Q1 2022: Earnings Review Part 2

Q1 2022: Earnings Review Part 2

The Jiggy Capital Newsletter #14

Back at with Earnings Review Part 2! This will be a different kind of edition due to the fact I’ve had quite the amount of portfolio turnover over the quarter. I’ll be catching up on the new positions since last update that had previously reported as well as the 4 I had left remaining that hadn’t reported.

The length of each company’s write up section will vary on the amount of KPIs the company discloses and the amount of good insights to share from their numbers. My hope is you’ll get an idea of how the company performed against expectations, the trends behind their numbers, and some quotes from the Q&D portion of their earnings call.

If I had to segment the quality of reports between the remaining nine companies, it would go as follows:

Great: MongoDB, Crowdstrike

Good: Snowflake, Sprout Social, Paycom, Synopsys

Average: Applied Materials, Lam Research, Cadence

Although I try to stay objective when assessing progress of companies I own, I’m no doubt biased when I say I honestly thought all of the reports were quite solid with pockets to get really excited about in each.

Now let’s get into individual reports!

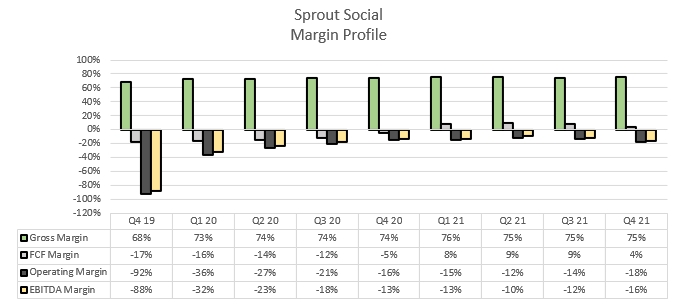

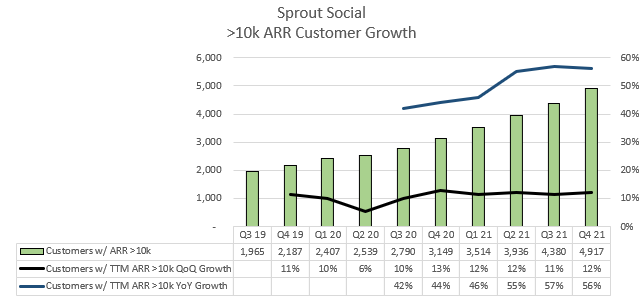

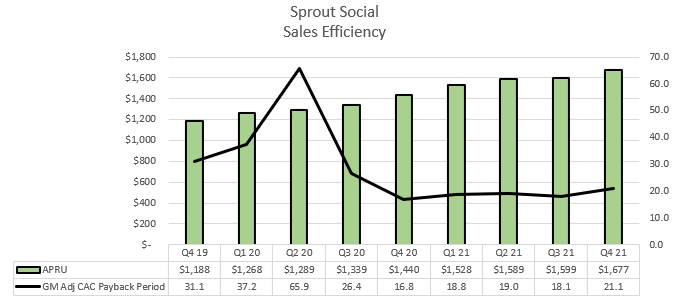

Sprout Social

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On NDRR expansion outlook:

We are accelerating seat expansion, changing segment mix and rising attach rates of our premium modules are each structurally improving our expansion rates. We believe there's a strong multi-year runway to further expand dollar based net retention from current levels.

- CFO Joe Del Preto

On R&D investment priorities:

One of the things that we're doing on the R&D side, to really lean into that is thinking about the kinds of tools and capabilities that larger teams need, the tools that they need to collaborate more effectively to work as large organizations with potentially many, many use cases, large volumes of messages

There's a good chunk of the roadmap that is dedicated toward just those more sophisticated use cases, generally, are we building and expanding against the social listening, the more complex customer care needs, things that really speak to those organizations that are a little further in their maturity curve.

- CEO Justyn Howard

The changing dynamics with selling upstream into mid-market and larger enterprises:

So in the mid-market and enterprise, specifically, those companies coming in, they've got bigger problems, they got bigger opportunities in front of them, they've got larger departments that are going to need access to Sprout. And so with that, it gives us an opportunity to start at a larger user account and start at a larger profile -- social profile level. So those things are all converging and providing a tremendous amount of opportunity for us. And we feel like there's a lot of positive tailwinds there.

- CFO Joe Del Preto

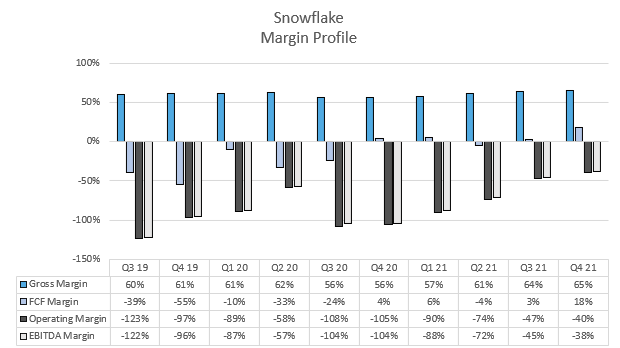

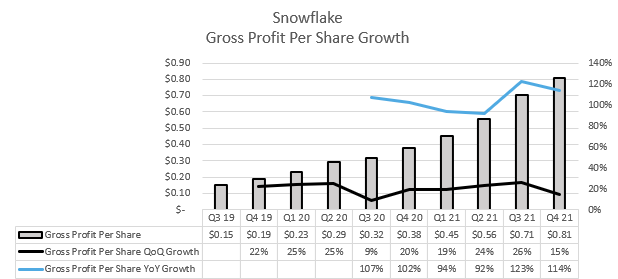

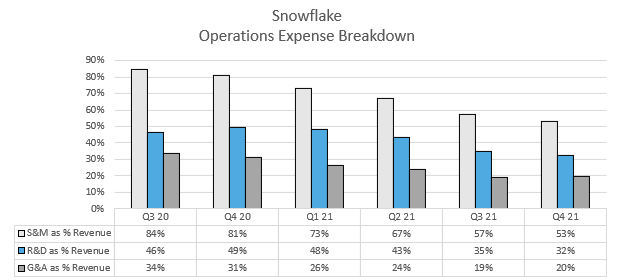

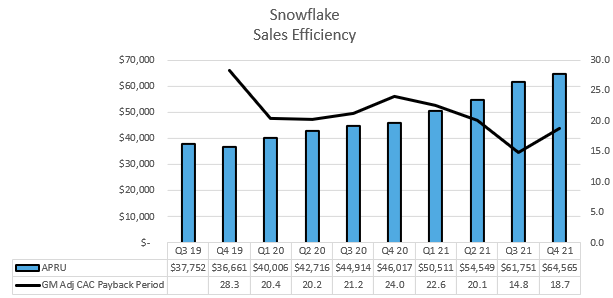

Snowflake

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On NDRR outlook:

It will stay above 150%, but it's not going to stay in the 170s.

- CFO Mike Scarpelli

On restructuring of sales org for larger accounts:

We really replaced the geographical backbone with an industry equivalent of that because we don't think, for a large account, the geographical breakdown really doesn’t add anything.

We've been talking on this call probably, I think, for the last four quarters about how we are really, in all aspects of our business, bringing a much stronger industry aperture to everything we're doing.

And today, nine out of 10 conversations are industry-specific, very, very industry-specific, oftentimes not necessarily with IT types but with businesspeople and data science types. People are really trying to drive predictive insights into the business, things that are becoming possible, have never been done before. So the company really wants to evolve toward this posture in the marketplace.

- CEO Frank Slootman

On Snowpark developments in Java and Python:

But if you just look at current adoption, Java is trending quite well. We see migrations from Spark, from Hadoop, and other workloads.

And I can also share that for Python, right now, we have way more customers requesting access to the preview that we can onboard currently. So they introduced super high. They generate a lot of consumption. Trends are very positive.

- SVP of Product Christian Kleinerman

On what stood out internally this quarter:

Where I was really surprised was the strength in bookings in the quarter. You saw that we closed over $1.2 billion in contract value in the quarter, growing our RPO to $2.6 billion. That was well above what we were planning internally.

The other thing I want to call out, too, is we co-sold with the cloud vendors, $1.2 billion in contract value for the year as well.

- CFO Mike Scarpelli

On tractions around data sharing:

And so historically, our business has been very -- much been a modernization play from existing workloads, and that's where you have to wait some time before people sort of get their sea legs under them and they sort of move on to these opportunities. But that is starting to change. As we said in our prepared remarks, I mean we now have 18% of our customers having at least one stable edge as part of their platform, and that was up from 13% last year. So the data cloud is really happening, and that is what a rapidly growing customer base underneath it.

- CEO Frank Slootman

On vision around Streamlit acquisition:

If you recall at Investor Day last June, we shared our vision to help organizations of all sizes build applications, data applications, and data experiences on Snowflake.

What we see with Streamlit is their super easy-to-use framework powering all sorts of applications both for internal consumption of data within companies but also coming to our marketplace and helping entire businesses, some of them industry vertical businesses, some of them horizontal experiences, but at the end of the day unlocking the power of data and creating new data experiences.

- SVP of Product Christian Kleinerman

On total data opportunity and where things are trending:

I think it's important for everybody on the call to understand that we are super early innings in terms of the total opportunity and what is -- what people are going to attempt to do with data. That's because the technology is running out front. It's enabling things that have never been done before. Now it's not like throwing a switch and all of a sudden everything is blinking green.

We're in conversations almost every day now with customers that are trying to do predictive things with data that they've never done before. And a lot of the challenges they have is with skill sets that translates from their core business to the data side and the gaps that exist there to make that all happening. So there's this very normal, natural friction in the evolution of that, that we're trying to learn how to do these things. And you see that in the world of machine learning a lot.

- CEO Frank Slootman

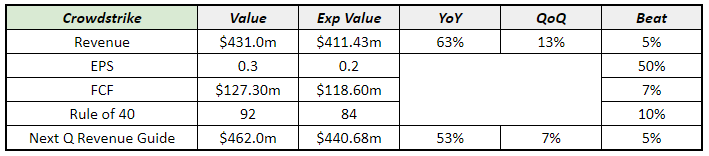

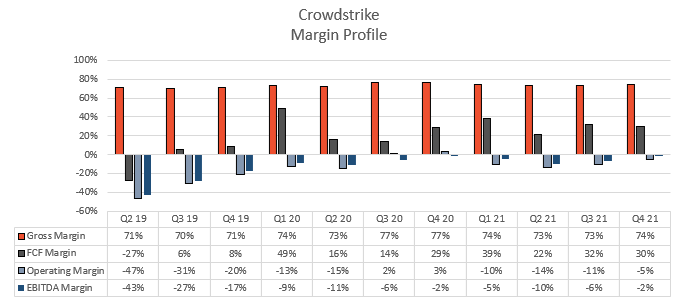

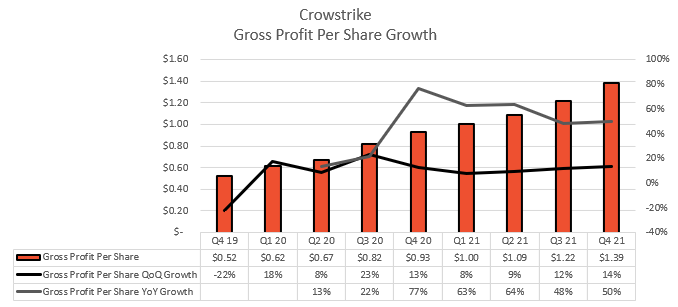

Crowdstrike

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On Identity Zero Trust module recent traction:

When you look at our Identity Zero Trust module, which came from the Preempt acquisition has now been integrated into the platform, which makes it seamless. It's obviously been a standout for us, because when we think about the threat environment, we've seen many of these breaches abuse identity, abuse directory services, and there's a massive compliance issue in just understanding, all of these accounts where they live and who has access to privileged accounts.

So, this is a highly differentiated module. Our competitors really don't have anything that's close to this. The way it works, the AI algorithms that we have built around it that we got from the Preempt team, and the expertise that we have in this area. So, it certainly is a big way for us to help differentiate the platform among many others. And it has been an absolute standout for us. And I think we've taken the time and effort to do the integration right, which is an important part of the way CrowdStrike looks at its platform.

- CEO George Kurtz

On what XDR means and how it differentiates the platform expanding upon EDR:

When we think about XDR, it's more than just the marketing acronym. And what we've seen in the past is that organizations of all shapes and sizes, security companies have tried to just slap XDR on what they have that's legacy. And we don't think that's the right approach.

We think you have to start with the best EDR in the market, and then you extend that. We believe our EDR is the best and we've been validated many times over in different places. And what we've been able to do is to leverage the very powerful, fast and efficient streaming engine of Humio. We just talked about the petabyte benchmarks to be able to combine that with our Threat Graph, apply AI on top of it to get the best threat detection outcome and response leveraging our fusion technology.

- CEO George Kurtz

On competitive landscape:

When we look at the competition, I think, this quarter, we put a punctuation mark on a competitive point. When you see the growth, you see the cross-sell, you see some of the modules outside of just the core.

We've never seen a better competitive environment for us. We're entering the quarter with the largest pipeline. We've got lots of replacements in the legacy world, lots of replacements in the next-gen world. And truly differentiated platform with our modules, we have 22, just to be clear.

- CEO George Kurtz

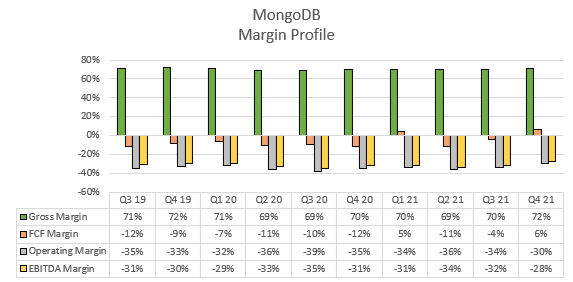

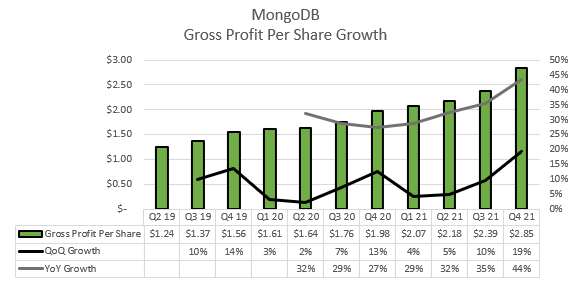

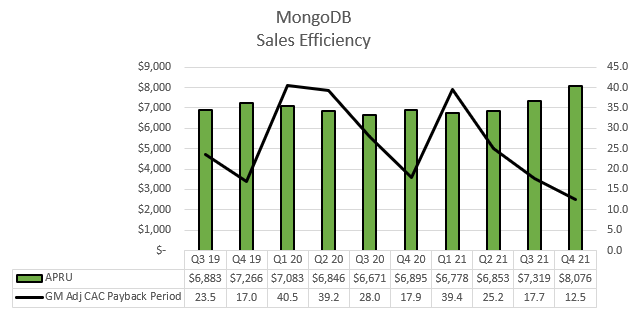

MongoDB

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On the types of workloads Atlas has been used for among different customer sizes:

I'd point to the seven-figure customers. The majority of those customers are on Atlas today. So we have large customers and actually even cutting-edge start-ups who are running mission-critical workloads.

For start-ups, it's probably their entire business on Atlas. For large customers, they're running mission-critical workloads. And so, Atlas is not just for small workloads. We are seeing -- and this has happened now for a number of years, we're seeing enterprises increasingly get comfortable with moving mission-critical workloads to the cloud.

And one of the benefits of moving to MongoDB is that you get real optionality of not just starting on-prem and moving to the cloud, but going from one cloud provider to another. So we're seeing strong interest -- and I think we have the customer proof points to give people confidence to really move mission-critical workloads to Atlas.

- CEO Dev Ittycheria

On how the GTM has evolved and will continue to evolve as they go from $1B to $2B ARR:

So we've constantly always tried to stay ahead of where the business is in terms of anticipating changes to our go-to-market model. I mean, as you can imagine, in the early days, we had one model, which is a direct sales force really trying to sell to everyone. Then we introduced an inside sales team.

Then we introduced self-serve. Then we've introduced the notion of having focused teams on high-end accounts. We introduced the notion of removing friction from the initial selling process to get customers on our platform more quickly. So we're always refining our go-to-market motion in anticipation of, one, how big this market is, and we try to meet customers where they are versus trying to force them to try to engage with us in one way.

And you'll see us continue to do that. We're going to be focused -- increasing on verticalization. As I mentioned in the prepared remarks, we are seeing a lot of traction in key vertical industries. We're developing a deep degree of confidence around those industries.

So you can see us continue to push the envelope in terms of innovation. And I would argue that we have the best sales organization in enterprise software.

- CEO Dev Ittycheria

On how their relationship with the hyperscalers has evolved in co-selling:

MongoDB is incredibly popular and the pot really spans all major cloud providers I think what we have shown first with Google as we started working with them very closely, given their ambitions to grow their business quickly is that we could partner effectively and help them acquire a lot of new customers, a lot of new workloads onto their platform. This did not go unnoticed by some of the other cloud providers, and we started going deeper with AWS.

As people may remember, in early 2018, AWS introduced a competitor, a clone of MongoDB and know some worries about how that relationship would evolve. And I'm pleased to say that I feel like the relationship has never been stronger. We have deep relationships in the field. We partner more on deals.

And AWS has recognized that MongoDB drives a lot of demand to their platform. And so, the relationship there is very healthy. And we're also doing a lot of business with Azure. So I would say our win rates are still very high against them when we go head to head against them.

- CEO Dev Ittycheria

On any changes in guidance philosophy:

The way I would think about it, Karl, is that our guidance philosophy hasn't changed, but I think our perception of the uncertainty or risk of the environment has changed and given how well we've operated over the course of the last two years of the pandemic, it would be hard for us -- despite the uncertainty that still exists, I think we just have a lot of confidence that we can execute in that environment, and that hasn't been the case the last two March’s when we've provided that guidance.

So I wouldn't describe it as a change in philosophy or a change in conservatism, but I think it's just sort of reacting to the facts as we have them and less risk and less uncertainty than we've had previously.

- CFO/COO Mike Gordon

On progress with their serverless offering:

So the whole notion of serverless is to essentially abstract the way the need to do capacity planning that people can basically connect to our database start using it and not have to worry about it anymore in the database to just scale up and down based on the needs of the application. And so, the early feedback has been incredibly positive. We're seeing a lot of interest.

We have a lot of people using it today. We're getting great customer feedback. And you'll see us continue to invest aggressively on serverless

- CEO Dev Ittycheria

And now, new positions that had reported earlier in the quarter. I unfortunately had no success getting expected FCF numbers after the fact:

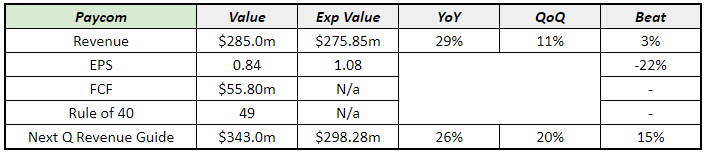

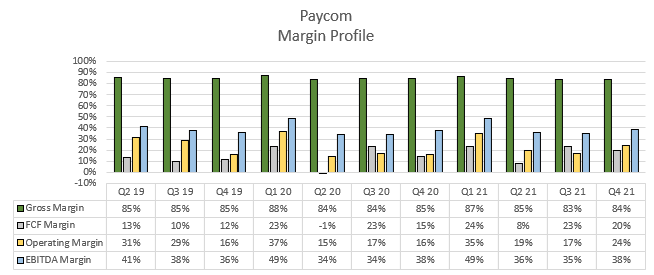

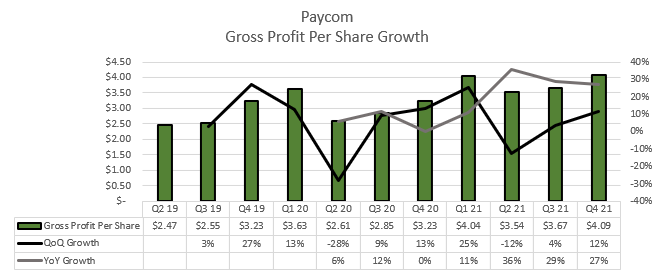

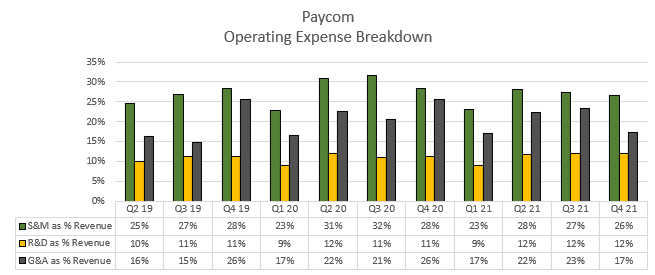

Paycom

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On continued incremental gains in net retention:

Obviously, 2020, we did have some retreat in our revenue, just the natural attrition that came from those employees being laid off or leaving their business during the pandemic. And then now in 2021, we've been able to increase it once again to 94%. And answer to that question, it's all really driven by usage. The more success a client has using our products, the greater the return on the investment they're achieving, and that makes them want to stay with us longer.

And so, how high can it go? Obviously, at some point, you do have to look at you're always going to have a certain number of clients that could be bought, sold, and merged. But I -- we're very ambitious with that number. We're seeing a lot of satisfaction across the client base. So, I don't -- I wouldn't necessarily say we're done with our retention aspirations, but we feel really good by being able to raise it again.

- CEO Chad Richison

On raising rates providing a small revenue tailwind from float:

I mean, obviously, if there are rate increases, which we're talking about here in the first quarter in March, that would be a tailwind to us. Based on the average daily balance, it's somewhere between $4 million and $5 million on an annual basis, but that would layer in, Mark.

- CFO Craig Boetle

On sales efficiency trends:

Sales productivity is way up from pre-pandemic levels when you look at a -- on a per-rep basis or even if you look at a per-team basis. When you lose one of your senses, the other takes over and we just -- we became a lot better throughout the pandemic in how we sold. We got better at strategy. We got better at connecting to our prospects.

We got better at marketing. We got better at retargeting. So, sales has been very strong, and it remains that today.

- CEO Chad Richison

On impact from large UKG ransomware attack:

We're having success with that. It's a pretty bad deal when you're down that long, and we are having success with that.

Our hearts go out to those clients and especially their employees that are impacted. But those are a little bit longer sales cycle when you're talking about the larger deals. I think this happened in December. Obviously, we're on it.

We do believe that we're going to have success taking some business. And, I mean, I think if you're a CFO or HR person, you'd be hard-pressed to stay in that environment without quite a few explanations. I mean, at some point, you got to read the room on what industry you're in.

- CEO Chad Richison

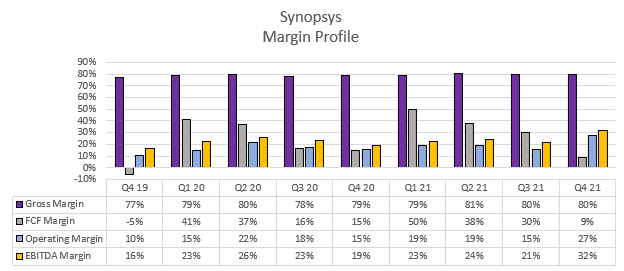

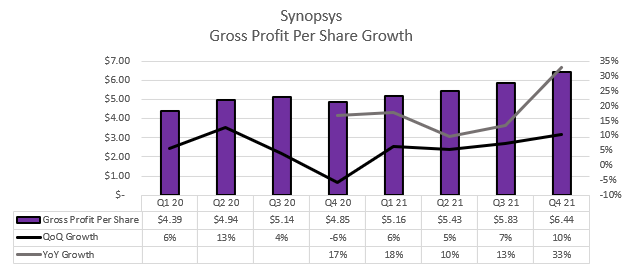

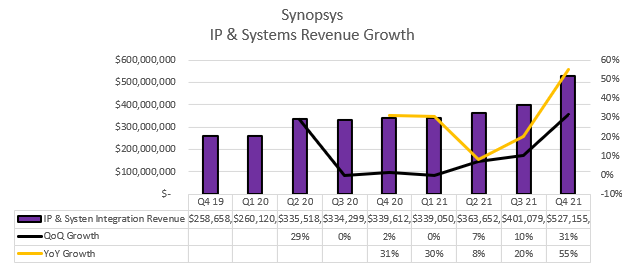

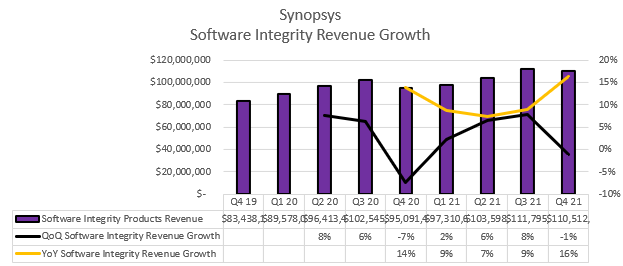

Synopsys

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On reasoning behind increased guidance:

Our strength has been really very much across the board. We can certainly say that the IP continues to stand out as growing very well. But some of the new capabilities that we see at EDA tools really are showing more and more opportunity going forward.

Now you heard about the Software Integrity Group. They continue on an excellent path. Last year was really a return to good growth and now we are improving the growth there as well.

And lastly, the systems area, which is sort of at the intersection between -- so we like to call it at the end of the section between silicon and software is an area that will continue to grow because most of the systems get now optimized to make the software run as well as possible on the hardware and the hardware to be as responsive as possible to the software all the way to trying to optimize even the power consumption.

- Co-CEO Aart de Geus

On the opportunity of shifting workloads to the cloud brings:

We do see cloud as a very strong incremental growth opportunity, and that is independent of whether or not they're using Synopsys cloud or a third-party cloud. We can support other scenarios, but the goal is to gain that business overall.

- CFO Trac Pham

On Aart’s thinking around a semiconductor cycle currently with his 40 years of experience in industry:

I'm very clear about this. I think that we are into a long-term great opportunity wave. Because the opportunity to change how the world operates with the combination of enormous amount of data combined with machine learning, ultimately, AI and automation has very, very big economic impact for every vertical.

Now at the same time, we are all well aware that there are some shortage of certain -- actually a fairly limited set but crucial set of parts. And I'm hesitate to call that a cycle. There have been interruptions in the supply chains due to global politics. There have been COVID that stop people from ordering. There have been a lot of things and it's mostly older parts.

And so yes, there's some shortage there. There's some additional capacity being built in. Most of the capacity is being lined up for actually advanced nodes because of the earlier point I made all these new opportunities. And so there will be always a little bit of a cycle of supply and providers alignment. But in general, I think that we're in for a decade of great opportunities in semiconductors.

- Co-CEO Aart de Geus

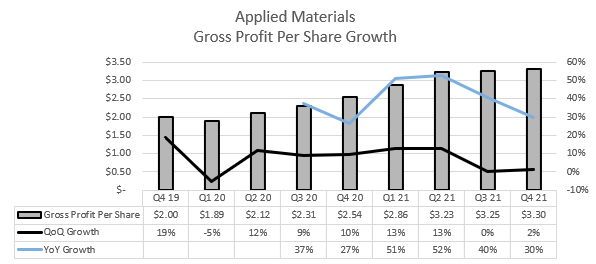

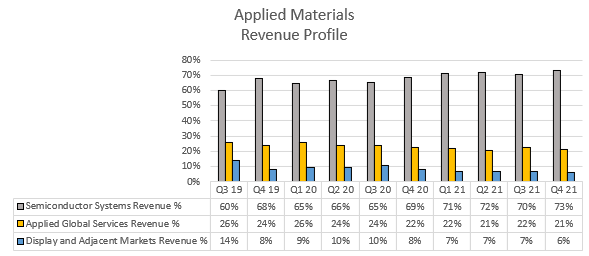

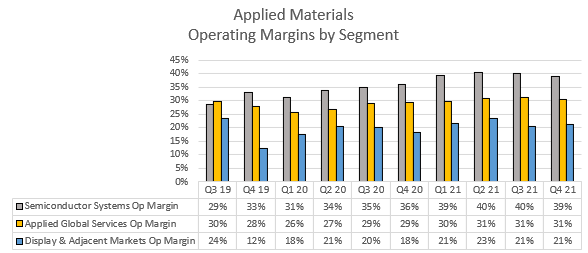

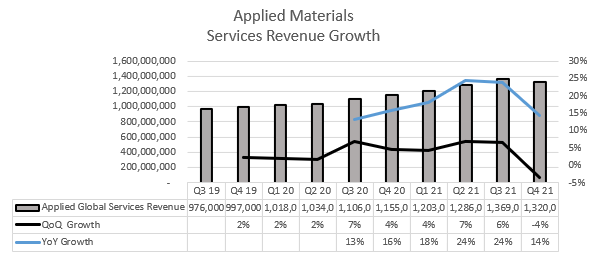

Applied Materials

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On their perspective of where we are in semi-cycle:

So if you go look at the history of the industry the last 15 years, 20 years, some of the leading indicators of when you overbuild is particularly strong memory is three years of a strong memory year. '07, '17 and '18, we're all over 50% in memory. So if you look at it right now, memory was 40% of WFE in 2021 and going down several points in '22.

So we look at memory as moderate growth and we don't see double bookings there. Second thing is a leading indicator of whether they're overbooking in the short term, we look at wafer starts and we look at fab utilization. So I said last quarter, fab utilization was at a record at our fiscal Q4. In fact, in Q1, fab utilization is slightly higher, so very high.

Thirdly, if you look at wafer starts over the last several years, wafer starts from '16 to '21 in memory, DRAM and NAND were both 19%. That's not a compound rate of growth, that's a total growth from '16 to '21. If you look at 200-millimeter, it's 17%. If you look at where the growth was, it was kind of 300-millimeter stuff, 100% from '16 to '21 in logic and foundry, right, logic/foundry.

- CFO Bob Halliday

On growth drivers moving forward and status:

If you look at the WFE by application base from '21 forward to '26, some of the biggest growth areas are, if you look at its data center, the accelerators, but it's also automobile, IoT, comms and some stuff in phones, particularly sensors. So there's big demand on this ICAPS sensor stuff. So if you look at it, the demand is there. And the funding of that through tools is not there because you don't have enough rolling over from the leading edge because the demand is going up on the trailing edge, right? So then, you look at it and say, well, what is the actual demand? So we said 53% in '21 and '22 for ICAPS.

Well, if you drill into 20-nanometer and above, so -- or 10, 14, 16 and look at some of the older stuff, particularly 28, it's gone up as a percentage of WFE from 31% in '20 to 43% in '21 and 44% in '22. So because of two factors, demand going up and less tools to roll over to those. So somebody might say, well, gee-whiz, that's overheated. Well, if you look at the rate of increase is declining, right? It went 31%, 43%, 44%.

- CFO Bob Halliday

On order demand and ability to fulfill those:

We have more orders than we can ship. If you look at our backlog build, it was $1.3 billion in the quarter, and our backlog growth is pretty substantial in the next couple of quarters. So we are totally supply constrained as everyone is in the industry.

- CFO Bob Halliday

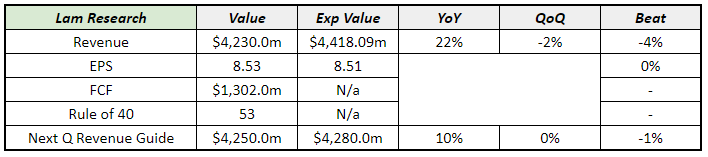

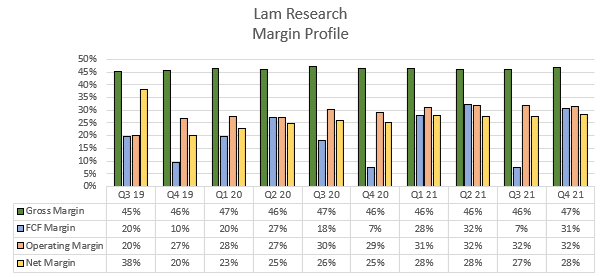

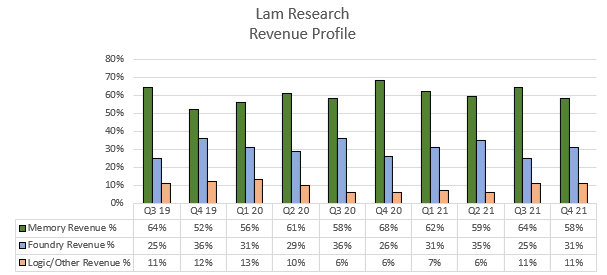

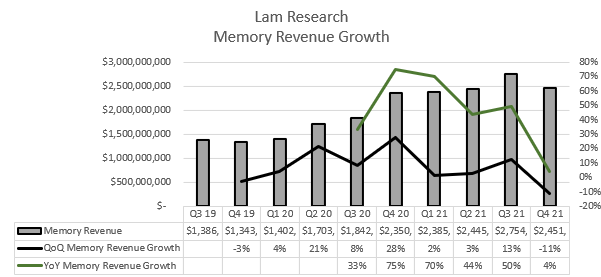

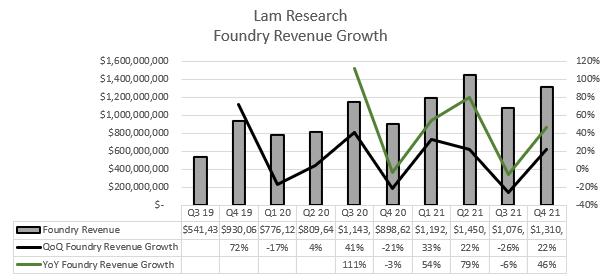

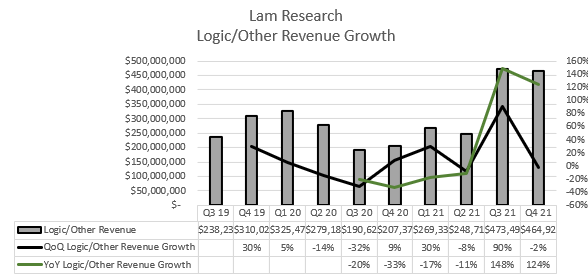

Lam Research

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On demand balancing outlook for this year:

I do think WFE is back-half weighted this year, maybe it's much to do with where true demand is, but also a little bit because I believe the industry in the first half of the year is going to be somewhat supply constrained. So, I think it's going to be a second-half weighted spending year [along with revenue].

- CFO Doug Bettinger

On China demand:

I think that from a China WFE perspective, we think it remains very broad demand across many different players. In fact, even some new fabs and new players that are new in the market there. And, you know, while some of it, of course, are big players, a lot of it is -- are fabs that are addressing what we all know is a very tight trailing-edge technology landscape. And so, I think that is a pretty big driver for WFE, and Lam participates well in that market.

And Doug mentioned our Reliant business that continues to show record after record in terms of business. And a lot of that stems from investments in places like China at the leading-edge nodes.

- CEO Tim Archer

Also:

I'm just going to say, it's a very broad set of customers was all I was going to add, Krish. A lot of whom you've probably not even heard of, frankly. So, there's a long tail of people spending dollars in China.

- CFO Doug Bettinger

On companies over-stocking inventory:

I mean, clearly, everyone is increasing held inventory. That probably goes to our spare parts business as well. Over time -- and I don't know when that would be because I think people are going to be a little bit cautious for quite some time about supply issues as we're talking about. Eventually, they will draw those inventories back to probably more efficient numbers, and that would cause some mitigation in the spare parts business part of the CSBG.

- CEO Tim Archer

On discussions Lam Research is having with customers about 2023:

I mean, obviously, we have sufficient conversations for very long lead time decisions that we have to make. You know, so as I talk about our expansion of manufacturing facilities and hiring rates, you know, one of the components, it's -- you know, not a -- that has a relatively long lead time is the hiring of engineers to go on-site to support those new customer facilities and projects. And so, I would say we're already having discussions with customers about 2023 in earnest.

But it's a little too early to get as precise as many of you probably like in terms of what does the number for 2023 WFE looks like, and we're not going to have that conversation today. But I would say, customers are giving a lot of [Inaudible] they want us to be ready. We're having those same conversations with our suppliers because we need them to be ready. And so, you can just believe that we're having those conversations quite frequently in quite some depth with customers today.

- CEO Tim Archer

On gross margin improvements progressing throughout 2022:

In my prepared remarks, I specifically said I believe gross margin will improve for us as the year progresses, meaning the March quarter, I believe, is a low point for the gross margin in the year. A lot because of these freight logistics and other things in the supply chain that we just need to go fix it, and that's what we're doing.

- CEO Tim Archer

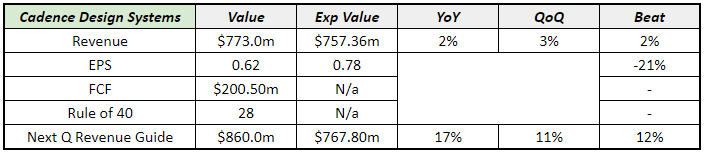

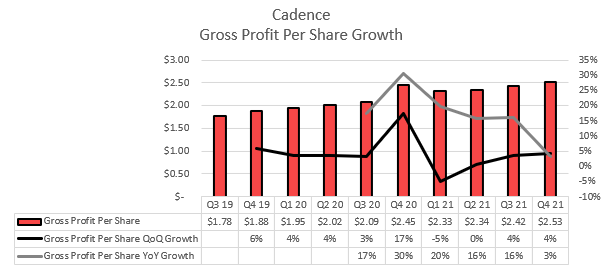

Cadence Design Systems

The Numbers:

The Trends Visualized:

Earnings Call Quotes:

On growth drivers inside business segments:

I think what I would like say is that, we feel that all business groups in all product areas and all regions are performing well at this time. So we feel pretty good where we are in the design activity we see. So we are expecting good growth across our portfolio. And I think we feel good how we are positioned.

- CEO Anirudh Devgan

Also:

So we’re expecting a very strong Q1. And we have a lot of visibility into core EDA. We continue to expect like double-digit growth there. I called out IP. IP, we typically aim for low teens.

If you look at the three-year CAGR, we’ve achieved mid-teens in that, but we typically aim for low teens, because we’re looking for the highest level of sustainable, profitable revenue growth there. I don’t want to give the team the opportunity to walk away from some business if it’s not the profitable nature we want.

- CEO Anirudh Devgan

On a shifting customer type revenue mix:

Richard, I think what we say is that about 45% of our revenue is coming from system companies versus semi companies. And over the years, that has increased — it used to be 40% now trending towards 45%.

And as you know, there is more and more system companies doing silicon and semi companies are becoming more system companies and system companies are becoming more semi companies. So that is a good trend for us and for the industry.

- CEO Anirudh Devgan

On their provided outlook with medium term targets:

I definitely think it’s going to be a historic year. I mean you can see from the guide in the in the CFO commentary that the three-year CAGR continues to accelerate. I think we’re — with the 12% revenue growth embedded in the guide for 2022, our three -year CAGR is naturally rounding up to 13%, when we achieved 12% this year.

Now it’s off of the back of a strong Q1. The second half of the year is tougher to predict for hardware. So that’s why I kind of modeled it out at 50% of our revenue falling in the first half versus second half. If we see the demand continue to flow through into the second half, then that will take the guide up. But it’s — but it’s tough to see that right now because typically our visibility in hardware and the pipeline is about six months. So I mean, that’s basically how we constructed the outlook.

- CFO John Wall

On Cadence Cloud adoption:

Our Cadence Cloud portfolio continued to scale with over 250 customers using our solutions in the cloud. Cadence Cloud-ready products are enabling our customers to realize meaningful scalability, performance and productivity benefits through the availability of several flexible use models.

- CEO Anirudh Devgan

Conclusion

As you can probably tell, I’ve become quite interested in semiconductor companies, and wow is it a challenge to following along these earnings calls but I do think it’s a fun challenge to scale up the learning curve.

This is 100% how I work through these transcripts:

Now, it’s worth noting that many of these companies I was catching up on (especially the semi companies) reported before any Ukraine-Russia war escalations, and there has also been recent news like TSMC saying China’s demand for mobile is beginning to soften due to lockdowns.

I think Q1 earnings season will be filled with fireworks as we get updated outlook on spending and demand trends.

Thank you all for reading for another completed quarter! I will be posting my Portfolio Review and What I Learned this week, and the first Q2 edition for Sector Analysis will come out 4/17!

- Sean

Great stuff!

Hi Sean, excellent write ups and end-of-quarter analysis, thanks. Liked very much your charts templates, how do you manage the x-axis to be arranged that way in excel? Thanks again!