:

So, like we have talked about before, the free cash flow margin improvement should be a little bit ahead of what we see in terms of our operating margin improvements trajectory of 350 basis points on average per year. Of course, free cash flow is not something that we officially guide, but we do manage to overall free cash flow on an annual basis internally. And it’s a very focused metric that we have, both in terms of magnitude as well as on a per share basis.

CEO Courtemanche on decision to have CFO transition to President of Fintech to oversee Levelset and overall group:

Adam, also it dovetails very nicely with the fact that we now have integrated a lot of [Levelset] already into Procore. And so now it’s time for a leader to come in and build on that foundation and launch us into growth mode. And that’s one of the reasons why now it’s the time for Paul to take on this role. And also, I do want to point out that I wouldn’t be this confident in this move if I didn’t have a great relationship with Howard [Fu, President of Finance & incoming CFO]. He both is a great partner, but also challenges me on where I need to be challenged, which is what you want in your dynamic between your CEO and your CFO, right, Howard? So, anyhow, yes, I think this is a testament for why it’s time for Paul to take the helm.

CEO Courtemanche on any demand trends from first six weeks of 2023:

No, nothing significant to report, nothing that has really been changing. I will say that the sentiment of the customers I talk to remains very positive and optimistic going forward, and backlogs do remain strong. So, we are feeling pretty good.

CEO Courtemanche on the changing importance of pre-construction planning:

But to your point, there has been a realization, not just because of the macro, but this has been over the last 3 years or 4 years, that preconstruction is where all your money is won and lost on the project. And so a lot of effort is being put on that. And the cool thing is, because you can’t – they can’t put more people to work, Procore provides them the ability to do more with less people, right. The quote that we had in the earlier stat was that Procore enables our customers to run about 50% more construction volume per person, which gives them a force multiplier to be able to create more throughput and revenue.

CEO Courtemanche on internal operational challenges they’re facing in International markets:

It is strictly, in our opinion, an internal operating challenge, not an external macroeconomic challenge. And actually, you may ask the question like, how do we know that, well, we actually look at all the territories in which we are selling. And we can see that in each one of the territories, we have highly productive and successful sales reps, but we also have newer reps that have not ramped yet that are having a little bit more of a challenge. So, we believe that getting our reps more ramped more rapidly is one of the keys to us driving success.

My Take

To me this was a pretty funny set of earnings calls we got to listen to, where there were many of the same questions throughout all calls even across completely different industries:

Asking about full year guidance philosophy in as many different ways possible

Guidance on OpEx and headcount

Can you please make year-long assumptions for me off first six weeks of year? Thx

Questions on buying appetite and desires for expansion/renewals

I’ll preface this by saying some of this can be clouded by how much of a sweet talker management decides to be, but one of my takeaways was their language around assumptions in their full-year guidance. Companies like PayPal and Procore were adamant to say their guidance is for a number they feel they can hit in any sort of environment, but others used language of “assuming things stay the same” like Datadog.

Speaking of Datadog, I did bucket them in the not-so-great category more for their guidance and then a kind of weird earnings call where they acknowledge their largest customers are optimizing and seeing pull back on commitments, but still have pretty aggressive OpEx forecast and seem to plan on investing through this all like normal. You can already see this in their margin trends since Q2 22 and it makes me a bit nervous since I do think there’s a non-zero chance their customer environment could get worse.

Now on the positive side, Datadog did report their best ever quarter of new logo ARR and first big fed contract which is something I’m excited to see. ServiceNow has been excelling through this macro in part because of their high FedRAMP clearance and ability to execute in winning large contracts from public sector. Management is also known for giving very conservative guidance, so maybe I’m reading a bit too much this all. @FromValue on Twitter had a great post showing every FY guide they’ve provided and execution on that, which is quite impressive but might just be a nature of visibility into a consumption-based model:

Procore is one of my smallest positions but I found myself most impressed with not even necessarily their reported numbers, but with the earnings call and felt it was more of substance than the others I listened to. This might just be a function of how new I am to this name but I came away quite impressed with the management team and backdrop of Procore. Fun being wooed back into a -40% operating margin software company lol!

One thing to note is I had previously planned on including Floor & Decor FND 0.00%↑ in this newsletter, but recently sold my shares after their earnings report due to guide down in store openings and further margin deterioration. I'll go over this more in my portfolio recap newsletter at quarter end, but I'm sure it's a company I end up owning again in the future.

The last thing I’ll say is how Andy Jassey joining the Amazon earnings call was a real treat. I would really suggest listening to that earnings call to listen to everything he had to say, but this was his first time doing this and we got some great insight into how he looks at 2023 and operating progress. The AWS language of current mid-teens growth though is quite alarming and could really pose problems for the company to hit the turnaround bottom line targets this year unless retail really picks it up.

-Sean